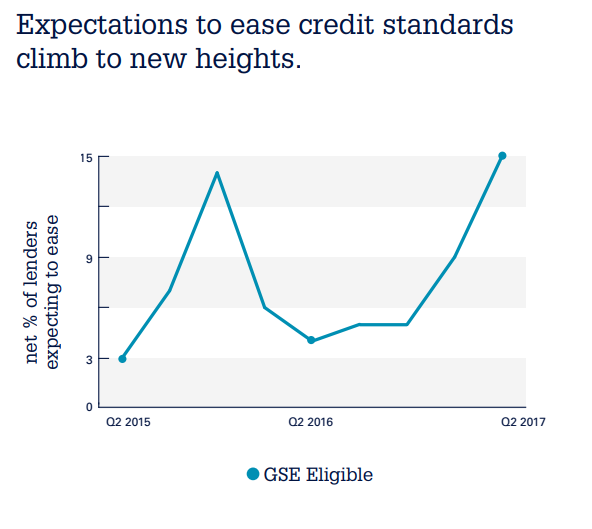

With mortgage volumes expected to decline, more lenders are telling Fannie Mae that they intend to loosen their credit standards. The company's second quarter 2017 Mortgage Lender Sentiment Survey found that, on net, the share of lenders reporting they have eased mortgage credit standards over the previous three months has continued the gradual uptick which started in the fourth quarter of last year. Additionally, when anticipating the next three months, the net share of lenders saying they plan to ease credit standards for GSE eligible, non-GSE eligible, and government loans reached or surpassed survey highs.

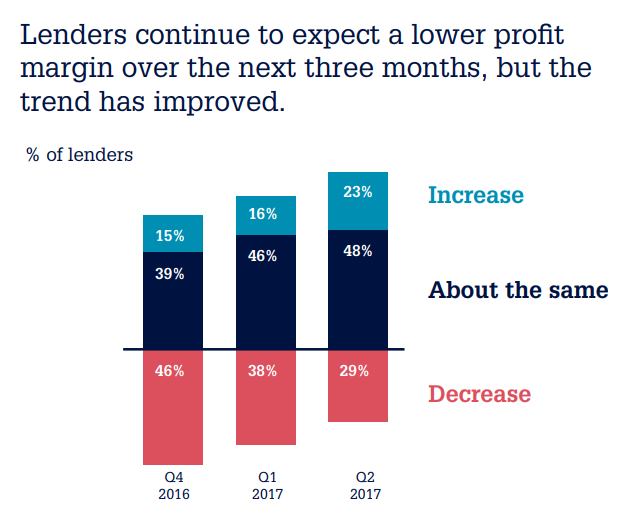

"Expectations to ease credit standards climbed to survey highpoints in the second quarter as more lenders reported slowing mortgage demand and increasing concerns about competition from other lenders," said Doug Duncan, senior vice president and chief economist at Fannie Mae. "Lenders cited additional contributing factors such as diminishing compliance concerns and more support from the GSEs, including clarification on representations and warranties and tools that provide greater certainty during the loan underwriting process. Easing credit standards might also be due in part to increased pressure to compete for declining mortgage volume. For the third consecutive quarter, the share of lenders expecting a decrease in profit margin over the next three months exceeded the share with a positive profit margin outlook. For the former, the percentage citing competition from other lenders as a reason for their negative outlook reached a survey high."

