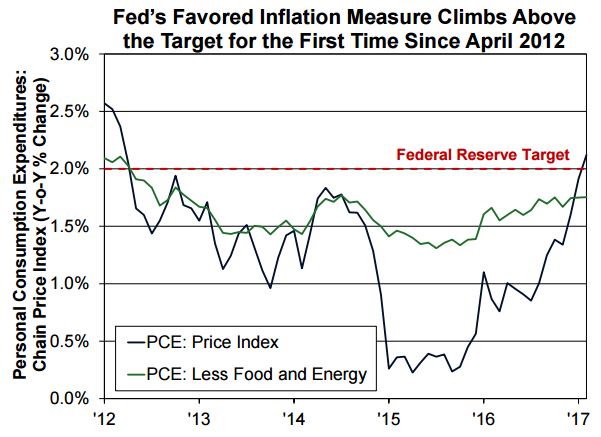

Fannie Mae has moved its projected timeline for further Federal Reserve price hikes forward by several months. The company's Economic & Strategic Research (ESR) Group points to an increase in the Fed's favored measure of inflation, the personal consumption expenditures (PCE) deflator, which increased by 0.1 percent in February, bringing it 2.1 percent higher than a year ago. This was the first time in nearly five years the PCE had exceeded the Fed's 2.0 percent target.

Combined with the unemployment rate which was down 0.2 percent to 4.5 percent in March, the ESR says "firming inflation will prod the Fed to raise the fed funds rate in June and September, compared with September and December in the prior (ESR) forecast." The minutes of the March Federal Open Market Committee (FOMC) meeting also point to an upcoming change in the committee's reinvestment policy, one that would begin shrinking the Fed's balance sheet and its huge portfolio of Treasury and mortgage-backed securities.

The ESR's April issue of Economic Developments notes that that reports from the housing sector during the first two months of the year were more upbeat than from other parts of the economy, partly because of unseasonably warm weather. Single-family starts were up and the National Association of Home Builders' index of builder confidence jumped by 6 points in March, the largest increase since the housing crisis. Multi-family starts and overall residential permitting however were both down.

Forward-looking indicators of home sales - pending sales and purchase mortgage applications - are both up, but the potentially faster pace of Fed rate increases, as noted above, pose a downside risk to home sales. Extremely low for-sale inventory is also expected to private a headwind to the spring home selling season. Declines in household mobility are suppressing the supply.

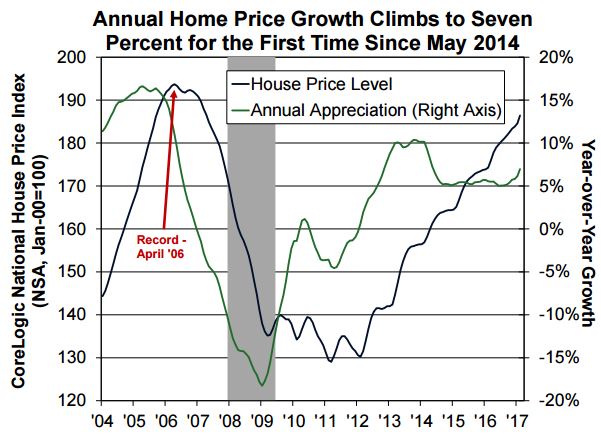

Fannie Mae's Home Purchase Sentiment Index gave back some of the previous months' gains in March as consumers overwhelmingly expect rates to rise and fewer feel that this is a good time to either buy or sell a home. Contributing to this a continuing high rate of annual price appreciation, 7.0 percent according to the CoreLogic Home Price Index, although slightly less per other indices.

Fannie Mae sees a slight uptick in inventories, perhaps as some sellers chose to lock in profits from recent price increases, and this, along with buyers jumping into the market before rates rise further, should push home sales up by 3.0 percent this year. The company is still forecasting that 30-year fixed rate mortgages should have an average rate of 4.3 percent by year's end and that mortgage originations will decline by about 20 percent this year to $1.58 trillion. The refinance share will drop by 50 percent from 32 percent last year to 16 percent in 2017.

In non-housing areas, Fannie Mae sees economic growth remaining at 2.0 percent in 2017, "unconvinced that a meaningful positive impact from stimulative fiscal policy will occur this year." First quarter growth appears not to have met expectations, but they expect improvement in the second quarter.

Near-term risks to the economy include a potential government shutdown on April 29 and policy uncertainty delaying investment decisions. The economic impact of a short shutdown would be minor because federal pay is usually made up retroactively, but a shutdown would weigh on consumer and business confidence.