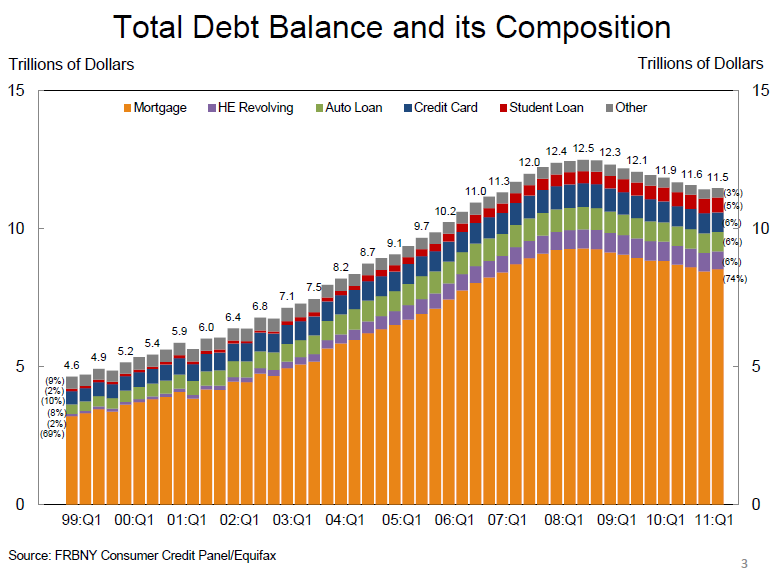

America's household debt level ticked upward for the first time in 10 quarters during the first three months of 2011 according to a report released by the Federal Reserve Bank of New York. Households, which had reduced debt by more than $1.03 trillion since its peak level of $12.5 trillion in Q3 2008, added $33 billion (0.3 percent) to the total debt tally during the first quarter of 2011.

Much of the increase was due to a fractional uptick in mortgage and home equity lines of credit (HELOC), which comprise 74 percent of the nation's debt burden. Despite the slight increase, mortgage debt and HELOC obligations are down from 2008 peaks by 8.1 percent and 9.9 percent respectively.

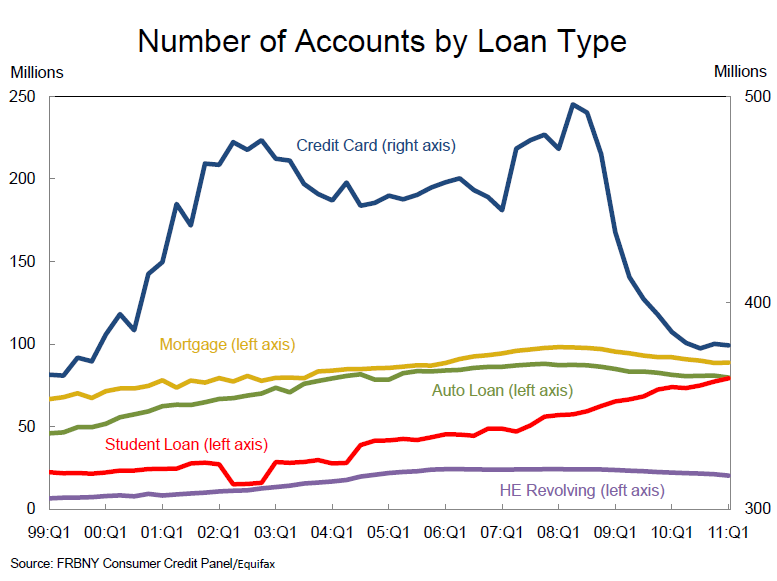

Other forms of consumer debt fell by $30 billion or about 1 percent during the quarter. Non-real estate debt is now $2.29 trillion, a decline of 9.6 percent from the Q4 2008 peak. Credit card limits increased slightly for the first time in 10 quarters while the number of open credit card accounts remained level at around 379 million. At the peak, almost 500 million credit cards were in use and 270 million accounts have been closed against about 160 million new accounts opened. Balances on outstanding credit card accounts are about 20 percent below peak levels.

While credit card accounts have plummeted in number since the start of the recession and the count of mortgages, HELOCs and auto loans have remained relatively unchanged, the number of student loans has continued to climb, increasing by about 50 percent since Q1 of 2008. The number of credit account inquiries within six months, an indicator of consumer credit demand, fell 3.5 percent after a string of three consecutive increases.

Total household delinquency rates continued to decline. As of March 31, 10.5 percent of outstanding debt was in some stage of delinquency, down from 10.8 percent at the end of the fourth quarter of 2010 and 11.9 percent a year ago. This was the fifth consecutive quarter the delinquency rate shrunk. About $1.2 trillion of consumer debt is currently delinquent and $890 billion is at least 90 days overdue. Both of these measures of delinquency have declined by 15 percent year-over-year.

Some 2.4 percent of mortgage balances that were current at the beginning of the quarter had transitioned into delinquency by the end; the second straight quarter this measure improved. The roll from early to serious delinquency also slowed to 28 percent from 30 percent. This is the lowest roll rate since the third quarter of 2003. There was also an increase in the cure rate - former delinquent loans that become current - to 32 percent from around 25 percent in mid 2010.

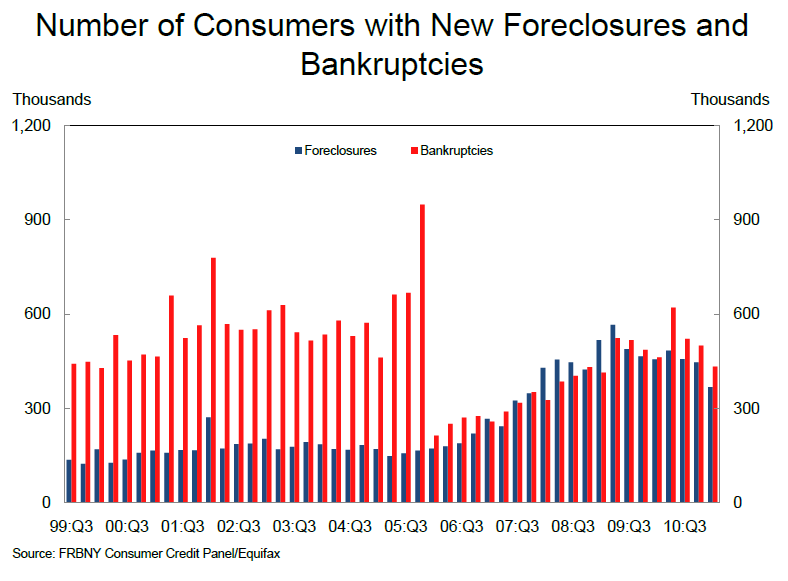

New foreclosures which the Federal Reserve defines as the number of individuals rather than properties receiving a first foreclosure notice, numbered around 368,000, a 17.7 percent decrease from the fourth quarter level. This number is a little hard to assess as a person with foreclosures on two loans (even if filed during different quarters) would be counted only once while a property with two owners would be counted twice.

Arizona, California, Florida, and Nevada have the nation's highest delinquency and foreclosure rates but the Fed notes that their rates are falling faster on average than in the other states. An exception is Nevada where new bankruptcies and foreclosures are dropping but general measures of delinquencies continue to soar.

New bankruptcies appeared on the credit reports of 434,000 individuals compared to 500,000 in the previous quarter, a decrease of 13.3 percent. New bankruptcies were down 6.4 percent from the level one year earlier.