Global equities are rallying and the U.S. is no exception.

Ninety minutes before the opening bell, Dow futures are up 80 points to 10,77 and S&P 500 Futures are 9.50 points higher at 1,098.75. Last week, the Dow climbed 2.81% and the S&P rose 2.51%.

The 2-year Treasury note yield is 3.6 basis points higher at 0.77% and the 10-year Treasury note yield is up 7.5 basis at 3.31%.

Also, WTI crude oil is up $1.62 to $ 75.40 per barrel and Spot Gold is up $0.65 to $1,227.35.

The Week Ahead

Monday:

Morning ― James Bullard, president of the St. Louis Federal Reserve, speaks in Tokyo at the Institute of Regulation and Risk of North Asia.

Treasury Auctions:

- 11:30 ― 3-Month Bills

- 11:30 ― 6-Month Bills

Tuesday:

6:15 ― James Bullard, president of the St. Louis Federal Reserve, speaks on asset bubbles, in Hong Kong, at the Institute of Regulation and Risk of North Asia

8:30 ― The Empire Fed Manufacturing Index, the first regional report on the sector to be released each month, is expected to continue expanding for the 11th straight month in June. Last month, the index dropped more than 11 points but remained healthy at 19.1; in June economists are looking for a 21.0 score, which would provide confirmation that manufacturing is leading the economic recovery.

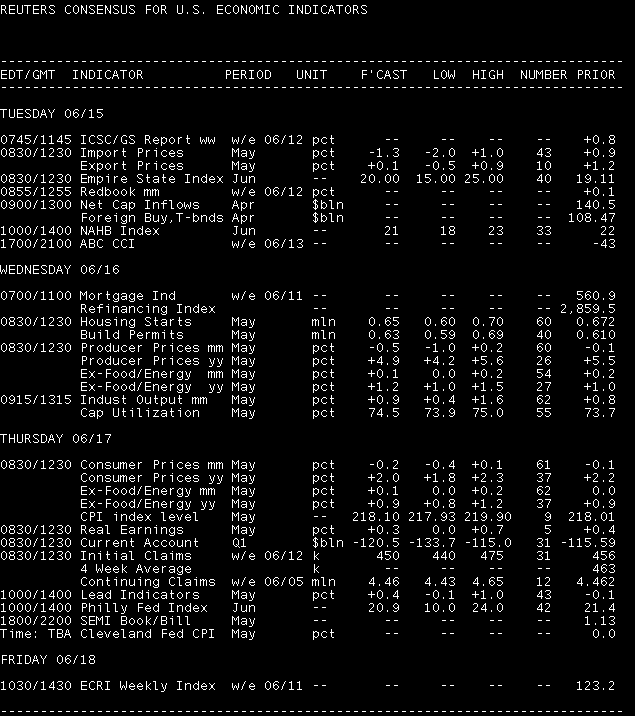

Economists at Nomura described the 11-point drop last month as a “temporary setback. However, if the index fails to recover ― and if confirmed in the Philly Fed index later this week ― it could suggest that the manufacturing recovery is starting to slow.”

9:00 ― The Treasury International Capital or TIC Flows report ― a measure of the flows of financial instruments into and out of the country ― improved significantly across the board in March as the Eurozone debt crisis prompted a flight-to-quality away from Europe and towards the U.S. Total TIC flows were way above expectations at $140.5 billion, “almost a threefold increase from the prior month, which is a series record,” according to economists at TD Securities.

For the April report, economists at Nomura anticipate more of the same.

“We expect that the ongoing sovereign debt crisis in Europe, as well as a structural shift out of euro-denominated assets, was behind the turn,” they argued in a weekly note. “Given that the spike in global risk aversion did not begin until early May, this week's April data should echo the March results.”

10:00 ― The Housing Market Index is a measure of homebuilder sentiment compiled by the National Association of Home Builders. Last month it rose three points to 22 last month, beating the consensus forecasts, yes, but not signalling any real optimism. The range of the index is from 0 to 100, suggesting that deep pessimism continues to reign despite hitting the highest level since August 2007. The index has been below the 50 threshold since May 2006.

No consensus from economists is available, but analysts at IHS Global Insight said to look for a decline after single-family housing permits for construction dropped 10% in April.

“We expect this decline to be reflected in May's single-family housing starts — with total housing starts dropping about 9% to a 610,000 annual rate,” they predicted. “We are also expecting another double-digit drop in single-family permits, further payback for the tax credit, and for permits to drop to a 563,000 annual rate.”

Treasury Auctions:

- 4-Week Bills

Wednesday:

8:30 ― Housing Starts ― or new construction of single-family homes ― are anticipated to fall in May after building permits contracted 11.5%. In April, the annual pace of starts increased almost 6% to 672k, while in May they are expected to come in at 650k. The expected decline follow two months of substantial month-t0-month growth, but aside from those months the level of starts had hardly budged since February 2009.

