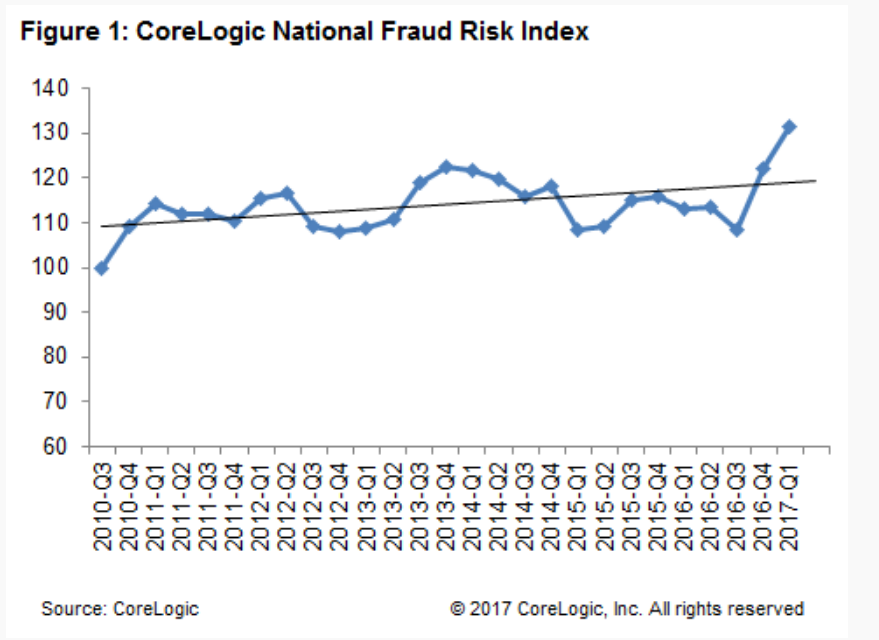

CoreLogic says conditions in the mortgage market are once again fertile ground for mortgage fraud. The company's National Fraud Risk Index hit a new high of 132 in the first quarter of this year versus 113 in the first quarter of 2016 and 122 in the fourth quarter.

Jacqueline Doty, executive, and product management for CoreLogic's Collateral Risk Solutions, reports in the company blog that hitting a "new high" isn't particularly momentous in this case, as the Index has only been around for a few years. It was established in 2010 after the high levels of fraud that existed during the housing boom had dropped along with mortgage volume. She said today's heightened number doesn't necessarily mean there is a lot more fraud occurring, just that conditions are present for it to increase.

The transition from a refinance to a purchase driven mortgage market it partially responsible for the more fraud friendly environment. Doty said there are more moving parts and players in a purchase transition and thus "more opportunities for financial gain...and for fraud."

Rapidly rising prices and competition among buyers is also contributing. More buyers are needing to stretch to qualify for a loan and CoreLogic has noted changes in the percentages of borrowers who report income that is high relative to their areas. Debt-to-income levels are also trending higher, another sign that applicants are pushing the outer limits of lending standards. "These conditions historically have supported fraud for housing schemes," Doty says.

She also warns lenders that one old fraud scheme seems to be coming back, and that, as usual, creative minds are thinking up new ones. The oldie-but-goody is one aimed at potential investors, usually from high cost states, who see what look like bargains outside of their local market. Home flippers pitch low-cost properties, often priced under $100,000 in more depressed areas such as the rust belt and try to convince the investors to buy sight unseen. They often accompany these pitches with offers to manage the property. They promise high returns of course; rewards that frequently are inflated.

The new scheme is might be termed inside-out occupancy misrepresentation. Instead of investors falsely claiming they plan to occupy the property on their mortgage application to qualify for special programs or get a lower interest rate, actual owner occupants are applying as investors and using future rental income to qualify for a loan. This scheme, Doty says, is gaining traction in New York and other large metro areas. With rental income non-existent, the homeowner may have problems keeping up with mortgage payments.