The housing boom created a rich climate for mortgage fraud and while the bust that followed the boom has changed the nature of the crime, it has provided continued opportunities which the Federal Bureau of Investigation (FBI) is attempting to quantify. The Bureau has released a study that attempts to quantify the breadth and depth of mortgage fraud in 2010 so FBI program managers and the general public can better understand the current threat.

The report says that fraud continued in 2010 at elevated levels that were consistent with those seen in 2009. Mortgage fraud enables high profits through illicit activity while posing a relative low risk for discovery. The FBI notes that mortgage fraud schemes are particularly resilient and readily adapt to economic changes and modifications in lending practices. Thus current economic conditions with tightened underwriting, fewer loan originations, increased delinquencies and foreclosures, high unemployment, demands for debt counseling and loan modifications have all provided opportunities that can be manipulated and motives for doing so.

Mortgage fraud perpetrators include lenders, mortgage brokers whether licensed/registered or not, appraisers, underwriters, accountants, real estate agents, settlement attorneys, land developers, investors, builders, bank account representatives, and trust account representatives.

There have been numerous instances in which various organized criminal groups were involved in mortgage fraud activity. Asian, Balkan, Armenian, La Cosa Nostra, Russian, and Eurasian organized crime groups have been linked to various mortgage fraud schemes, such as short sale fraud and loan origination schemes.

Mortgage fraud perpetrators have a high level of access to financial documents, systems, mortgage origination software, notary seals, and professional licensure information necessary to commit mortgage fraud and have demonstrated their ability to adapt to changes in legislation and mortgage lending regulations to modify existing schemes or create new ones.

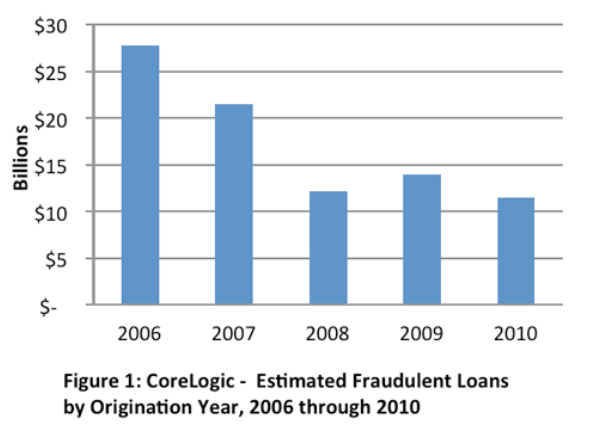

The losses attributable to mortgage fraud are unknown, but the FBI quotes CoreLogic estimates that between $12 and $15 billion in fraudulent loans were originated in each of the last three years. In 2006, the peak year identified by CoreLogic, there were $27 billion in fraudulent loans originated.

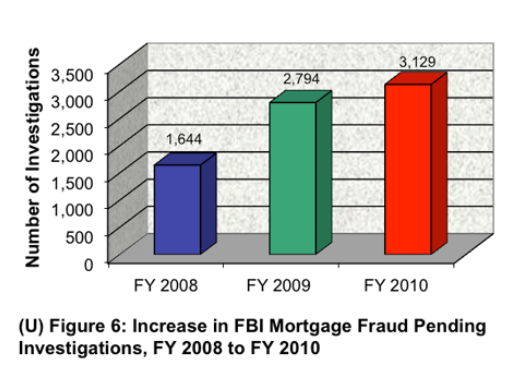

Suspicious Activity Reports (SARs) filed by financial institutions have risen sharply in the last three years . While not all SARs report a dollar loss (only 25 percent did so last year), those that did revealed $3.2 billion in losses in FY 2010, a 16 percent increase from FY 2009 and a 117 percent increase from FY 2008. As reports of suspicious activity have risen, so have open investigations. In FY 2010 the FBI had 3,129 pending investigations compared to 1,644 in 2008 and 2,794 in 2009.

Analysis of available law enforcement and industry data indicates the top states for known or suspected mortgage fraud activity during 2010 were California, Florida, New York, Illinois, Nevada, Arizona, Michigan, Texas, Georgia, Maryland, and New Jersey; reflecting the same demographic market affected by mortgage fraud in 2009.

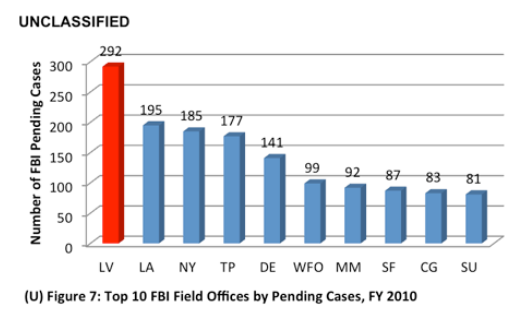

FBI field divisions that ranked in the top 10 for pending investigations during FY 2010 were Las Vegas, Los Angeles, New York, Tampa, Detroit, Washington Field, Miami, San Francisco, Chicago, and Salt Lake City, respectively.

The current investigations do not merely involve emerging information on fraud left over from the boom years. The report states that 55 percent of mortgage fraud cases opened in FY 2010 involved criminal activity that occurred in either 2009 or 2010.

