Freddie Mac is projecting that 2017 will be another good year for multi-family housing. The company, a major presence in financing multifamily housing, released its Multifamily Mid-Year Outlook on Wednesday.

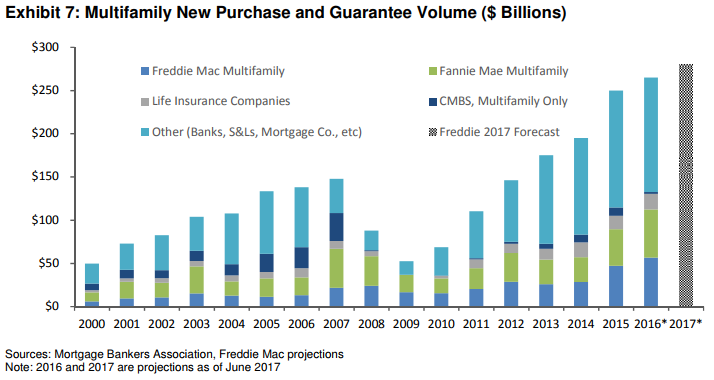

The Outlook, authored by Steve Guggenmos, Freddie Mac Multifamily vice president of research and Modeling, and Sara Hoffmann, predicts that the market will continue to grow for the remainder of this year and into the next. "Although the market will continue to moderate from cyclical highs," they say, "demand for rental housing units will remain steady. As a result, Freddie Mac is predicting that origination volume is likely to hit another record in 2017, reaching between $270 and $280 billion." That number, while a new high, is lower than the original forecast.

Higher interest rates and market uncertainty kept more investors on the sidelines during the first quarter of the year, but as interest rates stabilized and economic growth continued, investors have become more active.

Guggenmos and Hoffman see the number of multifamily construction projects peaking near the end of 2017 or in early 2018. This should result in higher vacancy rates, slower absorption of new units in some areas, and downward pressure on rent growth. This is already happening in some larger metro areas, they cite San Francisco, New York City, Washington, DC, and Miami. Still, it appears that two thirds of metro areas will end the year with vacancy rates lower than their historical averages. This will allow rents to continue to rise.

The larger economy has continued to support multifamily fundamentals. The labor market grew at a steady rate and outpaced population growth. Job growth was at an annual rate of 2.2 million last year and unemployment hit a 16 year low this June. Still, wage growth remains stubbornly low, although moving in the right direction. These factors have helped increase household formations, to 1.2 million in the first quarter of 2017. For the first time since 2006 more of those new households bought (854,000) than rented (365,000.) The homeownership rate has slowly increased from its cyclical low of 62.9 percent, reached in the second quarter of 2016, to 63.6 in the first quarter of this year.

Demand for rental housing slowed in general in the beginning of the year; 235,000 units (annualized) were absorbed, but that picked up to 280,000 in the second quarter, unchanged from the estimate for all of 2016. The current demographic drivers of the Millennial cohort, a more ethnically diverse population, and household preferences for rental housing all imply demand for rental units will continue, the authors say.

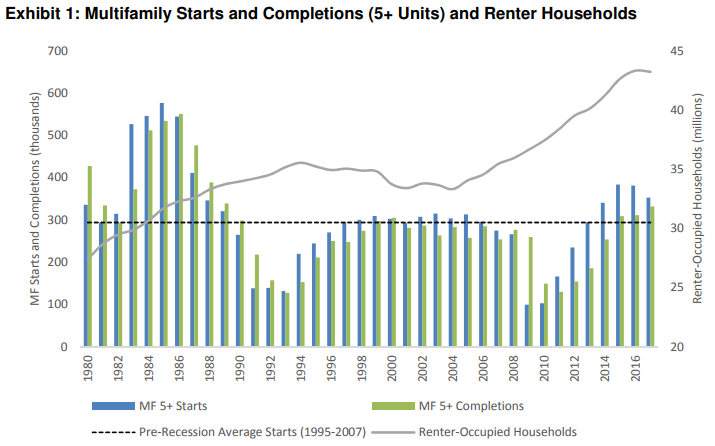

Multifamily permits and starts have been abating over the last two years, down 4 percent and 10 percent respectively while completions are expected to increase. There will be more units entering the market this year than at any time since the late 1980s. As of May, completions were at an annual rate of 330,000 units, a 6.7 percent annual increase and could rise higher "given that construction starts averaged 380,000 units each of the past two years, whereas completions averaged only 310,000 units each year." Those deliveries pushed vacancy rates slightly higher over the last few months although reports of the degree vary.

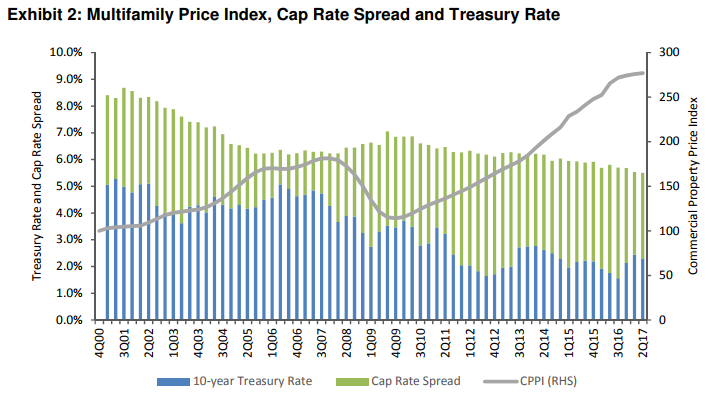

Both rents and property price growth moderated in the first party of the year, rents to 2.5 to 3 percent depending on the source, while property prices grew by 8 percent, the lowest since 2010. While moderating rents and vacancies had some impact on property prices, higher Treasury rates and overall market uncertainty also played a role.

Investment was tamped down late in 2016 by a spike in interest rates after the election and market uncertainty. Still, the authors expect, when final numbers come in, origination volume in 2016 will range from $265 billion to $270 billion, slightly higher than the Mortgage Bankers Association (MBA) projection of $260 billion.

Capitalization (cap) rates were flat through the first part of this year, at 5.5 percent as of April, and the recent interest rate spike did not cause an increase. The cap rate spread (difference between cap rates and 10-year Treasury) was a historically wide 410 basis points in third quarter 2016, and the interest rate increase was absorbed in that spread.

Freddie Mac expects the market to continue to grow in line with historical averages for the rest of the year and demand for units will stay strong due to lifestyle preferences and demographic trends. Delivery of new units should peak in the second half of the year and remain high into 2018 and will outpace demand in the short term so vacancy rates will grow, but more slowly than expected; that forecast has been lowered to 4.7 percent. This means rent growth will remain strong, exceeding the 2016 rate at the national level, and forecasts of higher wage growth will spur more housing demand.

Performance across metro areas will be varied. Those metros with below-historical average vacancy rates are better poised to absorb new supply whiles those with increased new supply and above-historical-average vacancy rates can expect slower absorption and potential negative impacts on multifamily fundamentals. Construction is slowing in some areas and increasing in others and rent growth will continue to be mixed.

On the debt side, multifamily origination volume is expected to grow throughout 2017. While the multifamily market continues to attract investments and capital, market uncertainty in the first part of the year may serve to lower full-year volume from earlier forecasts. Property prices are expected to grow, but more slowly than in the previous few years and with more moderation in large, higher-cost metro areas. Taking all these factors into account, the authors project origination volume to grow by 3 to 5 percent in 2017, to between $270 billion and $280 billion.