Conventional wisdom, according to the Urban Institute (UI), holds that small mortgages are riskier than large ones. That may be one reason that only one out of four homes sold for $70,000 or less in 2015 was financed with a mortgage compared to 80 percent of those sold for $70,000 to $150,000.

Sarah Strochak and Alanna McCargo, writing in UI's Urban Wire blog say there are more than 600,000 homes for sale nationwide priced under $70,000, but it is hard for buyers to arrange financing because of the perception that the buyers of these homes have worse credit profiles and their loans don't perform as well.

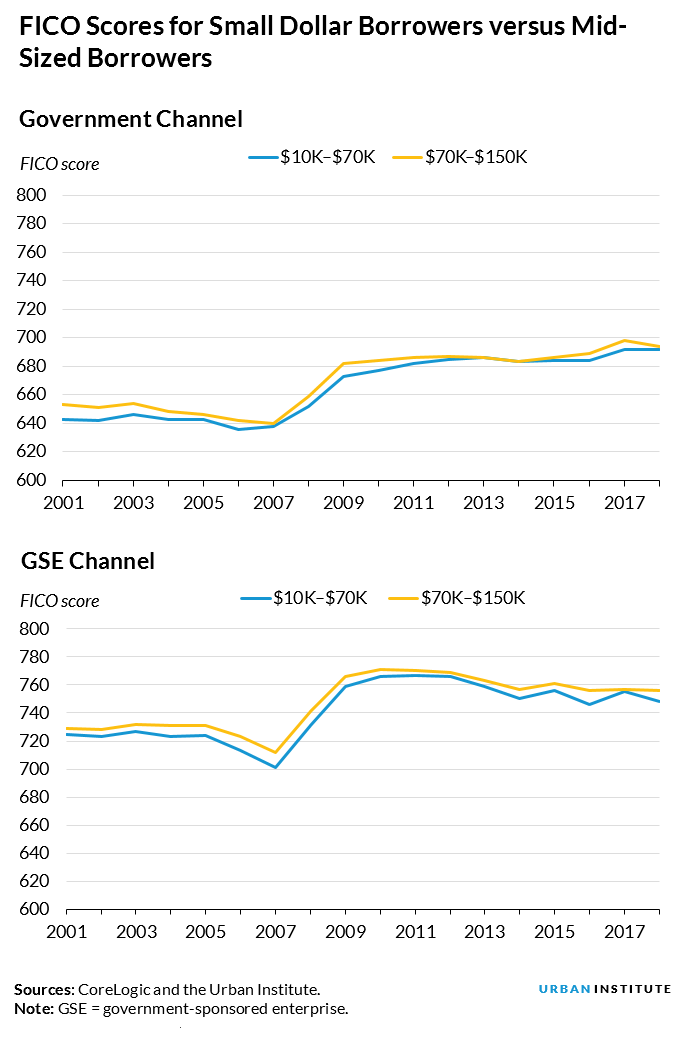

The two analysts have completed research which they say debunk this myth. Looking first at credit profiles, they found that those buyers who have been able to obtain small dollar mortgages across the spectrum, from government programs, bank portfolio loans, private label security (PLS) loans and the GSEs Fannie Mae and Freddie Mac, have comparable credit profiles to those of borrowers of mid-sized mortgages and their loans perform similarly. Over the past 17 years, the borrowers of small conventional and government backed loans have consistently had FICO scores within 10 points of their mid-size borrowing counterparts.

The loan-to-value (LTV) ratios are comparable as well, and debt-to-income (DTI) ratios are actually about 3 to 4 percentage points lower for small-dollar mortgage borrowers across all channels, likely because their smaller mortgages require lower monthly payments.

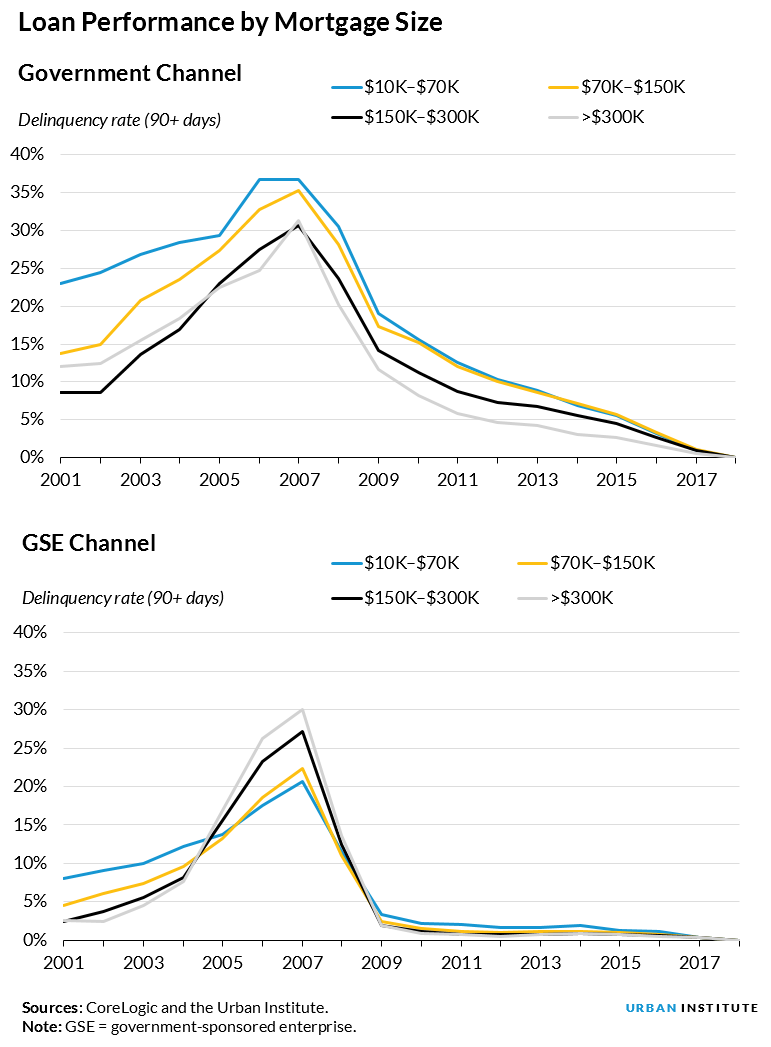

The small loans also perform similarly to those with higher balances over time. What little difference there is can be explained by the small differences in their LTV and DTI ratios and their FICO scores. Before the recession, smaller-dollar loans had noticeably higher default rates than other loans, but those borrowers also had lower credit scores. When the gap narrowed after the housing crisis, so did the difference in performance.

Even pre-crisis when GSE and portfolio loans consistently went to small loan borrowers with lower FICO scores their loans performed from nearly as well to even better than their higher balance counterparts. For example, the 2006 vintage of loans had a default rate of 17.5 percent for small loans and 18.6 percent for those with balances between $70,000 and $150,000.

The authors conclude that debunking the myth of risky small-dollar mortgages may lead to improving the availability of products targeted to that market. This would help low-and moderate-income households obtain the mortgages that would help them become homeowners.