In April, the Mortgage Bankers Association (MBA) published its proposal for reform of the housing finance system. This week Mike Fratantoni, MBA's Chief Economist and Senior Vice President of Research and Economics, weighed in on the potential implications of that plan on the cost of mortgage credit.

Fratantoni says evaluating any such proposal must balance three major objectives; protecting taxpayers, attracting capitol to those who guarantee the loans or mortgage backed securities (MBS), and ensuring consumers and borrowers have access to affordable financing. For certain stakeholders, he says, the last is the most important consideration, but they should understand that a more stable system also will have benefits for consumers, ensuring access to financing even during unstable market periods. His review of the different components of reform that could impact costs lead him to conclude that costs under the MBA proposal will be quite similar to those in the mortgage market today.

There are six factors actively under debate that will impact consumer costs; a full faith and guarantee behind MBS, Guarantor capital requirements, return targets, and pricing behavior; mortgage insurance fund (MIF) premiums, affordable housing fees, the credit box, and capital requirements for MBS investors.

Full Faith and Credit Guarantee Behind MBS

Most of the above factors may contribute to higher consumer costs but those increases would likely be offset by an explicit government guarantee of MBS. Currently Ginnie Mae securities carry a higher price and lower rate than the GSE (Fannie Mae and Freddie Mac) MBS because the former carries a full faith and credit guarantee while the later are "explicitly" backed by the Treasury by dint of its Preferred Stock Purchase Agreements (PSPA). This is a small distinction but still leads to a marked difference in price.

The benefit to consumers from the value placed on the Ginnie Mae guarantees can be seen in the spread between rates on conventional verses FHA loans which has ranged from 10 to 40 basis points in recent years. While other factors have affected the spread, different prepayment speeds, default rates, etc. Figure 1 shows the value that investors place on the explicit guarantee, and the larger size of the conventional market, a move to an explicit guarantee might mean even larger reductions in consumer costs.

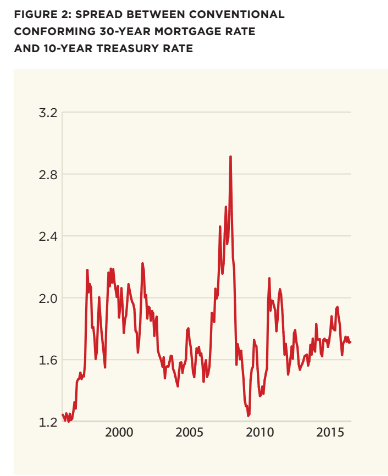

Fratantoni says the precise impact from "true" reform might be difficult to predict but reform through recap and release of the GSEs would lead to much higher consumer costs. Global investors have made clear they won't welcome a return to implicit guarantees and the resulting instability. This is shown in Figure 2, showing the spread between 30-year mortgage rates and 10-year Treasury notes. The spread nearly double during the housing crisis. "This is the instability that the MBA proposal seeks to solve for through a combination of sufficient private capital and an appropriately priced government backstop," he says.

Capital Requirements, Return Targets, and Pricing Behavior

MBA has proposed much more rigorous Guarantor capital requirements than were applied to the GSEs before the crisis, one that would be sufficient to survive a severe stress level of losses. It should also be consisted with the capital required for financial institutions that invest in mortgages. This should lead to consumer costs comparable to what is in the market today but higher than pre-crisis. Lower capitalization would lead to lower costs but a much less stable system.

Because of their duopoly position and the regulatory framework around them, the GSEs achieved above-market levels of return. A more competitive secondary market could lead to higher returns that would entice new entrants as would stable returns under utility-style regulation. In addition, ensuring a level playing field for lenders of all sizes and business models would support a dynamic and competitive primary market and competitive rates to consumers.

Several of the proposals under consideration would move guarantees from the implicit ones that support the GSEs to explicit ones behind the MBS. MBA proposes collecting premiums to pay for the Guarantee which, as it would be behind considerable private capital would need only to cover catastrophic risk, which is difficult to measure. MBA proposes the premiums be set at a reasonable level, allowed to build to an amount consistent to cover experienced levels of crisis. If premiums are set too low they might run dry in a significant crisis, requiring taxpayer support. If set too high they would needless add to consumer costs.

Affordable Housing Fees

MBA's proposal supports a fee on MBA to raise funds for affordable housing initiatives. The fee would need to address the large and growing needs of both owners and renters. But again, if set too high, would lead to higher costs and loss of access for those consumers who already barely qualify in the conventional market. Costs and benefits must be carefully balanced here.

The Credit Box

Subjecting Guarantors to a Qualified Mortgage type standard which sets eligibility for securitization would result in their setting underwriting standards and making pricing decisions consistent with prudent risk management. If the standard is set very conservatively, credit risk and consequently consumer costs might be lower than in the current market but access to credit could be unacceptably low in the eyes of many stakeholders. Alternatively, were there no eligibility standard and the market returned to one in which the GSEs set their own credit standards, with taxpayers on the hook for misjudgments, we might return to the unregulated array of products that led to the crisis and thus to higher costs for consumers. Fratantoni says, "Getting the balance right, such that the Guarantor credit box represents the provision of sustainable credit to qualified borrowers without being unduly restrictive, will be a challenging but worthy goal of reform."

Capital Requirements for MBS Investors

In addition to the differences between guarantees of Ginnie Mae securities and those of the GSEs, and by extension the lower rates for the FHA and VA loans in their Ginnie's pools, is their bank regulatory capital treatment. For risk-based capital purposes the Ginnie Mae MBS receive a 0 percent weight, the GSE MBS a 20 percent weight, even with the Treasury backstop behind the companies. Ginnie Mae's MBS are also considered high quality liquid assets for the liquidity coverage ratio test while the MBS from the GSEs don't quite meet this standard.

If, as MBA proposes, reform provides an explicit guarantee for MBS issued by Guarantors, and bank regulators change risk weights and liquidity treatment to align the GSE MBAs with those of Ginnie Mae today, that will also lower consumer costs. Again, given the much larger conventional market, this could lead to even lower consumer costs than those of FHA and VA.

Other Considerations

Fratantoni stresses that his analysis is about average pricing and that changes in any of the factors in that analysis could lead to differing changes for stronger versus weaker credit borrowers. It is critical to remember, however that the GSEs are not reaching many first-time homebuyers with their current pricing structure; FHA offers a more competitive all-in cost, even considering the GSEs' affordable housing initiatives

Conclusion

How consumer costs are impacted through housing finance reform will be determined by a lot of factors yet to be resolved through legislative debate. MBA expects the lower costs that result from an explicit guarantee behind MBS will offset at least most of the additional costs arising out of higher capital requirements, the MIF premium, and affordable housing fees. There will also be impacts from the business model of the guarantors which will carry with them required returns, credit standards, and changes to bank regulatory treatment of the GSEs' MBS Balancing taxpayer protection, investor returns, and consumer costs is critical to realizing a more stable housing finance system going forward.