This month marks the tenth anniversary of the current expansion. How much longer can it last? Fannie Mae's July Economics Development report indicates it has a way to go, although likely at a slowing pace.

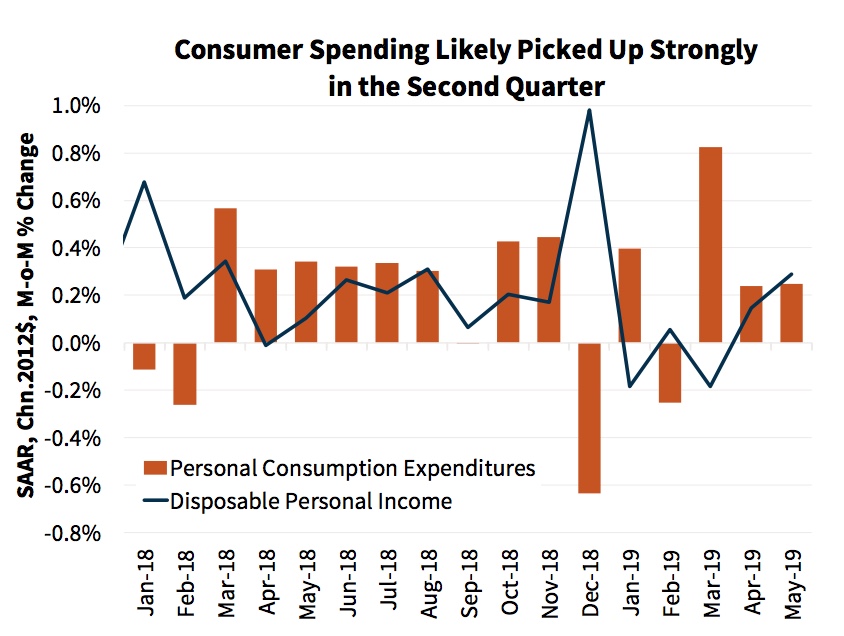

The second quarter of 2019 has just ended, but Fannie Mae's ESR Macroeconomic Forecast team expects that growth in real gross domestic product (GDP) probably slowed from the impressive 3.1 percent it posted in Q1. They upgraded last month's Q2 estimate by one-tenth based on higher expenditures for personal consumption, but still expect growth slowed to an annualized rate of 1.8 percent. They have maintained their previous full-year forecast for 2019 GDP of 2.1 percent. This will slow further next year to an estimated 1.6 percent due to waning fiscal stimulus, continued uncertainty weighing on consumer and business confidence, and eventually a slowdown in consumer spending.

Several key developments in the last month have affected the macroeconomy. Trade negotiations between the U.S. and China resumed after the G-20 summit in June, although tensions remain. Jobs rebounded in June after a weak May report, and both personal income and consumer spending remained solid.

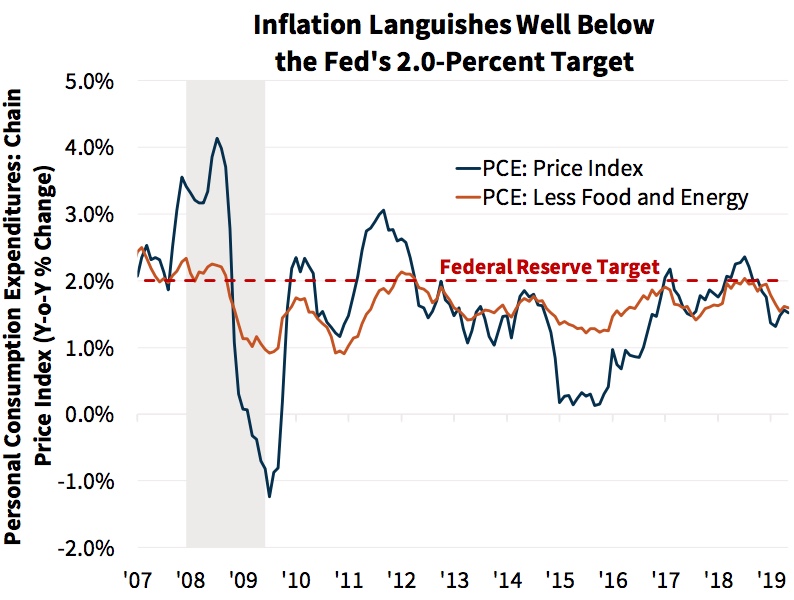

Against these positive developments is a reduction in the target 2.0 percent inflation projections announced at the Fed's June Open Market Committee (FOMC) meeting. The forecast for PCE inflation this year declined from 1.8 percent in March to 1.5 percent.

Testifying before Congress this month, Fed Chair Jerome Powell abandoned his earlier statements that the weak inflation numbers could be attributed to "transitory" factors and warned that low inflation risks were becoming more persistent.

All and all, Fannie Mae does not expect the Fed to be deterred from cutting the federal funds rate and they forecast quarter-point cuts in July and again in December, replacing an earlier prediction of a single cut in September.

