This may, or may not be a cause for celebration. The New York Federal Reserve Bank, using credit data from Equifax, reports that Americans are now back to owing as much money as they did before the housing crash.

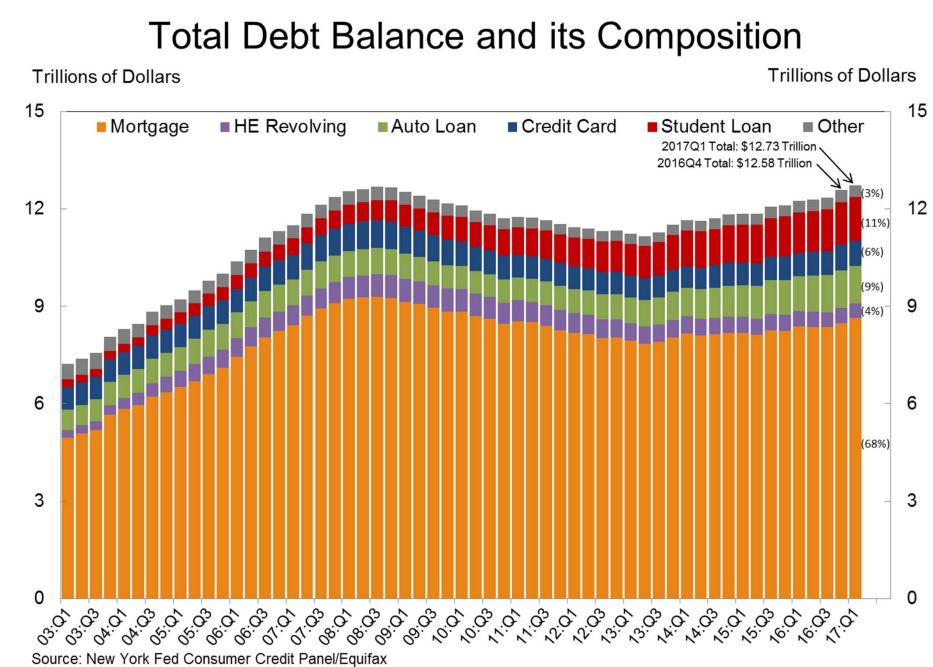

Aggregate household debt rose for the 11th consecutive time in the first quarter of 2017, reaching a total of $12.73 trillion at the end of March. This is an increase of $149 billion or 1.2 percent from the fourth quarter of 2016, and surpasses the prior peak level of $12.68 reached in the third quarter of 2008.

Household indebtedness hit the bottom of this economic cycle in the second quarter of 2013 at around $11 trillion. The most recent number represents a 14.1 percent increase from that trough.

The largest component of household debt is home mortgages. That balance also increased, rising quarter-over-quarter by $417 billion to $863 trillion and making up 68 percent of total household indebtedness

In addition to mortgage debt, another 3 percent of household debt is in the form of home equity loans (HELOCs). Balances on those loans declined by 17 billion in the first quarter, to a total of $456 billion.

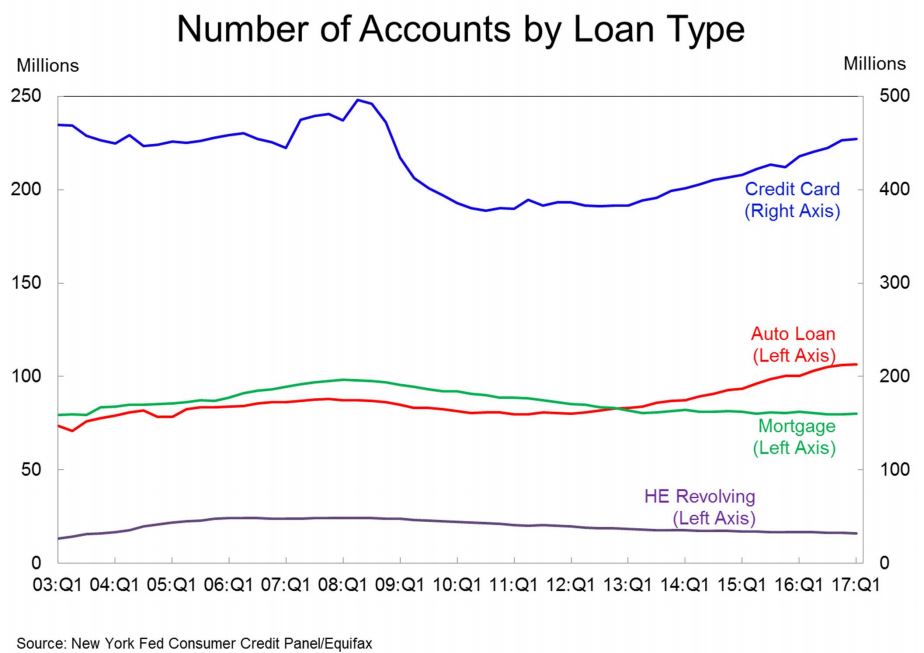

Even though it constitutes, by far, the largest dollar amount of debt, the number of mortgage loans is dwarfed by credit card accounts. There appears, from the chart below, to be about 85 million active mortgages while open credit cards number over 450 million.

