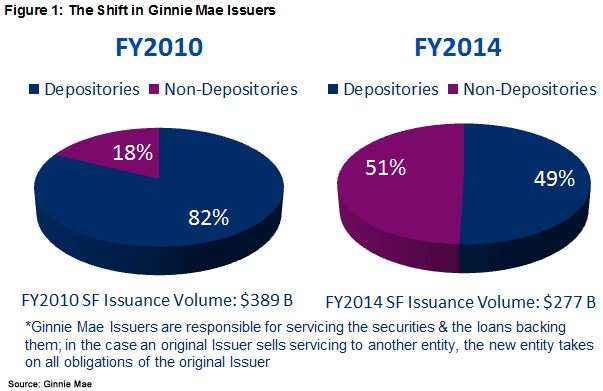

In the past five years there has been a monumental shift in mortgage loan servicing. Bank servicing subsidiaries, which once dominated in the market, no longer even constitute a majority of companies servicing Ginnie Mae mortgage loans. In an article in the CoreLogic Insights blog Faith Schwartz CoreLogic's senior vice president of Government Solutions, takes a look at how and why depository institutions have been releasing their servicing rights and what the implications may be for investors and consumers.

Schwartz says that seven years after the collapse of the housing market and after many many changes to regulations affecting mortgage originations, the face of those originations have changed and this is also having an effect on loan servicing. This trend of transferring servicing from banks to non-bank servicers, she says, can most likely to attributed to a combination of regulatory changes, reputational risks and basic economics.

Regulatory Changes:

Prior to implementation of BASEL II banks were able to contribute the value of mortgage servicing rights (MSR) to their Tier 1 capital but modified accounting treatment of MSR has led depositories to rethink their approach. This, Schwartz says, will continue to cap the growth of their servicing.

Other regulatory changes in Consumer Financial Protection Bureau (CFPB) servicing guidelines and Qualified Mortgage (QM) rules place new emphasis on default servicing, borrower engagement, and documentation management Penalties for violations have been, in Schwartz's words, swift and severe.

Reputational Risk:

While some aspects of servicing such as payment collection and processing had worked well in the pre-crisis years, increased delinquencies strained the collection and default services of services. The situation was made worse by a combination of light borrower contact, problems collecting information from borrowers, and the challenge of creating uniform processes inside institutions. These challenges coalesced around a problem that became more magnified than the industry anticipated. It provided ammunition to regulators and policymakers as well, pushing them to consider legislation specific to servicers. In addition, Schwartz says that reputation risk remains high when dealing with foreclosures and institutions with other revenue sources may turn away from high reputational risk activities.

The Economics:

Several factors have contributed to an escalation in servicing costs. Many states have enacted laws to slow down foreclosures and ensure procedural protections for consumers and the formation of the CFPB led to issuance of new rules as mentioned above. "The world (of servicing) changed from a traditional loss mitigation role to that of a borrower solution provider."

When you combine the activities that comprise "loan servicing" and overlay investor and government litigation, the overall cost to service loans has skyrocketed. Schwartz cites data from the Mortgage Bankers Association and the Urban Institute that estimate the cost of servicing performing loans has risen from $59 in 2008 to $156 in 2013 while costs for servicing non-performing loans has gone from $482 to $2,357.

Loan servicers say they are the most regulated entities around. A few metrics that are out there today to monitor performance include rating agencies, CFPB's complaint data base, Treasury HAMP ratings, Fannie Mae STAR rating system, Prudential regulators and State regulators.

Should we care if servicing is increasingly shifting to non-depository institutions? The author says it should make little difference to consumers. The rules are clear on how to engage with the consumer. There should be an ombudsman for difficulties and the CFPB consumer complaint database is an avenue for airing grievances.

For investors, there could be additional risk as these institutions have less capital than banks. But that can and is being managed, as agencies such as the Federal Housing Finance Agency and Ginnie Mae continue to issue guidance and rules around minimum capital requirements and adapt to these changing players in loan servicing.

Schwartz concludes that the sizable shifts in servicing that are taking place should not have a material impact on the industry as long as there is sufficient capacity for quality servicing as mechanisms are in place to manage and monitor activity on behalf of the investors as well as the consumer. One area of concern, however, is that the cost of default servicing will materially impact the cost of access to mortgage credit. "As housing finance continues to heal," she says, "there is an important role for investors and consumers to ensure there remains strong confidence in how the loan servicing market functions as it is a key component to a healthy and sound housing finance marketplace."