The continued decline in mortgage rates during the second quarter and sustained strength in the labor market should support demand for home sales and construction. While recent housing data has been mixed, it is in part due to the lingering effects of last year's slowdown, including continued slow growth in new home building. Tempering the pace of the recovery is the limited housing supply which remains a chronic obstacle.

The inversion of the yield curve that began in late May has persisted; the 10-year/3-month Treasury spread was at 19 basis points when the report was written. The Fed has downplayed the inversion's importance as a recession predictor, but Fannie's economists say it is widely considered either a sign of overly tight monetary policy or of an expected slowdown in economic activity. It may, therefore, cause further erosion of business confidence and investment. In addition, the current environment of negative longer-term interest rates in many major economies contributes to downward pressure on longer-term rates in the U.S. as well. "The longer the inversion remains, the more likely that it will have direct real effects on growth via tighter bank lending, as banks find it increasingly difficult to profit from borrowing on the short end of the curve and lending on the long end," the Fannie Mae report says.

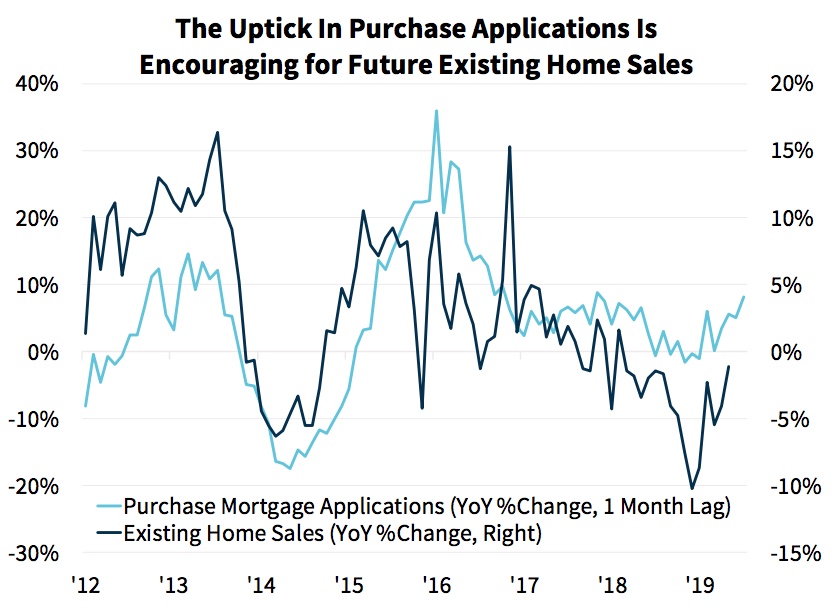

As forecast, new and existing home sales moved in opposite directions in May. Existing home sales increased 2.5 percent to the second-highest sales pace of the year. The company is holding to its second-quarter expectations that sales were up about 2.0 percent seasonally adjusted in the second quarter and will gain another 2.0 percent this quarter. Lower mortgage rates and a modest rise in inventories of homes for sale should help support an increase in existing sales.

Purchase mortgage applications have also continued to increase, indicating continued sales momentum during the last half of the year. Those sales are still likely to be tempered, even into 2020, by the chronically short supply of homes for sale, especially those in lower price tiers.

On the other hand, new single-family home sales were down for the second month in May after spiking earlier in the year to near highs for the recovery. That jump was aided in part by builder discounts which attempted to counter mounting inventories during the sales slump at the end of 2018. Much of that supply has been absorbed and Fannie Mae says it continues to view the underlying sales trend as modestly positive and expects a gradual increase in sales for the remainder of the year.

Single-family starts also fell in May and inventories have declined for four months. Permits for single-family construction rose 3.1 percent but this was the first month-over-month increase of the year and the largest since last September. The backlog of permits has risen for two straight months, so Fannie Mae expects starts to increase modestly over the next quarter, but probably faster than sales.

The slowdown in home price gains appears to be pausing, probably due to lower interest rates. The April S&P CoreLogic Case-Shiller Home Price Index measured annual house price growth at 3.5 percent, down only two-tenths from March. The CoreLogic National House Price Index, with a more recent reading from May, accelerated on an annual basis for the first time in fourteen months from 3.3 percent in April to 3.6 percent. Fannie Mae's forecast for house prices, as measured by the quarterly FHFA Purchase Only Index, calls for growth of 5.4 percent this year, up from its previous forecast of 4.6 percent. Deceleration to 3.7 percent is expected in 2020.

Multifamily construction has remained strong this year. Those starts are notoriously volatile, but the figure surged nearly 11 percent both in April and in May. While permits, which tend to be more stable, pulled back slightly in May, they remained near a one-year high. These developments have prompted a material revision in the forecast for multifamily starts last quarter and more increases for the remaining quarters of this year.

Mortgage rates have now declined for seven straight months and were at 3.75 percent when the report was written, the second-lowest level since November 2016 and more than a percentage point lower than their recent peak of 4.94 percent in November. The sustained decline and higher forecast for price growth have driven an increased forecast for single-family mortgage originations for the remainder of the year. The economic group now expects total originations to rise 7.0 percent from 2018 to $1.75 trillion and refinances to account for 32 percent of total mortgage originations in 2019, up from 29 percent in 2018.