The number of mortgage originations are based on new accounts appearing on credit reports. Experian data indicates an origination volume of about $491 billion, down from $617 billion in the fourth quarter. Both numbers include refinances. Aggregate HELOC limits declined by $19 billion.

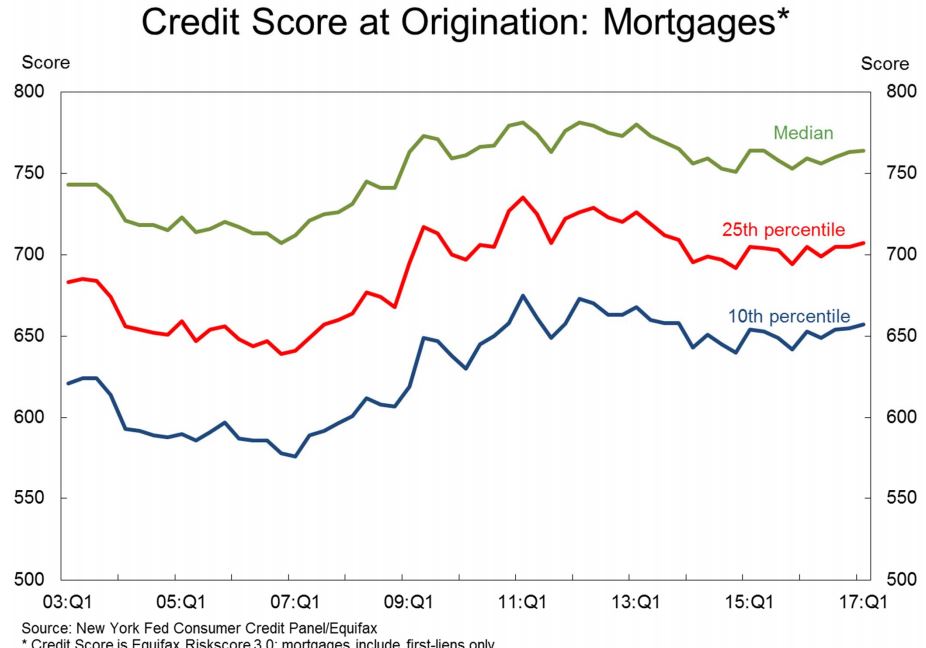

Credit scores for new mortgages rose to a median of 764. Originations with credit scores under 660 were down while those over 720 increased considerably.