It is unclear how much overlap there is in the cases reported by the FBI and from other sources. Mention is made, however, of 765 pending single-family residential loan investigations handled by the Office of Inspector General (OIG) at the Department of Housing and Urban Development (HUD). The OIG had 591 pending investigations in 2009 and 451 in 2008. The preventloanscams.org website maintained by HJUD has received more than 11,416 complaints as of December 31, 2010, with associated losses of more than $23 million.

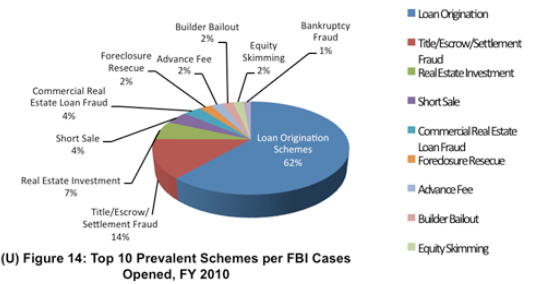

The FBI breaks down mortgage fraud schemes into 11 categories (see chart below.) The majority of cases opened in FY 2010 involved loan origination schemes (to include property flipping), followed by settlement-related schemes (to include kickbacks.)

Mortgage loan origination fraud is divided into two categories: fraud for property/housing and fraud for profit. The first, usually involving a single loan, entails misrepresentations by the applicant for the purpose of purchasing a property for a primary residence. Although applicants may embellish income and conceal debt, their intent is to repay the loan. Fraud for profit, however, often involves multiple loans and elaborate schemes perpetrated to gain illicit proceeds from property sales. Gross misrepresentations concerning appraisals and loan documents are common in fraud for profit schemes, and participants are frequently paid for their participation.

Loan Origination Fraud

These schemes involve falsifying a borrower's financial information--such as income, assets, liabilities, employment, rent, and occupancy status--to qualify the buyer, who otherwise would be ineligible, for a mortgage loan. Freddie Mac is reporting that the loan origination frauds they are witnessing include false documents, property flips with phantom rehabilitation, fictitious assets, and fabricated payroll documents. Freddie Mac reports the continued use of transactional "lenders" such as the "dough for a day" businesses that "loan" potential borrowers money to create assets for underwriting due diligence.

In a backwards application scheme, the perpetrator fabricates a borrower's income and assets to meet the loan's minimum application requirements through inflated income, fictitious assets, and altered credit reports.

Perpetrators fraudulently inflate property appraisals, often through overstated comps, to generate false equity with which they will later abscond. Perpetrators will either falsify the appraisal document or employ a rogue appraiser as a conspirator in the scheme.

Illegal property flipping involves the purchase and subsequent resale of property at greatly inflated prices. The key to this scheme is the inflated appraisal which enables the purchaser to obtain a greater loan than would otherwise be possible then flip it to a buyer at the inflated rate.

Traditionally, any exchange of property occurring twice on the same day is considered highly suspect for illegal property flipping and often is accompanied by back-to-back closings where a purchase contract and a sales contract that are both presented to the same title company. Property flipping is apparently occurring in 47 out of 56 field office territories. Among other industry sources reporting significant property flipping, Interthinx reports that it is still prevalent and trending upward. Current property flipping schemes reported by Interthinx involve fraud against servicers; piggybacking on bank accounts to qualify for mortgages; and forgeries. HUD reporting indicates the use of limited liability companies (LLCs) to perpetrate fraudulent property flipping.

Title/Escrow/Settlement Fraud/Non-Satisfaction of Mortgage

Over a third of FBI field offices are reporting some form of title/escrow/settlement fraud. The majority of these frauds involve the diversion or embezzlement of funds for uses other than those specified in the lender's closing instructions. Associated schemes include the failure to satisfy/pay off mortgage loans after closings for refinances; transfer of property without the homeowner's knowledge or consent; failure to record closing documents; recording of deeds without the title insurance paid for by the homeowner; and filing of fraudulent liens to receive cash at closing.

According to a review of FBI investigations opened in FY 2010, title agents and settlement attorneys in at least 21 investigations in 14 field office territories are involved in non-satisfaction of mortgage schemes, misappropriating and embezzling more than $27 million in settlement funds rather than using those escrowed funds to satisfy/pay off mortgages.

Real Estate Investment Schemes

Forty-three percent of FBI offices are reporting real estate investment schemes where perpetrators persuade investors or borrowers to purchase investment properties at fraudulently inflated values.

Short Sale Schemes

A real estate short sale is a pre-foreclosure sale in which the lender agrees to sell a property for less than the mortgage owed. One of the most common forms of a short sale scheme occurs when the subject is alleged to be purchasing foreclosed properties via short sale, but not submitting the "best offer" to the lender and subsequently selling the property in a dual closing the same day or within a short time frame for a significant profit. A recent CoreLogic study indicated that short sale volume has tripled from 2009 to 2010. In June 2010, Freddie Mac reported that short sale transactions were up 700 percent compared to 2008.

