As Americans are nearing the deadline to file their 2017 federal income tax return, what this will put on their 2018 return is still open to debate. The effects of the Tax Cuts and Jobs Act, passed by Congress in December was, in the words of CoreLogic's chief economist Frank Nothaft, "the largest change to the U.S. tax code in more than three decades," one that "has touched every person and industry." He recently looked at how it might affect tax-related housing decisions made by families.

The bill, he says, has lowered personal income taxes in the aggregate, but not necessarily for every taxpayer. An increase in after-tax income does increase, at least in general, the amount spent on shelter and thus the likelihood of being a homeowner - what economists call the 'income effect." This should, he says, all other conditions being constant, be a net plus for housing demand and homeownership.

But of course, not everything is constant - or perhaps equal would be a better word. Nothaft points to places where the bill will change things for a lot of tax filers. Persons with big mortgages, increasingly necessary for those buying on both costs, may lose some previous benefits from the mortgage interest rate deductions. The MID is capped for first mortgages over $750,000, and the deductibility for some home equity loans and second mortgages is gone. The deduction for property taxes might be affected with the new cap on the total of state and local taxes.

Even where deductions haven't been lost or reduced, many former itemizers may find it more beneficial to switch to the new and much higher standard deduction allowed in the new law. Lower marginal tax rates will reduce the value of itemizing for others.

"By raising the after-tax cost of homeownership, tax reform is expected, at the margin, to lower the amount of shelter consumed by owner-occupants and tilt tenure choice toward renting rather than owning," Nothaft says. Economists have a name for this as well, calling it the "price effect" because the relative cost of owning versus renting has changed.

Nothaft says whether it is the income effect or the price effect that prevails will determine whether the demand for shelter and the homeownership rate fall or remain about the same.

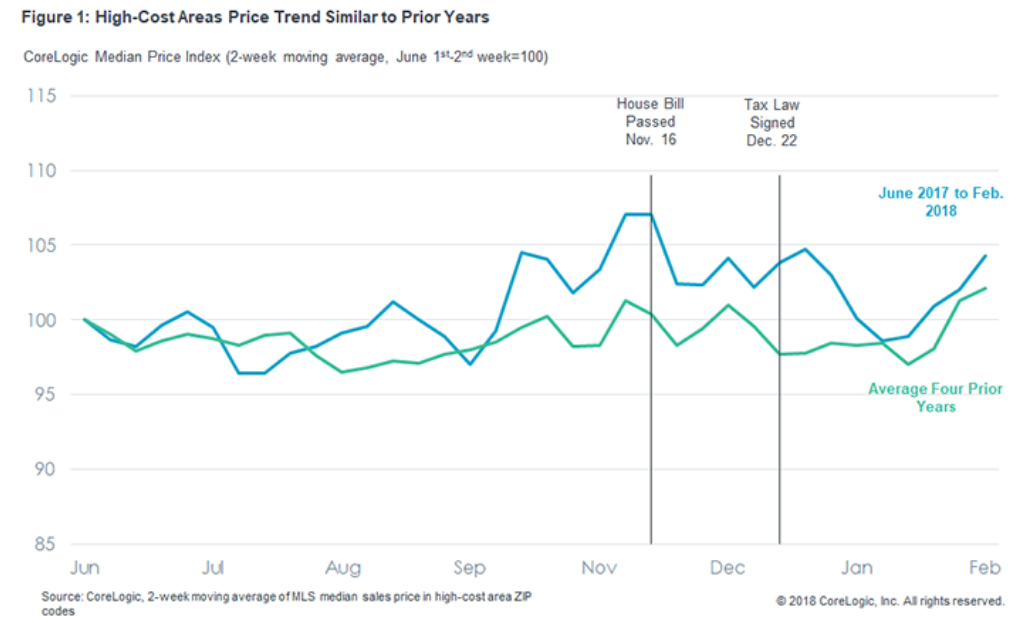

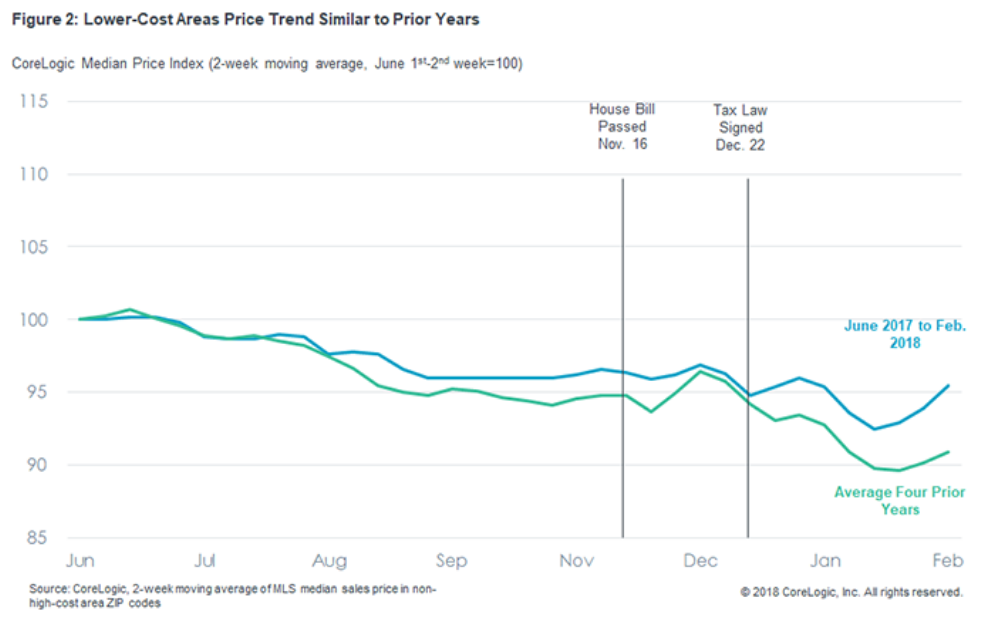

While it is still very early, he used CoreLogic sales data through February to analyze price trends in both high-cost areas, defined as places where the sum of annual mortgage interest and property taxes were the highest, and the remainder of the country outside these areas. Each was compared with the averages price trends of the previous four years. While the decline in unemployment, the strong stock market, and low inventories of available homes complicate the comparisons, he saw no material differences in price trends between to two areas, nor any meaningful change in the trends compared with earlier years.

In a footnote to his CoreLogic Insights article the economist notes that three other studies on the home price effects of the tax law contrast with his. All three, from PricewaterhouseCoopers, JPMorgan, and Moody's Analytics, expect a negative overall affect on home prices. The latter two expect negative price affects that are larger in higher priced areas or for higher priced homes and positive effects in lower-cost areas or for lower-priced homes. It should be noted that only the last study, by Mark Zandi, was completed after the bill was in near final form.