From the Fannie Mae Release...

Fannie Mae announced today policy changes designed to encourage borrowers to work with their servicers and pursue alternatives to foreclosure.

Defaulting borrowers who walk-away and had the capacity to pay or did not complete a workout alternative in good faith will be ineligible for a new Fannie Mae-backed mortgage loan for a period of seven years from the date of foreclosure.

"We're taking these steps to highlight the importance of working with

your servicer," said Terence Edwards, executive vice president for

credit portfolio management. "Walking away from a mortgage is bad for

borrowers and bad for communities and our approach is meant to deter the

disturbing trend toward strategic defaulting. On the flip side,

borrowers facing hardship who make a good faith effort to resolve their

situation with their servicer will preserve the option to be considered

for a future Fannie Mae loan in a shorter period of time."

Fannie

Mae will also take legal action to recoup the outstanding mortgage debt

from borrowers who strategically default on their loans in

jurisdictions that allow for deficiency judgments. In an

announcement next month, the company will be instructing its servicers

to monitor delinquent loans facing foreclosure and put forth

recommendations for cases that warrant the pursuit of deficiency

judgments.

Troubled borrowers who work with their servicers, and provide information to help the servicer assess their situation, can be considered for foreclosure alternatives, such as a loan modification, a short sale, or a deed-in-lieu of foreclosure. A borrower with extenuating circumstances who works out one of these options with their servicer could be eligible for a new mortgage loan in three years and in as little as two years depending on the circumstances

Here is the verbiage from the FN Bulletin:

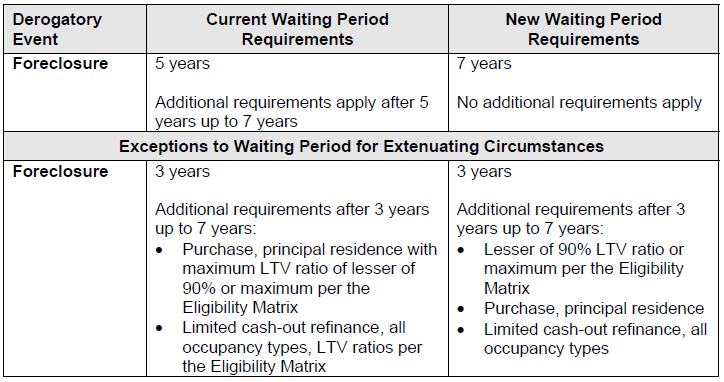

Currently, the waiting period that must elapse after a borrower experiences a foreclosure is seven years. However, Fannie Mae allows a shorter time period – five years – if certain additional requirements are met (e.g., minimum down payment and credit score, and occupancy requirements).

These requirements are being modified to remove the five year option. Unless the foreclosure was the result of documented extenuating circumstances, which only requires a three-year waiting period (with additional requirements), all borrowers will now be required to meet a seven-year waiting period after a prior foreclosure to be eligible for a new mortgage loan eligible for sale to Fannie Mae"

Don't miss the section that says borrowers who have extenuating circumstances may be eligible for new loan in a shorter timeframe.