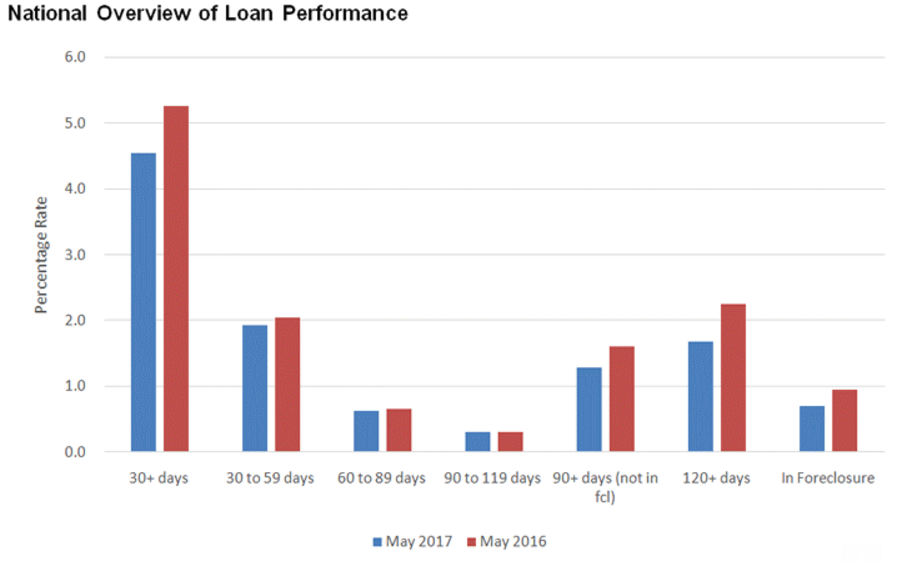

CoreLogic reported on Tuesday that the national mortgage delinquency rate in May was the lowest in nearly a decade. The company's Loan Performance Insights Report for the month shows 4.5 percent of outstanding mortgages were in some stage of delinquency, that is 30 or more days past due or in foreclosure. This is an 0.8 percentage point decline since May 2016 when the rate was 5.3 percent.

The rate for early-stage delinquencies, defined as 30-59 days past due, was 1.9 percent in May 2017, down from 2 percent in May 2016. CoreLogic said this is among the lowest rates of early-stage delinquencies in 17 years. The share of mortgages that were 60-89 days past due in May 2017 was 0.63 percent, down slightly from 0.66 percent in May 2016.

CoreLogic notes that early-stage delinquencies can be volatile so it also looks at transition rates. They too have declined. The share of mortgages that transitioned from current to 30-days past due was 0.8 percent in May 2017 down 0.1 percentage point from the previous May. As a reference point, in January 2007, just before the start of the financial crisis, the current-to-30-day transition rate was 1.2 percent and it peaked in November 2008 at 2 percent.

Two percent of mortgages nationwide were seriously delinquent, that is 90 days or more past due including loans in foreclosure. The rate was unchanged from the previous month, but down from 2.6 percent year-over-year. April and May tied for the lowest rate since November 2007 when it was also 2 percent.

As of May, 0.7 percent of active mortgages were in some stage of foreclosure, i.e. the foreclosure inventory rate. This is down from 1 percent in May 2016.

"Strong employment growth and home price increases have contributed to improved mortgage performance," said Dr. Frank Nothaft, chief economist for CoreLogic. "Early-stage delinquencies are hovering around 17-year lows, and the current-to-30-day past due transition rate remained low at 0.8 percent. However, the same positive economic conditions helping performance have also contributed to a lack of affordable supply, creating challenges for homebuyers."

"A prolonged period of relatively tight underwriting criteria has driven delinquencies down to pre-crisis levels across many parts of the country," said Frank Martell, president and CEO of CoreLogic. "As pressure to relax underwriting standards increases, the industry needs to proceed carefully and take progressive, sensible actions that protect hard-fought improvements in mortgage performance."

The highest delinquency rate was in Mississippi at 8.2 percent followed by Louisiana (7.6 percent), New Jersey (7.1 percent), New York (6.9 percent), and Alabama (6.3 percent). The foreclosure rate was highest in New York and New Jersey at 2.2 and 2.3 percent respectively, far ahead of third place Maine at 1.5 percent.