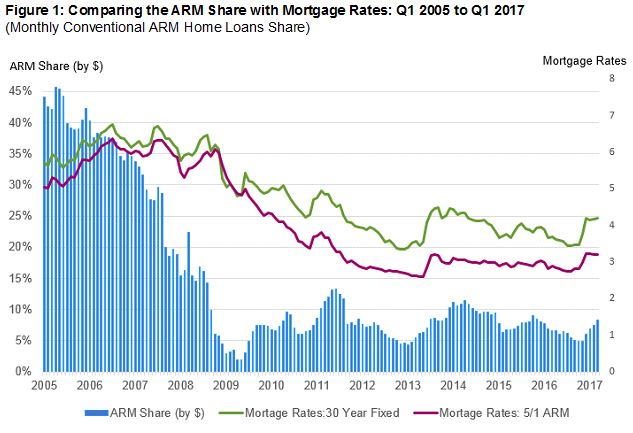

To paraphrase Mark Twain, reports of the demise of the ARM may have been greatly exaggerated.

The market share of ARMs (adjustable rate mortgages) dropped to 2 percent of originations and have fluctuated between 5 and 13 percent since, rising when fixed-rates rise and falling when those rates decline. In the first quarter of this year they accounted for 8 percent of originations. Contrast this with the 45 percent share ARMs represented in mid-2005.

However, as Archana Pradhan CoreLogic senior professional economist, writes in the company's Insights blog, if fixed-rate mortgage (FRM) rates increase in the coming year, it is likely the ARM share will as well.

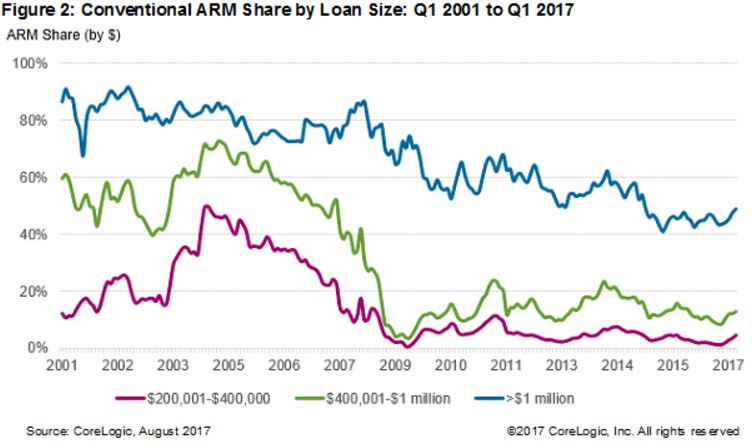

Despite their small percentages in the larger universe of mortgage originations, ARMs have consistently been a significant factor for homebuyers who are borrowing large amounts of money. Of mortgages that were originated during the first quarter of this year with balances in excess of $1 million, 47 percent were ARMs, up 4 percentage points from the previous quarter. In the $400,001-$1 million range, the ARM share was about 13 percent, up 3 percentage points from Q4 2016. However, among mortgages in the $200,001-$400,000 range, the ARM share was just 4 percent for Q1 2017, although that too was an increase, up 2 percentage points from the previous quarter.

Pradhan says that borrowers have historically favored ARMS when they are income-constrained or because they preferred the lower rate relative to FRMS. The latter is especially true when the spread between the two types of rates is wide.

ARMS got a bad rap because they performed more poorly during the housing crisis than did FRMs. Because underwriting standards were eased during the housing boom there were a lot of risky products available, such as the option ARM which allowed the borrower to choose whether to make a full payment, interest only, or even a partial interest payment (negative amortization) for a specified term after origination. There were also loans written without full documentation or verification of whether the borrowers had the ability to repay the loan.

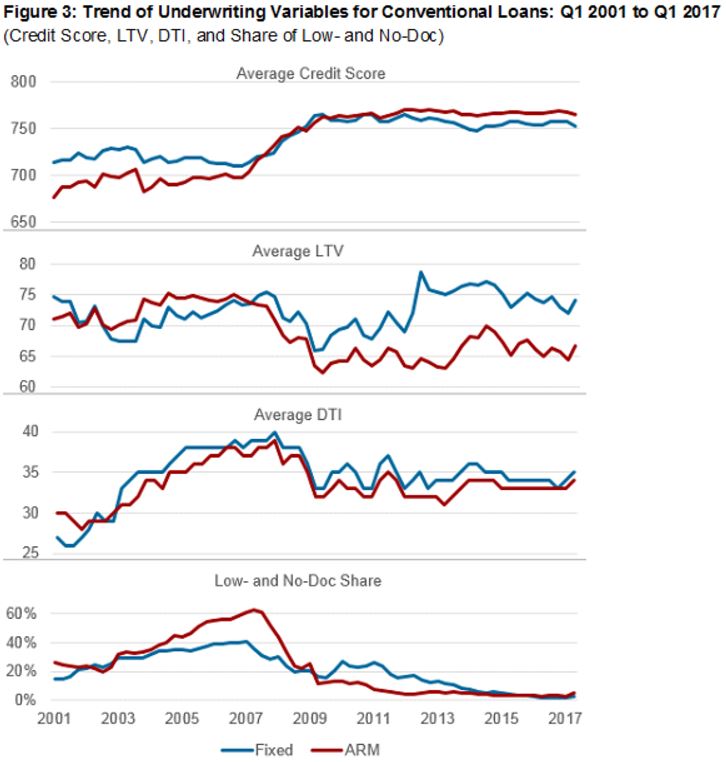

Today's ARM is very different from those written pre-crash. In 2007 about 60 percent of ARMs were low- and no-doc compared with only 40 percent for FRMs. Similarly, 29 percent of borrowers with ARMs during 2005 had a credit score below 640 compared with only 13 percent for FRMs. Today, almost all conventional loans, including both ARMs and FRMs, are full doc, amortizing, and made to borrowers with credit scores above 640.

Figure 3 shows four major variables for underwriting loans. One, low/no doc loans, now have a nearly negligible share of originations for either ARMs or FRMs. For each of the other three, credit score, loan-to-value (LTV) and debt-to-income (DTI) rations, the current credit risk is significantly better for ARMs than for FRMs.

As of Q1 2017, the average credit score of borrowers with ARMs was 765 compared with 753 for borrowers with FRMs and the LTVs averaged 67 percent and 74 percent respectively. The average DTI for borrowers with ARMs is also slightly lower compared with the DTI for borrowers with FRMs. Pradhan says that, as illustrated, ARMs today have much lower credit risk than ARMs of a decade earlier, and in addition, have lower risk attributes than today's FRMs.