Although home affordability is high, relative to pre-crisis levels, the rate at which their prices are increasing is cause for concern. Andrew LePage, CoreLogic Professional in Research Analysis, says the role of rising interest rates should not be overlooked; they can affect affordability more than home price appreciation.

Household incomes have not been keeping up with rising home prices, but the persistently low interest rates have mitigated some of the impact. But LePage asks, what will happen now that rates are trending higher again?

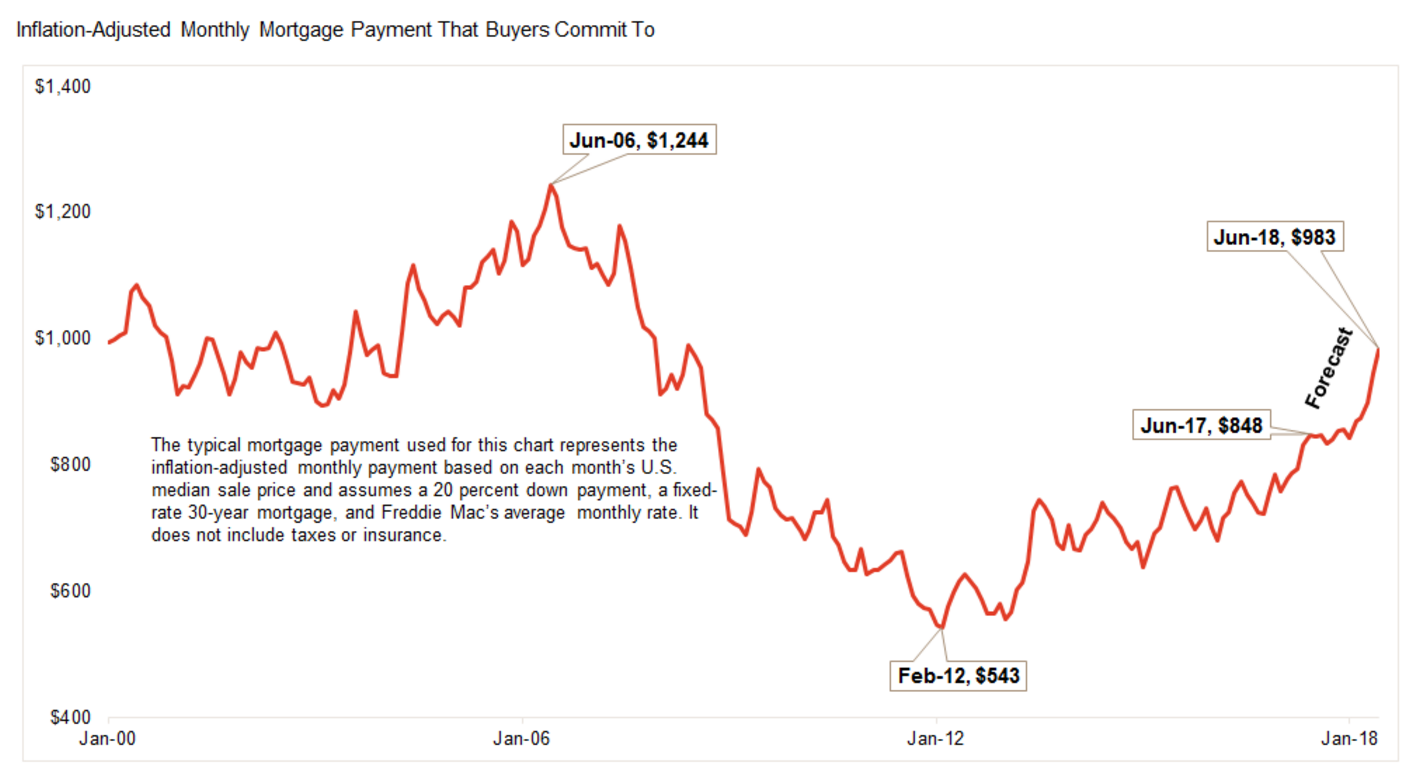

One way to measure how inflation, interest rates, and home prices impact affordability is "the typical mortgage payment." This is an interest rate-adjusted monthly payment derived each month using the median national home sale price and the Freddie Mac average rates for a fixed-rate 30-year mortgage with a 20 percent down payment. Insurance and taxes are not included in the calculation.

LePage says this is a good proxy for affordability because it approximates the amount for which the borrower would have to qualify for a mortgage to buy a median priced home. Adjusting that amount for inflation adds some historical context over time.

The chart below shows that, while the typical monthly payment has trended higher in recent years, it remains significantly lower than the pre-crisis version on both an inflation-adjusted and rate-adjusted basis. At the measure's peak in June 2006, the inflation-adjusted typical mortgage payment was $1,244, 47 percent higher than the typical payment this past June.

Another component driving the difference, the median sales price in 2006 was $199,900. When expressed in 2017 dollars that is $241,495, significantly higher than the median sales price this June, $225,000. Interest rates, which averaged 6.7 percent 11 years ago, were 3.9 percent this June.

LePage says looking at the change in the typical payment over the past year shows it is misleading to only consider home prices when discussing affordability. In March 2017, the median home price was 5.9 percent higher than a year earlier in nominal terms, but the typical mortgage payment had risen 12.6 percent. This was largely because mortgage rates had increased one-half percentage point in that 12-month period.

CoreLogic's Home Price Index forecast suggests an increase in home prices of 3.3 percent in real terms over the next year and projections from IHS Markit are for mortgage rates, inflation, and household income to rise gradually. Using this information, LePage is predicting the inflation-adjusted typical mortgage payment will rise from $848 this past June to $983 over the following year, a 15.9 percent increase.