RealtyTrac's July U.S. Home Sales report is a tale of extremes. July sales of properties in foreclosure and all-cash transactions both dipped to multi-year lows while home sales for the first six month of 2015 and July home prices hit seven and eight year highs.

There were 1.34 million single family homes and condos sold in the first six months of the year. This was the highest number of sales in the first half of any year since 2007.

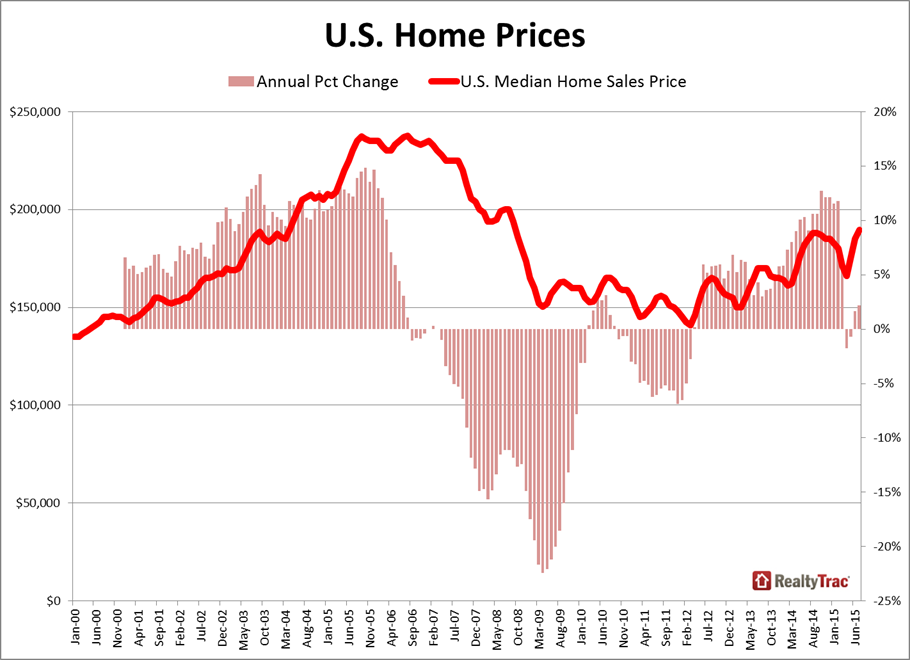

The median price of a home sold in July was $189,500 a 2 percent increase both from June and from July 2014. It was the highest median price since September 2008.

Meanwhile the sale of properties sold while in the process of foreclosure (but not yet REO) fell to 6.4 percent of all single-family and condo sales from 6.6 percent in June and 8.0 percent a year earlier. This was the lowest monthly share since January 2000, the earlier date the information was available. RealtyTrac does not indicate what is included in this metric but we assume it is both short sales and homes sold at foreclosure auction as other sources have put the share of short sales alone below 4 percent since mid-2014.

All-cash transactions made up 22.6 percent of all single family home and condo sales in July, down from 23.7 percent in the previous month and from 26.5 percent in July 2014. This was the lowest percentage of cash sales since July 2008. At the post-housing crisis peak in February 2013 39 percent of sales were all cash.

"While the stock market may be on a roller coaster as of late, the housing market is still on solid ground, with the eight-year low in cash sales combined with the eight-year high in overall sales volume in the first half of the year evidence that housing is successfully transitioning from an investor-driven recovery to one that is drawing in traditional buyers as a good foundation for sustainable growth going forward," said Daren Blomquist, vice president at RealtyTrac. "That's not to say there are no cracks in the foundation of this recovery, the top three of which are housing affordability - or lack thereof in some high-flying markets - along with overdependence on capricious cash buyers - both foreign and domestic - in some markets, and the persistent overhang of underwater homeowners who continue to represent heightened default risk given any future economic shockwaves."

Ten markets out of the 161 analyzed reached new home price peaks in July bringing the share of markets that have surpassed pre-crash peaks in the last 18 months to 20 percent. New peaks were established in July for the Denver, San Jose, Columbus (Ohio), Nashville, Raleigh, and Omaha markets. Also setting new highs were Colorado Springs, Madison, Burlington (Vermont), and Boulder,

Home sale volume for January through June was at an eight year high in 124 of the 190 housing market for which data was available and 24 markets recorded 10 years highs. In four markets, The Villages (Florida), Lincoln, Pittsburgh, and Denver, sales were the highest since 2000, the first year for which data was available.

While cash sales nationally are almost down to half of the recent peak they remain elevated in a number of areas, especially in Florida, home of nine of the ten markets with the highest percentage of such transactions. They include several of the largest cities (Miami, Naples, Sarasota) but also smaller markets like Sebastian, Homossa Springs, Sebring, Port St. Lucie, Punta Gordo, and The Villages. The cash sales in each of these areas was 47 percent or greater. Number ten for cash sales was the New York City market.

Metros with highest share of in-foreclosure properties in July were Salisbury, North Carolina (23.6 percent), Rockford (17.1 percent), Morehead City, North Carolina (16.3 percent), Baltimore, (16.1 percent), Toledo (15.2 percent) and Chicago (14.7 percent).

In 61 of the 172 markets analyzed for in-foreclosure sales (35 percent), the share of in-foreclosure sales increased from a year ago, counter to the national trend. Those markets included Chicago, Atlanta, Boston, Baltimore and Pittsburgh.