Two press releases that came out on Monday may point to a new direction for the residential construction market and perhaps for housing policy.

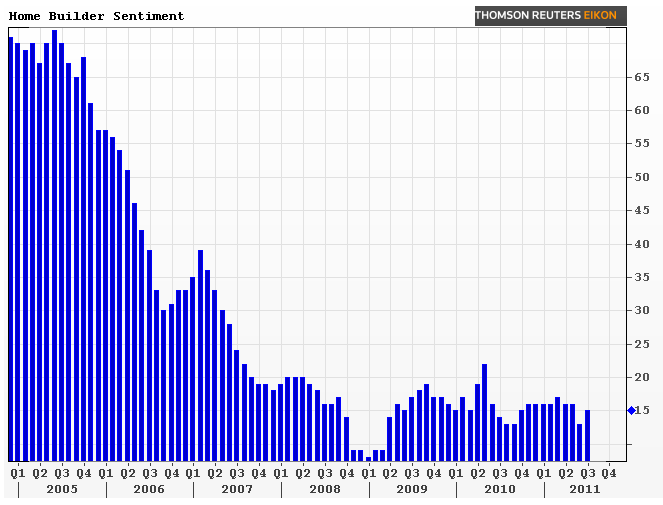

Home builders continue to have little optimism about the new home market according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI) for July. The index, floating near its bottom for since October 2008, did rise two points to 15 but this only partially recouped the three point drop seen in June.

The NAHB HPI is a composite index of home builder sentiment about the new home market. Builder members of the National Association of Home Builders (NAHB) are asked for their perceptions of both current single-family home sales and sales expectations for the next six months as "good," "fair" or "poor" and asks them to rate traffic of prospective buyers as "high to very high," "average" or "low to very low." Scores are used to calculate three component indices and the HPI, a seasonally adjusted index. Any number over 50 for the HPI and each of the components indicates that more builders view sales conditions as good than poor.

The component indices also rose slightly from their terrible June levels. The component gauging current sales conditions rose two points to 15 while the one measuring expectations for traffic over the next six months jumped seven points to 22. The component assessing prospective buyer traffic was unchanged at 12. On a regional basis, the Northeast declined two points to 15 but the Midwest was up one point to 12 and the South and West each gained three points to 17 and 14 respectively.

According to Bob Nielsen, chairman of NAHB, "The improvement in builder confidence in July is a positive sign that the outlook perhaps isn't quite as bleak as was feared in June. While builders continue to confront serious challenges with regard to competition from foreclosed properties that are priced below replacement cost, inaccurate appraisals of new homes, and a very restrictive lending environment for new home construction, select markets are showing gradual improvement as consumers begin to take advantage of very favorable buying conditions."

At the same time, the BuildFax Remodeling Index (BFRI) which tracks building permits and construction starts indicated that May had the highest level of remodeling activity since the Index was first introduced in 2004.

The BFRI is derived from building and permitting information from 4,000 cities and counties throughout the country assembled by BuildFax, a division of BUILDERadius. The BuildFax database currently covers over 60 percent of the US commercial and residential building stock.

The BFRI for May reveals that residential remodeling activity in May registered growth in every region of the country and signifies the 19th consecutive month of industry growth. According to BuildFax, the data demonstrate that many Americans are remodeling their current homes rather than purchasing new ones.

The May 2011 index was 124.3, the highest number ever. This was a 22 percent year-over-year increase. Each region increased month-over-month with the Northeast up 9.8 points (12%), the South up 7.3 points (7%), the Midwest up 16.3 points (18%), and the West up 8.7 points (7%). Even though the Midwest was up month-over-month, it continues to lag the other regions (as it has for the past three months) in year-over-year performance, down 10.6 points (11%) year-over-year. All other regions were up year-over-year, with the Northeast up 7.2 points (9%), the South up 9.5 points (10%), and the West up 20.7 points (21%).

Joe Emison, Vice President of Research and Development at BuildFax said of the index, "Even with the continued struggles in the economy, the remodeling industry has been a bright spot, as consumers look to make upgrades to their current homes, rather than purchasing a new residence. Based on the trends from the first months of this year, we expect to continue seeing strong gains from coast to coast."

So how does this have any bearing on housing policy? Housing starts continue to lag - the Census Bureau reports they were up 3.5 percent in June from May figures but were down almost an identical amount from June 2010. Builders are simply not going to build until the current inventories of new and existing homes return to more normal levels and the shadow inventory does not loom so ominously over the market.

If the emphasis were shifted from new construction to rehabilitating and improving existing housing stock it could provide a real jump start to the ailing construction industry. Remodeling dilapidated houses lacks the sex appeal of building yet another subdivision or condo complex as well as the economies of scale; but it also lacks the infrastructure costs, conservation headaches, and permitting delays. Returning some of the million plus "off market" vacant property to service as well as improving the stock of REO to useable/salable condition might, while creating construction jobs, also speed up the timeframe for reducing the inventory and returning the market to normal activity.

Adam Quinones, MND's Managing Editor, notes that the Department of Housing and Urban Development has already announced initiatives to rebuild the distressed housing stock. "With so many foreclosed properties sitting empty on the market we can expect remodeling and rehabbing to be a leading indicator of a bottom in the housing market. We already know there is a dearth of affordable rental housing available to low income renters. From that perspective, FHA should open its 203(k) program to investors if they want to accomplish their affordable housing goals."