Given how critical first-time homebuyers are to the housing system the Urban Institute says it is important to accurately measure how present they are in the market. The National Association of Realtors® (NAR) has consistently said that such homebuyers typically represent 40 percent of buyers in a healthy market and has reported the share as remaining below this mark since mid-2010. In a House Policy Research Center brief for the Institute, The Urban Institutes Housing Finance Policy Center Director Laurie Goodman and fellow researchers Bing Bai and Jun Zhu contend that the widely accepted measures of the percentage of first-time buyers such as those provided by NAR "are overbroad and sometimes misleading."

Until recently loan-level data was not available on most of the largest group of mortgages loans, those backed by FHA and the two government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac. While Freddie Mac began publicly providing loan-level data in 2005 the same was not true of Fannie Mae and Ginnie Mae (which securitizes FHA loans) until 2013 and such data is still not available from FHA itself. The authors based their work on complete loan-level single-family purchase-money mortgage data from the GSEs and Ginnie Mae combined with estimates reported by FHFA and the FHA to review the trend in first-time homebuyer shares over the past 14 years.

According to the data about one-quarter of GSE-guaranteed mortgages originated between 2001 and 2003 were made to first-time buyers for a home purchase. This percentage grew steadily through the housing boom to 42 percent in 2007. This was followed in 2008 by a spike in home refinancing that lasted four years and dropped the first-time homebuyer share of mortgages to 38 percent by 2012 except for 2009 and 2010 when the temporary homebuyer tax credit boosted it back a bit above 40 percent. As interest rates began to climb at the beginning of 2013 refinancing eased and the first-time buyer share rose back to 42 percent.

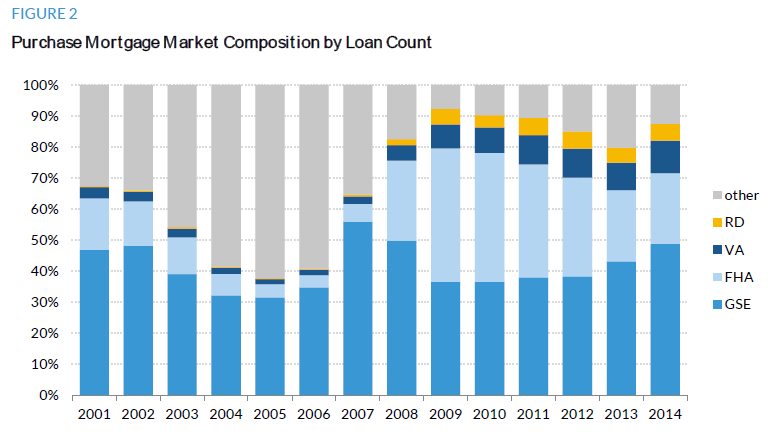

FHA is designed to provide mortgage access to households not adequately served by the conventional market including first-time buyers. As a result its share of homebuyers has always fluctuated around 80 percent of its purchase-loan originations, peaking at 81 percent in 2014.

When the housing market began to collapse in 2007 and private mortgage money disappeared the GSEs and FHA stepped in to provide nearly all home mortgage financing and have accounted for between 67 and 79 percent of purchase mortgage loans between 2008 and 2014.

Because of FHA's traditional focus on first-time buyers, the joint FHA-GSE first time homebuyer time series tends to be driven by shifts in FHA's market composition and as its share of the purchase market skyrocketed from 6 percent in 2007 to over 40 percent in 2010 this was reflected in the joint first-time homebuyer share. Then from 2011 to 2014 FHA insurance premiums rose and more buyers shifted to conventional loans. FHA's market share shrank to 23 percent in 2014 and the joint first-time homebuyer share declined from 61 percent in 2010 to 54 percent in 2014.

