The American Banking Association (ABA) has found that real estate lending conditions at the end of 2011 were little changed from those at the end of 2010 despite increasing regulations, compliance costs and a lack of clarity about rules. ABA reported the results of its 19th annual Real Estate Lending Survey on Tuesday.

The survey involved 185 banks, 86 percent of which were smaller community banks with assets under $1 billion. Fifty-six percent of the participants were commercial banks and 68 percent were stockholder-owned.

The banks reported that refinancing made up 63 percent of mortgage activity in 2011 compared to 66 percent in 2010 but about the same percentage as in 2009. Fixed rate loans represented 80 percent or originations compared to 81 percent the year before and 30-year loans made up 47 percent of all originations, down 1 percentage point from the year before.

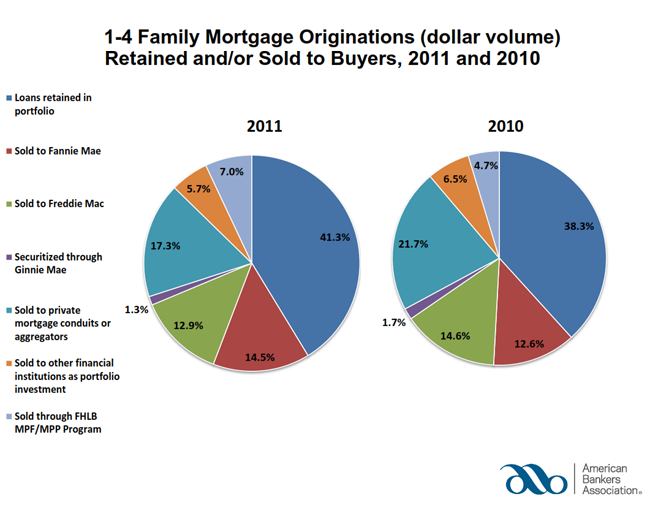

Banks retained 41 percent of the one-to-four family mortgages they originated during the year, an increase of 3 percentage points, and sold 27 percent directly to one of the government sponsored enterprises (GSEs), unchanged from 2010 but triple the volume in 2006. Sales to aggregators fell from 21.7 percent in 2010 to 17.3 percent in 2011, while sales to the Federal Home Loan Bank programs increased from 4.7 percent to 7.0 percent.

Conforming loans made up 72.0 percent of production, down from 72.0 while non-conforming loans increased from 11.6 to 14.0 percent. FHA loans were down from 6.5 percent to 5.0 percent and Jumbo originations increased slightly to 9.0 percent from 8.7 percent. Mortgage features such as piggy-backs, low documentation loans and pre-payment penalties have virtually disappeared in recent years. The only loan feature surveyed that had a greater than 5 percent reported occurrence was balloon payments.

Mortgages to first-time homebuyers represented 9 percent of originations, virtually unchanged over the last two years. The percentage of loans written with loan-to-value ratios of 60-80 percent rose slightly from 48 percent in 2010 to 51 percent with the difference made up by very slight decreases in several higher LTV categories.

Two-third of the banks surveyed used some type of automatic loan underwriting system with Desktop underwriter being the most popular type. A majority, 55 percent, reported that they do not scan or image loan documents for transmittal but 61 percent said imaging was a priority for 2012.

Respondents said that their major concerns regarding the mortgage market in 2012 were:

- Regulatory burden and compliance costs

- Falling home prices and drops in appraisal values

- Continued high unemployment, slowdown in economy, increase in foreclosures

- The future of the government sponsored enterprises

- Loan demand and other credit challenges.

"Continued concern about forthcoming mortgage rules and the unknown future of Fannie Mae and Freddie Mac have increased lending uncertainty in an already sluggish market," said ABA's Executive Vice President Bob Davis. "Clarity through well-constructed rules that ensure credit availability for qualified borrowers is essential for the housing recovery."