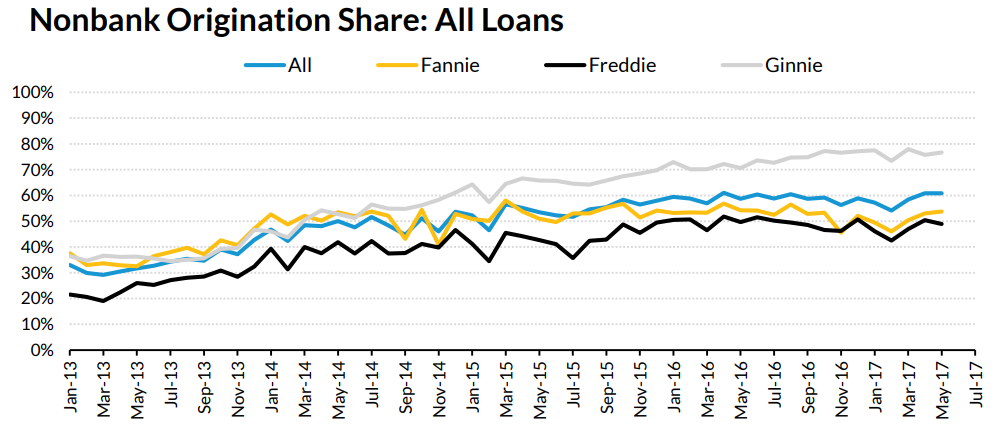

Mortgage originations by nonbanks have not only surged past those coming from regulated banks, but according to the Urban Institute (UI), they are helping to widen the credit box for agency and government loans. Where in 2013 banks originated 70 percent of new mortgages, this year nonbanks originated 60 percent.

In an article in UI's Urban Wire blog, three analysts say that, while banks have been the traditional lender for most homebuyers, "the market turbulence of the past decade has spurred a significant restructuring of the mortgage finance industry, thrusting nonbanks-institutions that provide some banking services but are not regulated banks-into a dominant position as mortgage originators."

UI's analysts, Karan Kaul, Bing Bai, and Linda Goodman, indicate in their article that the shift in originations is less because nonbanks are aggressively seizing a larger share but rather because banks are willingly ceding it.

Since 2013, the nonbank share has increased across the board, with Ginnie Mae seeing the biggest jump, from 36 percent in 2013 to 76 percent of originations today. The share of nonbank Freddie Mac loans have increased at nearly double the rate of Fannie Mae's (up 27 percentage points versus 14) so now their nonbank origination percentages have nearly converged.

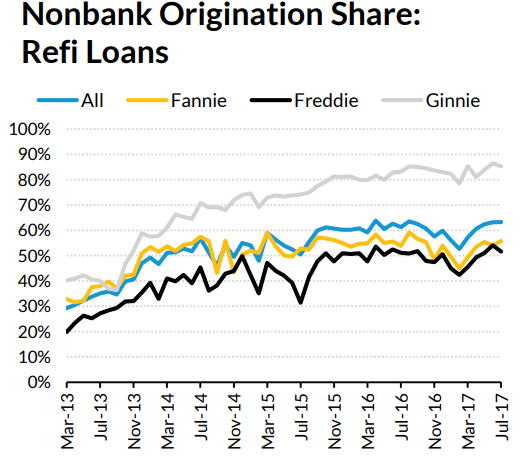

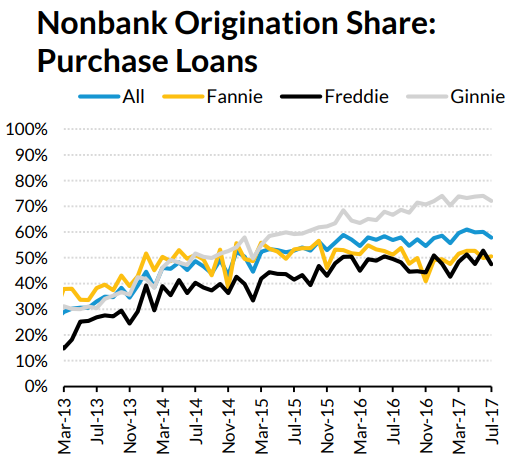

Nonbank originations are higher for refinances than for purchases across all three agencies. In 2017, 58 percent of purchase mortgages were originated by nonbanks compared with 63 percent of refinance mortgages. For Ginnie Mae loans, 72 percent of purchase mortgages were originated by nonbanks versus 85 percent of refinances.