As shown in Figure 1 there is a substantial difference between the shares of first-time homebuyers as estimated by NAR and those derived from the GSEs and FHA. The combined GSE/FHA share (bright blue line) and the NAR reported share (gold line) both hovered around 40 percent until 2006 then they diverge. (The temporary spike in 2009 and 2010 coincided with the tax credit program) By 2014 there was a significant difference with NAR estimating a first-time buyer share of 33 percent while the authors put it at 54 percent. The authors go to great lengths to explain the discrepancy.

First, they say that NAR looks at all recent buyers while they focused only on those who obtained GSE or FHA mortgages. Secondly there was a vast difference in sample size with the Nar survey surveying about 148,000 recent homebuyers and sellers in 2014 with a 6.1 percent response rate while the Urban Institute looked at over 1.8 million loans.

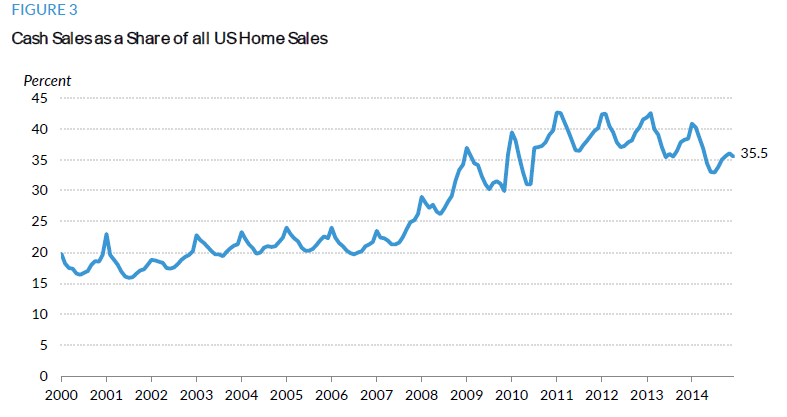

There was also a difference in the denominators. NAR's purchases differed from the study's in two important ways. The study's universe was mortgages originated to purchase homes intended for the owner to live in while NAR's included both owner-occupied homes and those purchased as investment properties or vacation loans and homes purchased without a mortgage. There was a nationwide surge in cash sales starting in 2007, rising to over 40 percent of all sales in 2011 and remaining at elevated levels. A surge in cash sales by investors would reduce the percentage of first-time homeowners in any survey that counts both cash sales and mortgage-financed purchases.

These denominator differences explain much of the discrepancy. For example, adding purchases for other than principal residences into the GSE/FHA share in 2014 would lower it from 54 to 49 percent. Assuming 30 percent of purchase transactions were cash would lower the share further to 34 percent, very close to the NAR's figure.

The study also describes a technical issue with Ginnie Mae's reporting which may be underrepresenting first-time buyers and urge that FHA begin making their data publicly available.

The authors looked at differences between first time and repeat borrowers in 2014 in the amount they borrowed, their credit scores, loan to value (LTV) and debt-to-income (DTI) ratios and the mortgage interest rates they obtained. Not surprisingly loan amounts taken through the GSEs were larger overall than FHA loans and also not surprisingly first-time borrowers took out smaller loans than repeat borrowers. However the gap between loan amounts for first time and repeat buyers was only about $26,000 for both GSE and FHA loans.

The average credit score of first-time homebuyers lagged 14 points behind the score of repeat homebuyers for GSE purchase loans, compared with only a 2 point difference for FHA loans. For GSE borrowers, the average LTV for first-time buyers stood at 85 percent; the average repeat buyer was able to pay slightly more than 20 percent up front to avoid mortgage insurance. Because of its low down payment requirement, FHA's LTV averaged about 95 percent for both types of buyers. Repeat buyers however had a slightly higher debt-to-income ratio than first-time buyers, reflecting in part higher homeowner-related obligations.

With higher credit scores and lower LTVs, the GSE repeat homebuyers enjoyed more favorable interest rates, 12 basis points lower than their first-time buyer counterparts. By contrast, the rates were about the same for FHA borrowers, as both types of buyers shared similar credit scores and LTVs.