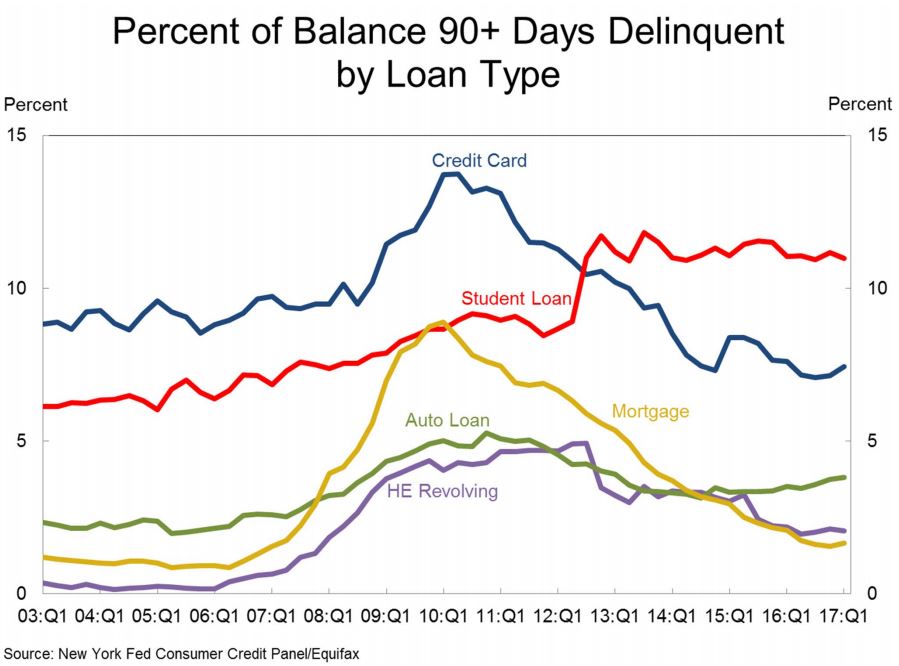

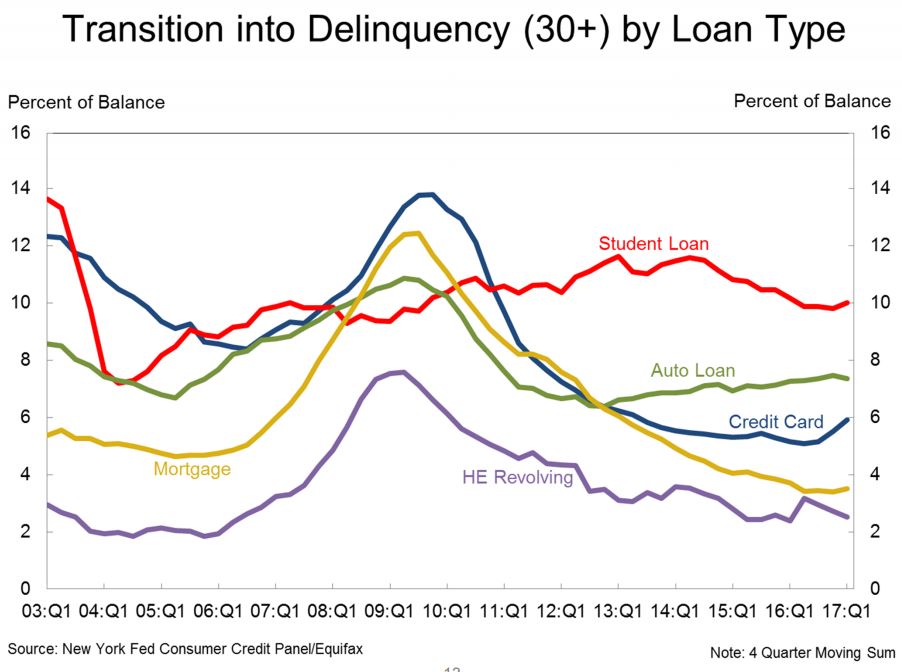

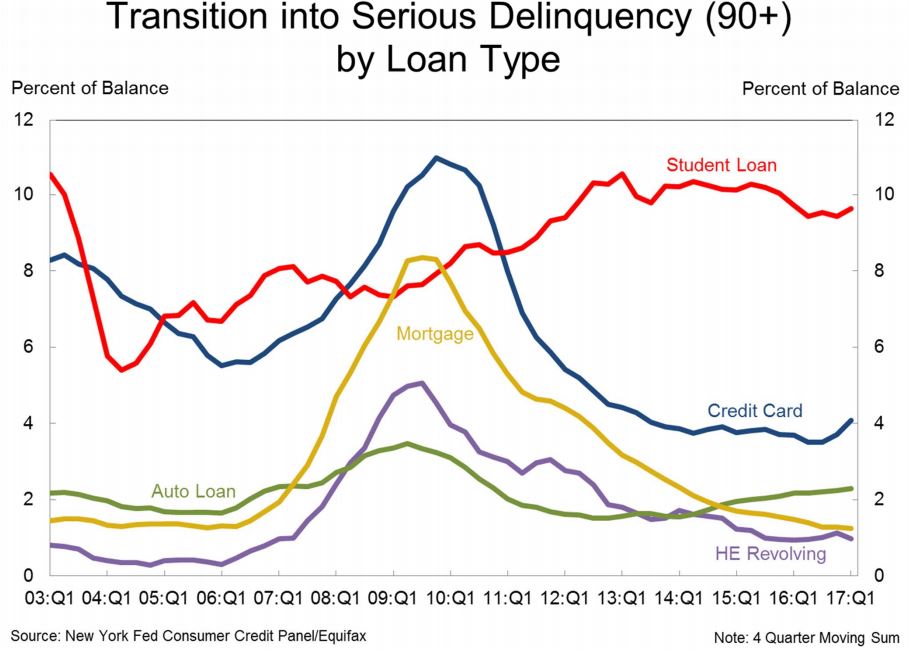

As of March 31, there was $615 billion in debt of all kinds that was delinquent, a rate of 4.8 percent. Of that figure $426 billion is seriously delinquent or severely derogatory, that is at least 90 days late. Serious delinquencies of both mortgages and HELOCs were well below those of other loans types, student loans hover around 12 percent, although mortgages had a slight uptick to 1.7 percent in the serious category during the first quarter.

Mortgages and HELOCS are also transitioning into delinquency at a relatively low rate. One percent of current mortgage balances transitioned to early delinquency. Of mortgages in early delinquency, 18% transitioned to 90+ days delinquent, while 36% became current.

About 91,000 individuals had a new foreclosure notation added to their credit reports between January 1 and March 31st, an increase since the fourth quarter, although foreclosures remain low by historical standards.