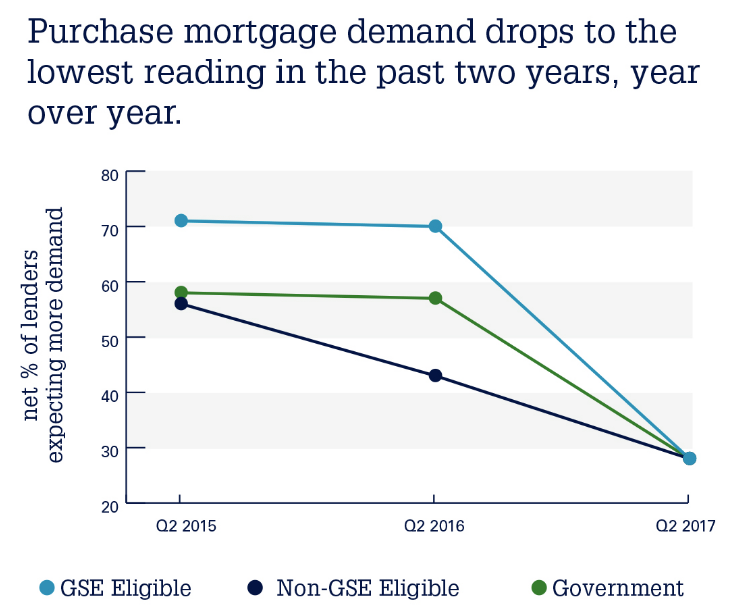

Slowing of demand was noted for both purchase mortgages and refinancing. The share of lenders reporting demand growth for purchase loans over the prior three months was in single digits (3-7 percent) for all three loan types. On net, responses reached the lowest reading for any second quarter in the last two years.

Duncan noted that the lenders' reports of diminishing demand for purchase mortgages parallels the latest findings from his company's National Housing Survey. Responses to the question about whether it is a good time to buy a house dropped, on net, to a survey low. "The results of both surveys mirror the ongoing narrative for housing: Tight inventory has pushed up home prices, which is weighing on affordability and constraining sales," he said.

Looking forward, the net share of lenders expecting increased demand over the next three months remained relatively stable compared to the second quarter of 2016. The net positives ranged from 10 percent for government loans to 15 percent for GSE eligible lending.

For refinance mortgages, the net share of lenders reporting rising demand over the prior three months fell significantly, reaching a three-year survey low across all loan types. The net share of lenders reporting demand growth expectations for the next three months has changed little from the previous survey in the first quarter of this year.

When asked about their mortgage execution plans, the lenders' net responses were for continued expectations to grow GSE and GinnieMae shares over the next 12 months and reduce portfolio retention and whole loan sales shares.

The net share of lenders reporting a negative profit margin outlook has declined since reaching the survey's worst reading in the fourth quarter of last year, however more lenders reported a negative outlook than a positive one. Mid-sized institutions were most likely to expect a net decrease in profit margin, while larger institutions were more likely to expect a net increase.

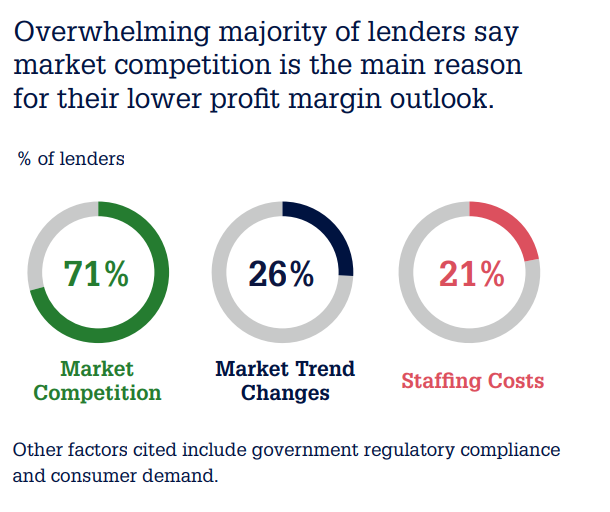

Among all drivers of profit margins, concerns about competition from other lenders was cited as the key reason for lenders' decreased profit margin outlook, setting a new survey high. The perceived impact of "government regulatory compliance," which declined sharply in Q4 2016, has remained low.

The Lenders Sentiment Survey was conducted in May, receiving responses from 207 senior executives representing 184 lending institutions. The breakdown was 58 mortgage banks, 82 depository institutions, and 36 credit unions. Seventy-two of the institutions were classified as small, with loan originations under $252 million and 54 as large, with volume over $1.01 billion.