Here we go again?

Sam Khater, CoreLogic's deputy chief economist, says loan performance is beginning to show some cracks in what has been a near perfect veneer. This might be an early signal of a downturn in the credit cycle. Khater is not issuing a warning, merely alerting those who should be watching such things to pay attention.

He writes, in an article in the CoreLogic Insights blog, that a typical economic expansion and recession are strongly driven by loan performance. When times are good, lenders take on more marginal borrowers then tend to become more conservative when loan performance begins to deteriorate. That often exacerbates an economic downturn.

Loan performance across the four major types of loans (agricultural, business, personal consumption, and real estate) all improved throughout the first five years of the expansion. Then, over the last year, performance of the first three loan types began to slip. Real estate loans bucked the trend, continuing to improve. Now, Khater says, there are small signs that their pristine levels of performance could be deteriorating.

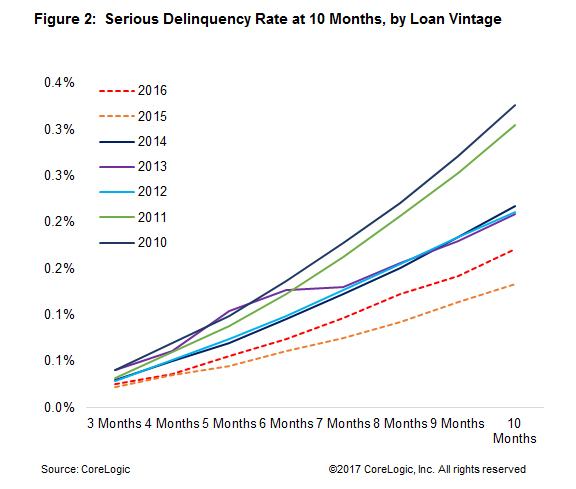

Mortgage performance is typical measured by levels of delinquency and foreclosure but those, Khater says, are both backward looking and lag as indicators. One way to address that is through transition rate analysis. This method controls for time by looking, in the case of his analysis, at loan vintage, i.e. production within a given year, which he says, allows for a much more nuanced view of performance.

By focusing on only those loans produced in the first 10 months of each year in question allowed Khater to include 2016 data in his analysis. His justification for the short and early time frame is that historically the first six to nine months of a loan's performance have a very strong persistence, and loans tend to remain on a similar track years later. He starts his analysis with 2010 as the first full year of the expansion vintages and says underwriting has remained roughly similar since then.

He sees three trends emerging from his analysis of these six vintages. The loans originated in 2016 were the first where the serious delinquency rate after 10 months was higher than in the previous year. Second, there is clear clustering in those years when the economy was weaker compared with the other economies. The first two years, when the economy was still recoverying and falling home prices had not yet turned the corner, loans had a 0.32 serious delinqeucy rate compared to 2012 through 2014 where the rate averaged 0.21 percent. Then in 2015, with the economy recovering, job creation picking up and home prices flying, the loans originated that year had the lowest serious deliquency rate in two decades, 0.13 percent.

Last year economic growth slowed a full percentage point and Khater says, "affordability cracks began to show. The serious delinquency rate for the 2016 vintage worsened, rising to 0.17 percent at the 10-month mark. Granted, this is a modest increase, and performance is still very good when compared to that over the last 20 years, still that is a show of some weakness."

Khater concludes, "Historically, when the mortgage credit cycle begins to deteriorate it continues to do so until the economy bottoms and the credit cycle begins to improve again. While the deterioration in mortgage performance is very small and rising from very low levels, it is important to track because turning points are critical but difficult to identify in real time."