Fannie Mae said it is sticking with its forecast for 2.0 percent economic growth in 2017, a projection it first made in February. The estimate of 2.1 percent growth in the first half of the year is expected by the company's economists to slow to 1.9 percent in the second half. Further, they say while housing won't drag on the economy this year, it won't make a huge contribution either, as inventories remain a problem.

The global outlook has improved and this helped to move Treasury yields higher; the 10-year rose about 25 basis points during the first few weeks of July. Improving growth abroad along with the 4 percent decline in the dollar so far this year, should help improve U.S. manufacturing and exports.

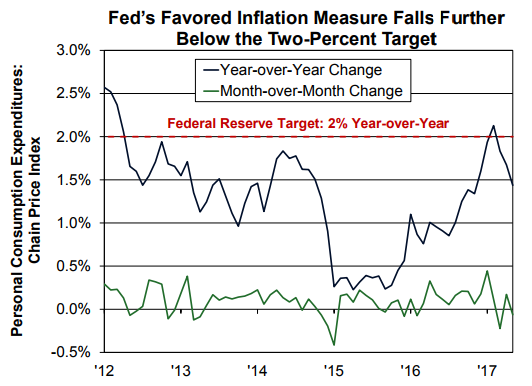

Fannie Mae's economic staff says the June Federal Reserve Open Market Committee (FOMC) meeting indicated no consensus among members as to when the Fed should start winding down its $4.5 trillion balance sheet. Some attendees thought a schedule should be announced "within a couple of months," while others wanted to wait until later to allow more time to assess the economic and inflation outlook. Inflation, as measured by the Personal Consumption Expenditures (PCE) deflator favored by the Fed, moved further away from the its 2.0 percent target. The PCE fell 0.1 percent in May, the second decline in the past three months, pushing annual inflation down to 1.4 percent. Fannie Mae now expects the Fed to announce its policy to taper the balance sheet in September and hike the fed funds rate once more this year, in December.

The economists call recent housing data, especially as regards homebuilding, "soft." Housing starts fell for the second time in three months in May, and permits were down for the third time. Multi-family starts, which drove residential building stats for some time, have declined for the last five months and are now 5 percent lower than the same time last year. Multi-family permits also declined in May. Single-family starts are still up 7 percent year-over-year. Fannie Mae says the multi-family slide reflects the maturing of the sector's expansion while the recent slowdown in single-family indicators might be payback for the warm weather boost construction got earlier in the year. New homes have been selling well and there has been a built-up in the number of permits authorized but not yet used.

Because of the recent weakness in the single-family sector, Fannie has revised their full-year projection for starts from the 9 percent annual gain they predicted in May to 6 percent. They still forecast only a slight decline in multi-family starts compared to 2016.

For the first time in more than a year there was a pull-back in private residential construction spending, reflecting both a downturn in units built and their average cost. After rising at a double-digit annualized pace in the first quarter, real residential investment likely fell modestly in the second quarter, dragging on GDP for the first time in three quarters.

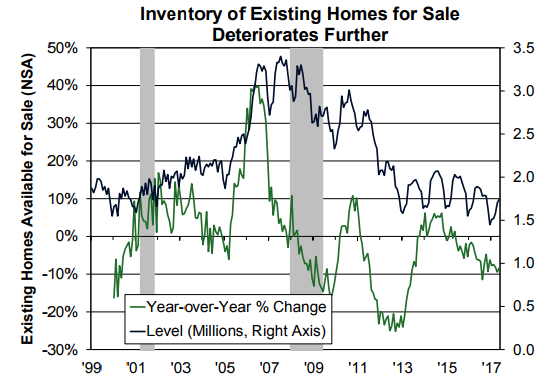

May brought increases in both new and existing home sales, but lack of inventory continues to constrain them. The inventory of existing homes is 8.4 percent below what was available a year earlier and has posted year-over-year declines since June 2015. The months' supply declined to 4.2 months from 4.7 months last May and the average marketing time set a fresh record low of 27 days, down from 29 days in April and 32 days a year earlier.

Average purchase mortgage applications rose for the fourth straight month in June. However, that conflicted with the other leading sales indicator, pending sales were down in May for the third consecutive month.

Those tight inventories continue to support home prices which are estimated to be rising along a range of 5.5 percent by Case-Shiller to 6.9 percent by the Federal Housing Finance Agency. Gains appear to be significantly stronger among lower-priced homes; CoreLogic found a 9.4 percent appreciation in their lowest price tier. Fannie Mae is now predicting prices will be up 5.8 percent for this calendar year.

The economists also predict that mortgage rates will continue to support housing demand through the rest of the year and that the 30-year fixed rate mortgage will average 4.1 percent in the fourth quarter. They revised slightly higher their forecast for purchase mortgage originations but left their refinance projections unchanged. As a result, they expect total single-family mortgage originations to drop about 20 percent in 2017 to $1.65 trillion, with a large decline in the refinance share from 48 percent in 2016 to 34 percent in 2017.