It appears that lenders have surmounted the initial difficulties they encountered with the roll-out of the new Truth-in-Lending disclosures (TRID) required by the Consumer Financial Protection Bureau (CFPB) starting in October 2015. The new rule initially led to delays in home sale closings as lenders and their software vendors became familiar with the system.

Ellie Mae, in its latest Origination Insight Report, said that in March the time to close all mortgage loans dropped to the shortest period in since last March, 44 days. As the TRID rule was implemented the average time to close rose from 46 days in October to 48 in November and December as the TRID affected loans reached the closing table and to 50 days in January. That reversed dropping to 46 days in February and now the new low in March.

The average time to close a purchase loan dropped from 48 days in February to 45 days in March and the refinance timeline shortened to 41 days from 44 days. The time to close FHA loans decreased from 47 days in February to 44 days in March and the VA timing decreased from 50 days to 48 days.

The share of purchase loans increased slightly to 55 percent compared to 52 percent at the beginning of the year. Refinances as a percentage of lenders' overall loan volume fell one percentage point from February to 45 percent. The share of loans across loan types tends to move only a point or two each month. In March 66 percent of closed loans were Conventional, 22 percent were FHA, and 9 percent VA.

Average closing rates for all loans continued to rise to the highest since Ellie Mae began tracking data in August 2011. Increasing to 70.6 percent in March, from 69.9 percent in February. Refinance closing rates rose to 66.2 percent, while purchase closing rates were at just over 75 percent. The closing rate is calculated on a 90-day cycle rather than on a monthly basis because most loan applications typically take one-and-a-half to two months from application to closing. Loans that do not close could still be active applications or applications withdrawn by consumers or denied for incompleteness or non-qualification.

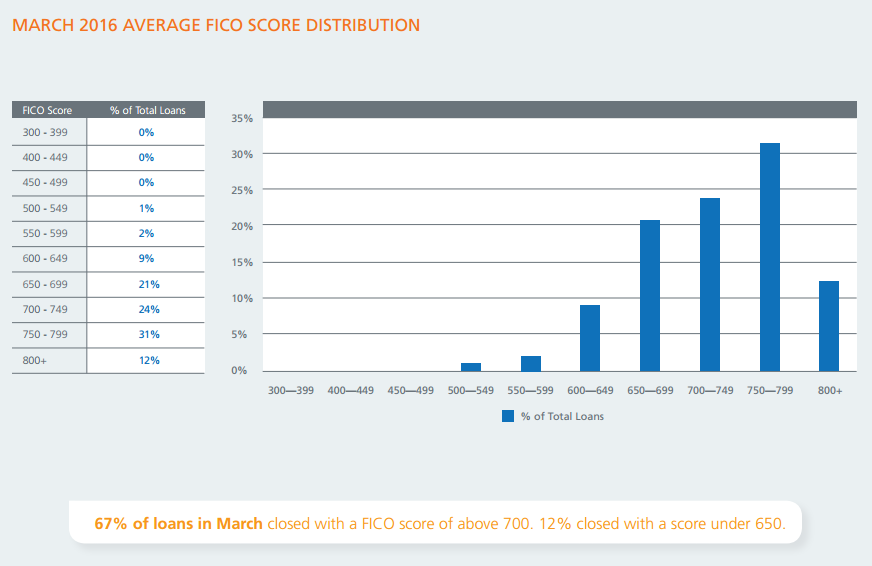

Sixty-seven percent of closed loan had FICO scores above 700 with an average of 722; only 12 percent of scores were below 650. The average loan-to-value ratio was 80 percent, up a point from February, and the average debt-to-income ratio, which has remained nearly constant for months, was 25/38.

"We continue to see a decrease in days to close from 46 days in February to 44 days in March," said Jonathan Corr, president and CEO of Ellie Mae. "In addition, the percentage of loans closing are continuing their upswing, increasing one percentage point to just over 70 percent, which is the highest closing rate we've seen since we began tracking data in August of 2011. However, we're still seeing credit remain relatively tight with 67 percent of closed loans having FICO scores of 700 or above."

Ellie Mae's Origination Insight Report mines its application data from a sampling of approximately 75 percent of all mortgage applications that were initiated on its origination software.