The Federal Reserve's most recent Senior Loan Officer Opinion Survey on Bank Lending Practices noted that the demand for some types of residential real estate loans had weakened over the previous three months. In addition, most of the 55 domestic banks and 22 U.S. branches and agencies of foreign banks that responded to the survey indicated that they expected this lack of demand to continue through the year.

Conducted in July, the survey addressed changes in Banks' perceived demand for loans to businesses and households over the past threee months.

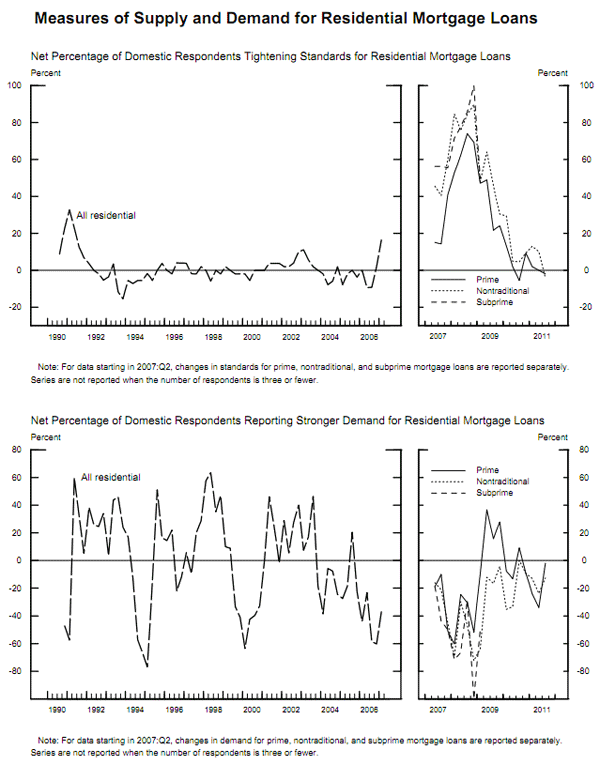

Questions about residential real estate cover three types of loans; prime, subprime loans, and non-traditional mortgages which include interest only and Alt-A mortgages such as those requiring limited income and other verifications. Banks themselves are classified as "large" if they have assets greater than $20 billion and "other" if assets are less. 53 banks responded to the set of questions on residential mortgages.

Over three-quarters of banks reported that their credit standards for both prime and non-traditional loans had remained basically unchanged over the last three months. The remaining respondents were divided fairly evenly on whether standards had tightened or eased, but none of them indicated "considerable" easing or tightening. Only about half the respondents said they offered nontraditional mortgages and too few banks answered questions about subprime loans for the responses to be reported.

There was considerably more differentiation among responses to questions about consumer demand for residential mortgages. 53 percent of banks said that the demand for prime mortgages had remained about the same during the previous three months while 22.6 percent called demand "moderately stronger." 24.5 percent thought demand was moderately weaker. Among the smaller group offering non-traditional mortgages 71 percent said demand was about the same, 21 percent noted moderate or substantial weakening and 8.3 percent said demand was moderately stronger.

The bankers were also questioned about standards and demand for home equity lines of credit (HELOCs). Over 88 percent reported that credit standards were unchanged. Of the five banks (9.4 percent) reporting somewhat eased standards, four were large banks. Only one bank said that his bank's standards had tightened somewhat.

Demand for HELOCs was unchanged among more than half of the banks while more than one quarter said demand had weakened and 19 percent indicated moderately stronger demand. A disproportionate number of those reporting moderately stronger demand were those classified as "other" banks.

The Federal Reserve asked bankers a series of questions about their expectations for the second half of the year regarding closed-end residential loans. None of the bankers expected significant increases or decreases in demand and 75 percent expected no change at all. The remainder were evenly divided (9.5 percent each) among those expecting originations to decrease somewhat and those expecting them to increase somewhat.

Respondents were given eight reasons why demand for closed-end residential real estate loans might increase or decrease over the remainder of the year and asked to assess their importance. Here's how the responses stacked up in terms of the percentage of respondents ranking these statements as "somewhat or very important"

- 98 percent: "Reduced or Unchanged Demand From Creditworthy Borrowers"

- 95 percent: "Uncertainty About The Economy" 95 percent said this was somewhat or very important.

- 93 percent: "Uncertain or Unfavorable Forecasts for House Prices"

And here are the percentages of respondents who said the following factors were NOT important to loan demand through 2011:

- 70.5 percent: "lack of secondary and securitization markets for non-conforming loans"

- 61.4 percent: "The expected reduction in conforming loan limits"

- 70.5 percent "reduced availability of private mortgage insurance"

With respect to consumer lending, the net percentages of banks that reported easing standards were low and roughly in line with the previous survey. While positive net fractions of respondents reportedly experienced an increase in demand for both credit card and auto loans over the past three months, the pickup in demand was not widespread; moreover, demand for other consumer loans was about unchanged.