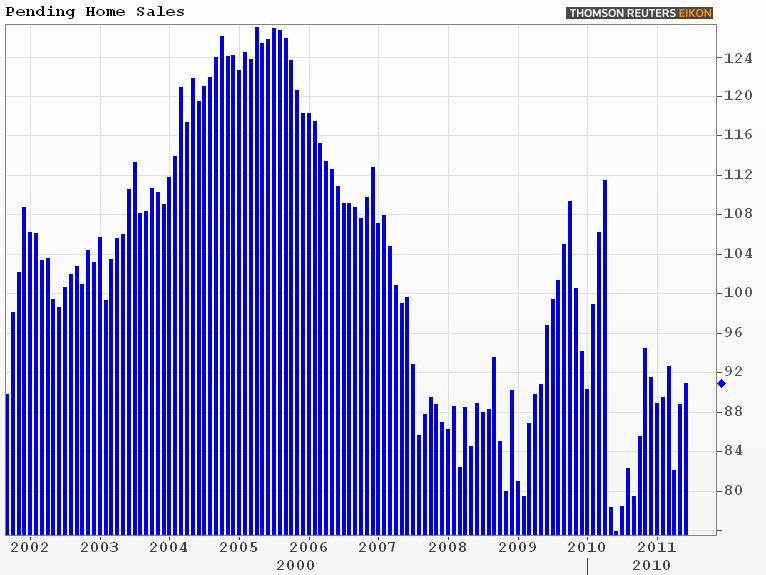

Pending real estate sales had another strong showing in June according to the Pending Home Sales Index (PHSI) released today by the National Association of Realtors® (NAR).

The Index, a forward-looking indicator based on home sales contracts, rose 2.4 percent to 90.9 in June, following an 8.2 percent increase to 88.8 in May. The June figure is 19.8 percent above the 75.9 percent number one year earlier, a trough period immediately following the expiration of the home buyer tax credit.

The PHSI is based on a large national sample, typically representing about 20 percent of transactions for existing-home sales. An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined as well as the first of five consecutive record years for existing-home sales; it coincides with a level that is historically healthy.

A sale is listed as pending when the contract has been signed but the

transaction has not closed and the Index generally assumed to be a predictor of

actual sales over the following one or two months as the contracts close. However, earlier this month NAR reported

there appeared to be an unusually high cancellation of contracts that were signed

in the spring and/or delays of closings.

June's existing home sales figures did not reflect the increases predicted

by the PHSI and were actually down compared to May.

On a regional basis, the Index fell

0.4 percent to 68.9 in the Northeast and 3.7 percent to 79.7 in the

Midwest. Both the South and the West

rose, the south by 4.4 percent to 99.2 and the West 6.4 percent to 107.0. All four regions showed strong improvement

over June 2010, a month that represented a nadir for home sales. The year-over-year change was 19.4 in the

Northeast, 26.4 percent in the Midwest, 19.2 percent in the South and 16.4

percent in the West.

Lawrence Yun, NAR chief economist, said there may be some increase in closed existing-home sales. "For the majority of transactions, the lag time between pending contacts to actual closings is one to two months. Therefore, the two consecutive months of rising activity should lead to overall improvement in closed sales in upcoming months," he said. "Though a higher than normal cancellation rate can hold back final closing figures, it could well be that some past cancellations are nothing more than delayed buying decisions rather than outright cancellations."

Yun said tight credit and economic uncertainty have been constricting the market. "The best way to ensure a more solid recovery in housing is to simply return to normal, sound credit standards so more creditworthy home buyers can get a mortgage," he said.

"Washington also should not rock the boat with policy changes that would negatively impact affordable credit or otherwise increase the cost of buying or owning a home," Yun added.

Existing-home sales this year are expected to total 5.0 million, slightly higher than 2010. Similarly, little change is forecast for aggregate home prices with several indicators, including NAR's median prices, showing recent signs of stabilization.

READ MORE: Home Sales Sag. Contract Cancellations Cited