“Inventories of new homes are at historically low levels and builders’ confidence has improved, but the excess supply of existing homes and less than robust demand will keep many builders’ tools in the tool shed,” said economists at BBVA. “The recent pick-up in housing starts in recent months points to recovery. Nevertheless, economic conditions indicate that the recovery will be slow.”

Economists at Nomura added: “Housing starts and building permits diverged in April, with starts increasing by 10% m-o-m but permits falling by 10%. We expect the opposite pattern in May, with starts cooling but permits rebounding sharply. We forecast a 62.5% decline in starts to an annualized rate of 655,000 units, and a 10.7% increase in building permits to an annualized rate of 675,000 units.”

8:30 ― Falling gasoline prices are expected to push the Producer Price Index into a state of month-to-month deflation in May. Economists look for headline prices to be slashed by 0.5% in the month, falling a 0.1% drawback in April and a 0.7% increase in March. Core prices, which exclude food and energy costs, are anticipated to rise 0.1% following upticks of 0.2% and 0.1% in the prior two months.

“Unlike other measures of core inflation, growth in the core PPI has actually accelerated in recent months,” noted economists at Nomura. “This is especially evident when one strips out the volatile vehicle and tobacco components. This likely reflects pass-through into finished goods prices from the rise in commodity prices, particularly metals. Importantly, the PPI does not include any services prices, which are a key factor in the ongoing weakness in the CPI.”

9:15 ― After climbing by a healthy 0.8% in April, Industrial Production is expected to advance by 1.0% in May. Optimistic predictions are based largely on the strength of the nationwide ISM Manufacturing survey, which hit a six-year high in April before moderating slightly in May. Also, the ISM’s employment index hit its second highest reading in 26 years.

“The re-stocking process is driving manufacturing production sharply higher,” said economist at IHS Global Insight. “Manufacturing hours surged 1.0%, electricity production rebounded on warmer weather, and motor vehicle production rose to its highest level in twenty months.”

Analysts at BBVA added that the ISM survey results should translate into “a significant improvement in industrial production.” They said inventory adjustment and a more solid financial footing were playing a role in the expansion, plus greater financing opportunities and improved confidence among businesses.

“A positive surprise in Wednesday’s data would be a signal that business investment is picking up and that private demand is firming outside of fiscal stimulus,” they wrote.

2:15 ― Charles Plosser, president of the Philly Fed, speaks on a panel on fixing the financial system in New York.

Thursday:

8:30 ― The Consumer Price Index should be less impacted by oil prices than the producer price index, but the direction is expected to be the same. Prices are set to fall 0.2% in May after a 0.1% cut in April, while core prices are set to rise 0.1% after a flat reading. In sum: the threat of inflation remains benign, allowing the central bank to keep interest rates low.

“Pump prices normally rise sharply at this time of year, but we estimate that they fell slightly in dollar terms in May, which should translate into a 6.3% seasonally adjusted decline. That alone takes 0.3 percentage point off the CPI,” said economists at IHS Global Insight. “The overall CPI decline should be moderated by rising food prices and by a modest 0.1% increase in core prices. Core prices have moved little in recent months, as retailers find consumers reluctant to buy without a price incentive.”

8:30 ― Initial Jobless Claims have been levitating above the 450k range for the entire calendar year so far, disappointing many who assumed the downward trend begun in Q4 last year would continue steadily. Economists are hoping for a 450k figure in the week ending June 17, which is 6k below the prior week’s level.

“Initial jobless claims declined slightly last week but in general have failed to improve much over the last two months. This may indicate that the hiring recovery is proceeding slowly,” said economists at Nomura.

Continuing claims ― a tally of those still receiving unemployment benefits ― fell to 4.462 million in the final week of May, marking the lowest level since late 2008.

10:00 ― Leading Economic Indicators surprised some by breaking a 12-month growth streak in April. But the fall was only by 0.1%, and in May the index is expected to rise by 0.6%, more than erasing the temporary drawback and building upon the 1.3% jump in March.

“An increase in average weekly hours, slightly lower jobless claims, as well as the upward sloping yield curve should contribute positively to the index,” said economists at Nomura. “This may be partially offset by lower stock prices and a small decline in the ISM's vendor performance index. In contrast to the Conference Board's measure, the ECRI weekly leading index has recently turned sharply lower, pointing to slower growth later this year.”

10:00 ― Following the Empire State Survey on Tuesday, the Philly Fed Survey is expected to remain firmly in growth mode in June. The anticipated level is 20.0, or 1.4 points below the headline in May. Estimates range widely from 13.8 to 21.5 ― the low estimates largely result from the new order index dropping to 6.1 from 13.9 last month.

"The Philly Fed index edged higher in May to the second highest reading of this cycle,” said economists at Nomura. “While expect that the region's manufacturing sector will continue to grow, the exceptionally fast pace of growth should begin to slow, in our view. We therefore forecast a decline in the index to 20.0 in June.”

11:00 ― The Treasury announces terms of the following week’s 2-, 5- and 7-year note auctions.

Friday:

No significant data.