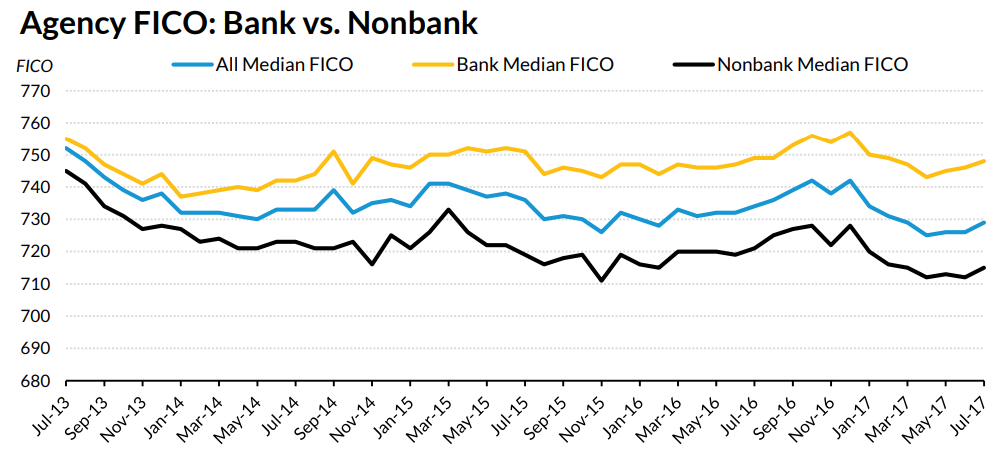

The authors say this new origination pattern has played a key role in easing credit access. Median credit scores have declined for all loans since 2013, with the median score for all originations down 23 points. This is largely because of nonbanks, where the decline is 30 points (from 745 to 715), while the bank-originated median is down only 7 points. Ginnie Mae, FICO scores have increased for bank originations but moved in the opposite direction for nonbank loans, reflecting the sharp cut-back in FHA lending. Nearly all of the decline has been in refinancing; with purchase originations have seeing little relaxation in scoring on the part of many banks.

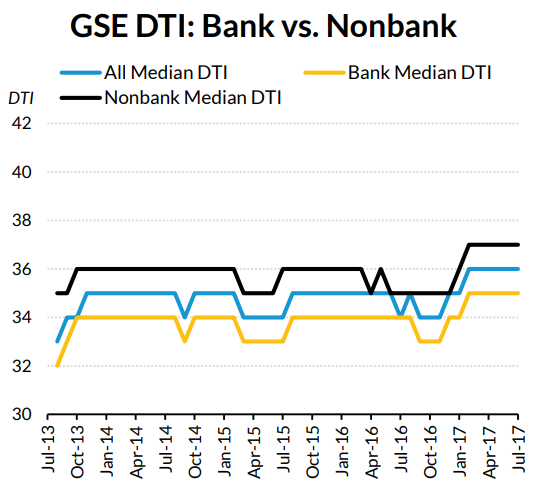

When it comes to loan-to-value (LTV) ratios, there is only a slight difference between the two origination sources for GSE loans and essentially none for Ginnie Mae loans. Debt-to-income (DTI) ratios are a different matter. UI says that this year there has been a measurable increase in DTI across all loans and originators, but the nonbank median is higher.

This increased reliance on nonbanks could pose some risks for the GSEs and the Federal Housing Administration (FHA). UI notes that, as nonbanks are not a strictly regulated as banks, there may be greater counterparty risks. Many nonbanks are assuming the market share left behind by banks are not well capitalized; this raises concerns they may be more willing to take risks

The decline in bank lending, the authors day, is because of wariness about originating FHA and GSE loans. They cite three reasons behind this:

- Lack of clarity about when the bank might be forced to buy a loan back from an investor, and related reputational and litigation risk.

- The high cost of servicing delinquent loans.

- The uncertain litigation risk from Ginnie Mae's "overly aggressive enforcement" of the False Claims Act.

If these concerns are addressed, UI says, banks might reclaim their previous market share. While significant progress has been made in reducing lender uncertainty, FHA has lagged behind the improvements made by the GSE's and their regulator, the Federal Housing Finance Agency.