The Mortgage Bankers Association (MBA) today released its Weekly Mortgage Applications Survey for the week ending June 18, 2010.

The Mortgage Bankers Association application survey covers over 50% of all US residential mortgage loan applications taken by mortgage bankers, commercial banks, and thrifts. The data gives economists a look into consumer demand for mortgage loans. In a low mortgage rate environment, a trend of increasing refinance applications implies consumers are seeking out a lower monthly payment which can increase disposable income and consumer spending (or give consumers a chance to pay down other debts like credit cards). A falling trend of purchase applications indicates a decline in home buying interest, a negative for the housing industry and the economy as a whole.

Excerpts from the Release...

The Market Composite Index, a measure of mortgage loan application volume, decreased 5.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 6.0 percent compared with the previous week. The four week moving average for the seasonally adjusted Market Index is

down 0.5 percent.

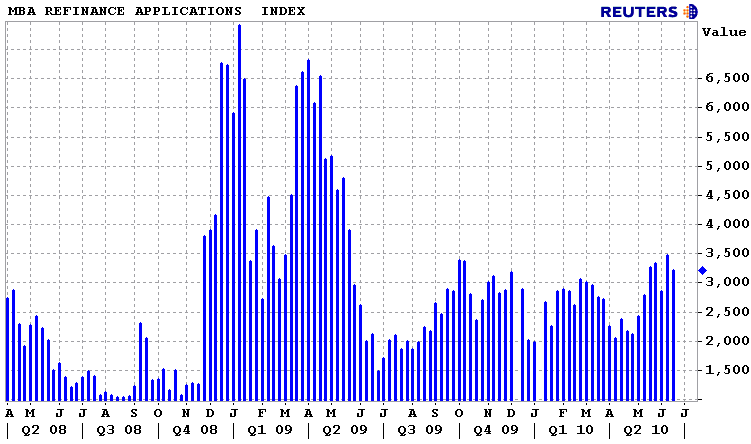

The Refinance Index decreased 7.3 percent from the previous week. The four week moving average is down 0.4 percent for the

Refinance Index. The refinance share of mortgage activity decreased to 73.8 percent of

total applications from 74.8 percent the previous week.

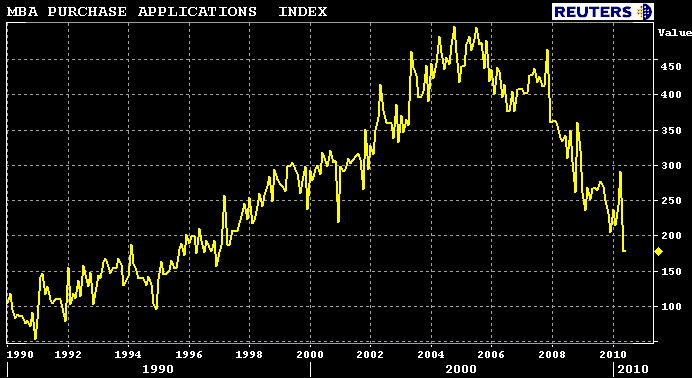

The seasonally adjusted Purchase Index decreased 1.2 percent from one week earlier. The unadjusted Purchase Index decreased 2.3 percent compared with the previous week and was 36.8 percent lower than the same week one year ago. The four week moving average is down 1.1 percent for the seasonally

adjusted Purchase Index.

The decline in total purchase applications was driven by a 4.4 percent decrease in government applications, while conventional purchase applications increased by 1.0 percent.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.75 percent from 4.82 percent, with points increasing to 1.07 from 0.89 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. This is the lowest 30-year contract rate observed in the survey since the week ending May 15, 2009. The effective rate also decreased from last week.

The average contract interest rate for 15-year fixed-rate mortgages decreased to 4.19 percent from 4.23 percent, with points increasing to 1.00 from 0.83 (including the origination fee) for 80 percent LTV loans. Due to the increase in points, the effective rate is unchanged from last week.

The average contract interest rate for one-year ARMs decreased to 7.05 percent from 7.07 percent, with points remaining constant at 0.27 (including the origination fee) for 80 percent LTV loans. The adjustable-rate mortgage (ARM) share of activity decreased to 4.9

percent from 5.2 percent of total applications from the previous week.

Last week the MBA survey told us that refinance apps improved as lenders were passing along lower consumer borrowing costs via a reduction in origination and discount fees. In the data released today, we learned that mortgage rates fell but lenders increased closing costs. Although mortgage rates improved, the change in total consumer borrowing costs did not create enough incentive for borrowers to re-apply at a new lender. (plus borrowers have less disposable income to put down at the closing table)

The uptick in refinance demand seen last week looks to have stolen demand from this week. READ MORE