Are low-down payment buyers beginning to benefit from a price war? The Urban Institute says that the Federal Housing Market has had an edge with homebuyers who lack the 20 percent down payment required for Fannie Mae and Freddie Mac (GSE) loans, but private mortgage insurers are ramping up the competition.

FHA and companies providing private mortgage insurance (PMI) provide guarantees to lenders that they will recoup at least some of their losses should loans where borrowers have put as little as 3.5 percent down default and require foreclosure. While it is the lender who is insured, it is the home buyer who pays the premium.

FHA guarantees require the borrower to pay both an upfront charge and an annual premium (billed monthly) and after FHA was burned by rampant foreclosures during the housing crisis both premiums were raised several times to help rebuilt its Mortgage Insurance Fund. With the fund returning to health, at the beginning of 2015 the Obama administration lowered the annual premium on FHA loans by one-half percent to 0.85% of the base loan amount or $212 on a $250,000 loan. FHA premiums do not vary by credit scores while PMI varies. After the FHA rate reduction a borrower with a credit score in the lowest FICO bucket (620-639) had a PMI premium that was over $200 a month more for that $250,000 loan than an identical FHA borrower.

The Urban Institute's Bing Bai and Laurie Goodman, writing in the organization's blog Urban Wire said the rate cut made FHA a better deal for almost all borrowers, even those with perfect credit would have paid almost $100 more per month with private mortgage insurance than through an FHA loan.

The lowered FHA premiums drove more borrowers to FHA loans and PMI insurers lost market share, from 40 percent of the market in 2014 to 35 percent in 2015 while FHA's share went from 34 to 40 percent. This reversed the trend of the previous four years as PMI insurers had steadily increased their share as FHA premiums rose.

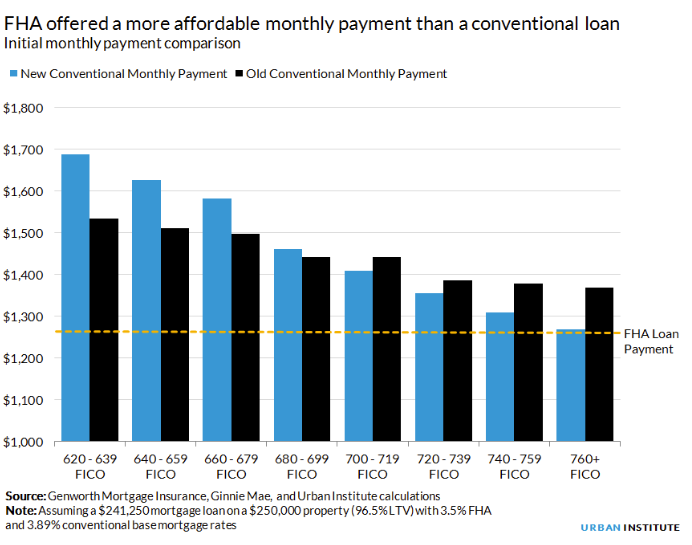

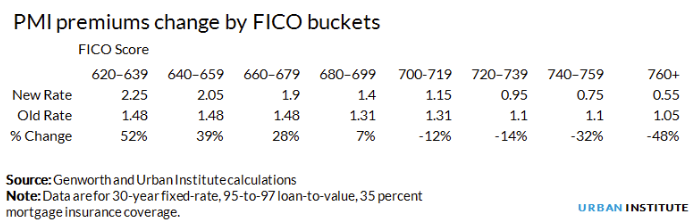

But now Bai and Goodman say, that may change. In April the PMI companies changed their fees making their insurance more affordable, at least for high quality borrowers. It lowers premiums for borrowers with FICO scores of above 700 and raises rates for those with lower scores. For borrowers with the highest credit scores (760 and above), the conventional loan payment fell sharply to $1,268, $5 less than an FHA loan. For borrowers with scores from 740 to 759, the conventional loan remains more expensive than the FHA loan, but the gap has shrunk substantially from $106 to $30. Moreover, borrowers stop paying private mortgage insurance once the remaining balance on the mortgage is down to 78 percent of the home's value, but FHA's annual premium never goes away, providing another reason for potential borrowers to favor conventional loans, even with a slightly higher monthly payment.

This new pricing could pull some of the highest quality borrowers out of FHA and into GSE loans. In fact, the new pricing buckets appear designed to promote adverse selection, that is to drive low-quality buyers directly to FHA.

The authors say the new pricing will likely increase the GSE share of low-down payment, high credit borrowers. "The overwhelming majority of FHA borrowers make down payments between 3.5 and 5 percent. Of these, 32 percent have FICO scores above 700-the range where the PMI premium is decreasing. Nearly 12 percent have FICO scores above 740 and may now find GSE execution to be more attractive. While the number of borrowers who will now choose the GSE mortgage over the FHA mortgage remains to be seen, we would expect it to be small but noticeable."