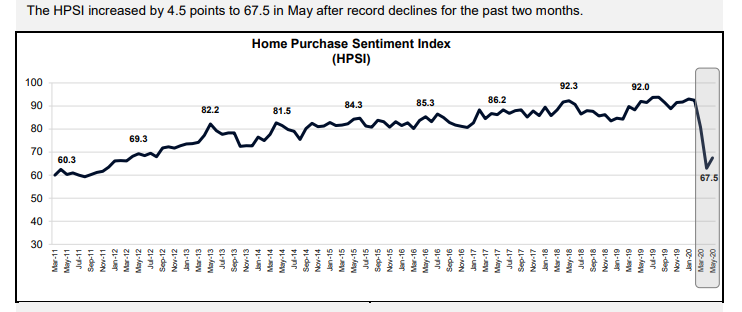

After falling an aggregate of 29.5 points in March and April, Fannie Mae says its Home Purchase Sentiment Index (HPSI) has begun to recover. The Index rose 4.5 points in May to 67.5 from an all-time survey low in April. Four of the six index components gained ground. Year over year, the HPSI is down 24.5 points.

Consumers reported a somewhat more optimistic view of homebuying conditions and, to a lesser extent home-selling conditions, in their responses to the National Housing Survey upon which the index is based. Moreover, fewer consumers reported expectations that mortgage rates will go up over the next 12 months.

"Although the HPSI's precipitous declines of March and April did not continue in May, Americans' financial, economic, and housing market concerns remain substantially elevated compared to survey history," said Doug Duncan, Senior Vice President and Chief Economist. "Low mortgage rates have helped cushion some of the impact of the pandemic on consumer sentiment regarding whether it's a good time to buy a home, which picked back up this month to late-2018 levels. Although weakened income perceptions and continuing job loss concerns, particularly among renters, are likely weighing on many would-be buyers, purchase mortgage applications have returned to mid-March levels when pandemic response measures began ramping up. Home-selling sentiment remains severely dampened due primarily to economic concerns, though increased purchase activity may improve the confidence of some potential sellers. As lockdown restrictions begin to ease across the country, we expect economic recovery to be largely shaped by consumers' decisions regarding when and how to reengage in the economy. We believe this month's HPSI results and Friday's unexpectedly favorable labor market report to be encouraging signs for the months ahead."

The percentage of Americans who say it is a good time to buy a home increased from 48 percent to 52 percent, while the percentage who say it is a bad time to buy decreased from 46 percent to 39 percent. As a result, the net share of Americans who say it is a good time to buy increased 11 percentage points to 13 percent.

Those who view this as a good time to sell a home increased from 29 percent to 32 percent while "bad time" responses fell 3 points to 62 percent. This put the net of those who say it is a good time to sell at a negative 30 percent compared to -36 percent in April.

The percentage of Americans who say home prices will go up in the next 12 months increased this month from 23 percent to 26 percent, while the percentage who said home prices will go down gained 1 point to 35 percent and those who expect no change decreased from 36 percent to 30 percent. As a result, the net share of Americans who say home prices will go up was 2 percentage points higher than in April.

The net share of Americans who think mortgage rates will move lower over the next year rose 10 points to 0.0 percent. In May 2019 that net was -37 percent. Only a quarter of respondents expect rates to rise.

The two index components that did not gain ground deal with job security and household income. The percentage of Americans who say they are not concerned about losing their job in the next 12 months decreased from 76 percent to 75 percent, while the percentage who say they are concerned increased from 23 percent to 24 percent leaving a net share of those not concerned down 2 points at 51 percent.

The percentage of Americans who say their household income is significantly higher than it was 12 months ago decreased from 20 percent to 18 percent, while 19 percent said it was lower and 61 percent reported it as unchanged. This put the net reporting significantly higher income at -1 percent.

While it is not an index component, survey respondents are asked each month whether the economy is on the right or the wrong track. In February 60 percent said it was the right track. In May only 29 percent thought that was the case while 60 percent said the economy was headed in the wrong direction.

The National Housing Survey from which the HPSI is constructed, is conducted monthly by telephone among 1,000 consumers, both homeowners and renters. In addition to the six questions that are the framework of the index, respondents are asked questions about the economy, personal finances, attitudes about getting a mortgage, and questions to track attitudinal shifts.