Industry sources report that in the process of committing short sale fraud, fraudsters are manipulating the Broker Price Opinions (BPOs) and MLS; engaging in non-arms-length transactions; failing to record short sale deeds of trust; using back-to-back and multiple real estate agent closings; selling the property to a party the fraudsters control and deeding the property back to themselves; engaging in escrow thefts, and dozens of other mechanisms.

Commercial Real Estate Loan Fraud

Commercial real estate loan fraud continues to mirror fraud in the residential mortgage loan market. Law enforcement investigations indicate that perpetrators such as real estate agents, attorneys, appraisers, loan officers, builders, developers, straw buyer investors, title companies, and others are engaged in same-day property flips; the falsification of financial documents, performance data, invoices, tax returns, and zoning letters during origination; the diversion of loan proceeds to personal use; the misrepresentation of assets and employment; the use of inflated appraisals; and money laundering.

Foreclosure Rescue

Perpetrators convince homeowners that they can save their homes from foreclosure through deed transfers and the payment of up-front fees. This "foreclosure rescue" often involves a manipulated deed process that results in the preparation of forged deeds. In extreme instances, perpetrators may sell the home or secure a second loan without the homeowners' knowledge, stripping the property's equity for personal enrichment. Analysis of FBI intelligence reporting indicates that foreclosure rescue schemes were the sixth-highest reported mortgage fraud scheme in FY 2010 and comprised 2 percent of all FBI cases opened that year.

Advance Fee Schemes

Mortgage fraud perpetrators such as rogue loan modification companies, foreclosure rescue operators, and debt elimination companies use advance fee schemes, charging victims for services that are never rendered, to acquire thousands of dollars from victim homeowners and straw buyers.

Builder Bailout Schemes

These are common in any distressed real estate market and typically consist of builders offering excessive incentives to buyers such as no-down payments, which are not disclosed on the mortgage loan documents.

Equity Skimming Schemes

This occurs when perpetrators drain all of the equity out of a property by charging inflated fees to "help" homeowners refinance their homes multiple times or obtain home equity lines, skimming the equity from the property and then encouraging the homeowner to use these funds for investment in various scams.

Debt Elimination/Reduction Schemes

FBI reporting indicates a continued effort by sovereign citizen domestic extremists throughout the United States to perpetrate and train others in the use of debt elimination schemes. Victims pay advance fees to perpetrators espousing themselves as "sovereign citizens" or "tax deniers" who promise to train them in methods to reduce or eliminate their debts. While they also target credit card debt, they are primarily targeting mortgages and commercial loans, unsecured debts, and automobile loans. They coach people on how to file fraudulent liens, proof of claim, entitlement orders, and other documents to prevent foreclosure and forfeiture of property.

In the current economy efforts to help distressed homeowners are also proving opportunities for mortgage fraud. Interthinx reports that property owners are fraudulently decreasing their income and property values, fabricating hardships, and filing false tax returns to get their debt reduced to qualify for loan modifications. Individuals who first perpetrated fraud in loan origination are now attempting to defraud again during their loan modification.

CoreLogic reports that mortgage fraud is becoming increasingly well-hidden and that lenders are reporting increases in hidden frauds such as short sale fraud, REO flipping fraud, and closing agent embezzlement. They are also seeing an increased frequency of flipping and straw buyer schemes in FHA loans.

Victims of mortgage fraud are both individual homeowners and lenders. Perpetrators target victims from across a demographic range, sometimes recruiting ethnic community members as co-conspirators and victims. Perpetrators identify common characteristics such as ethnicity, nationality, age, and socioeconomic variables, to include occupation, education, and income and target people who have access to tools that enable them to falsify bank statements, produce deposit verifications on bank letterhead, originate loans by falsifying income levels, engage in the illegal transfer of property, produce fraudulent tax return documents, and engage in various other forms of fraudulent activities.

The current and continuing depressed housing market will likely remain an attractive environment for mortgage fraud perpetrators who will continue to seek new methods to circumvent loopholes and gaps in the mortgage lending market. The FBI, however, cites recent legislation as having the potential to curb fraud mechanisms such as the elimination of BPOs under Dodd-Frank, features of the SAFE Act, and the partial prohibition of advance fees for loan modification services under the Federal Trade Commission's "MARS" Rule.

In June 2010, the Department of Justice announced a mortgage fraud takedown referred to as Operation Stolen Dreams which targeted mortgage fraudsters throughout the country and was the largest collective enforcement effort ever brought to bear in combating mortgage fraud. It involved 1,215 criminal defendants and included 485 arrests, 673 informations and indictments, and 336 convictions. The defendants were allegedly responsible for more than $2.3 billion in losses. The FBI current supports 25 mortgage fraud task forces and 67 working groups and continues to foster relationships with representatives of the mortgage industry to promote mortgage fraud awareness and share intelligence.

The FBI says the continuing depressed housing market will likely remain an attractive environment for mortgage fraud perpetrators who will continue to seek new methods to circumvent loopholes and gaps in the mortgage lending market. These methods will likely remain effective in the near term, as the housing market is anticipated to remain stagnant through 2011. Market participants are expected to continue employing and modifying old schemes and are likely to increasingly adopt new schemes in response to tighter lending practices.