Annual reports from financial institutions rarely make the best seller list, but the one published by the Federal Reserve Bank of Dallas is beginning to rocket around the Internet because of an essay it contains. The essay, written by Harvey Rosenblum, Executive Vice President and Director of Research at the Bank is titled "Choosing the Road to Prosperity: Why We Must End Too Big to Fail - Now."

The essay is stunning enough in and by itself, but in an accompanying cover letter the Dallas Fed's President Richard Fisher expressly endorses it, in effect putting at least a part of the Federal Reserve System on record as advocating an end to Too Big to Fail (TBTF) institutions.

"In addition to remaining a lingering threat to financial stability," Fisher says, "these mega banks significantly hamper the Federal Reserve's ability to properly conduct monetary policy." Likening the economy to a car he said that the Fed had filed the tank with plenty of cheap, high-octane gasoline, but it takes more than gas to propel a car. "If there is sludge on the crankshaft - in the form of losses and bad loans on the balance sheets of the TBTF banks - then the bank-capital linkage that greases the engine of monetary policy does not function properly to drive the real economy. No amount of liquidity provided by the Federal Reserve can change this."

Propagating TBTF has also resulted in an erosion of faith in American capitalism, he said, and diverse groups "argue that government-assisted bailouts of reckless financial institutions are sociologically and politically offensive. From an economic perspective, these bailouts are certainly harmful to efficient workings of the market."

Rosenblum's essay tracks the downfall of the economy but less as a tick-tock than as a sociological study. It is long and difficult to summarize so we will do so in two parts.

* * *

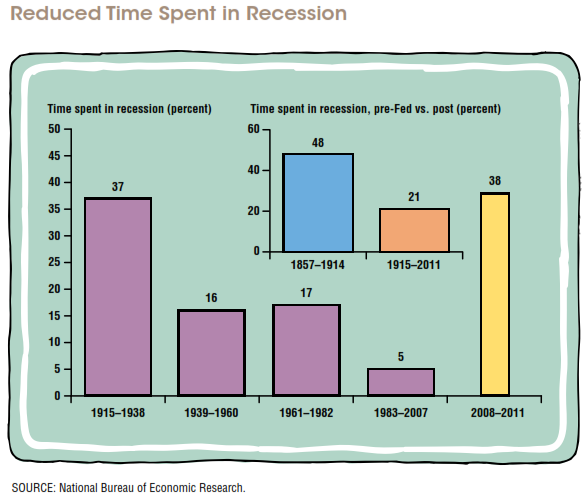

Good times breed complacency, not right away but over time, as memories of past setbacks fade. In 1983 the U.S. entered a 25 year span interrupted by only two brief shallow downturns accounting for just 5 percent of that period. There was strong growth, low unemployment and stable prices.

Before the Federal Reserve was founded in 1913 the economy spent 48 percent of the time in recession, in the 99 years since recessions have affected the economy only 21 percent of the time. "When calamities don't occur, it's human nature to stop worrying. The world seems less risky."

In the run-up to 2008 the public sector grew complacent and relaxed the financial systems constraints, explicitly in law and implicitly in enforcement, and felt secure enough to pursue social engineering goals such as expanding home ownership. The private sector also became complacent, downplaying the risks of borrowing and lending.

There was greed; capitalism cannot operate without self-interest and most of the time competition and laws keep it in check. But when competition declines incentives often turn perverse and self-interest can become malevolent. That's what happened in the years before the financial crisis. New technologies and business practices reduced "skin in the game," and greed led "innovative legal minds" to push boundaries of integrity.

Success led to complicity. The banks were making money, investors wanted part of it, and credit rating agencies got involved. The Fed kept interests rates too low too long, contributing to the speculative binge in housing and pushing investors to seek higher rewards in riskier markets. "Hindsight leaves us wondering what financial gurus and policymakers could have been thinking. But complicity presupposes a willful blindness. Why spoil the party when the economy is growing and more people are employed? Imagine the political storms and public ridicule that would sweep over anyone who tried."

"Easy money leads to a giddy self-delusion." The certainty of rising housing prices convinced some homebuyers that high-risk mortgages weren't that risky; that draining equity to pay for new cars or a vacation was prudent. Buying into the exuberance gave people what they wanted, at least for a while.

These traits, complacency, greed, complicity, and exuberance were intertwined with concentration, the result of a natural desire to grow bigger, more important, and a dominant force in one's industry. Concentration amplified the speed and breadth of the subsequent damage to the banking sector and the economy as a whole.

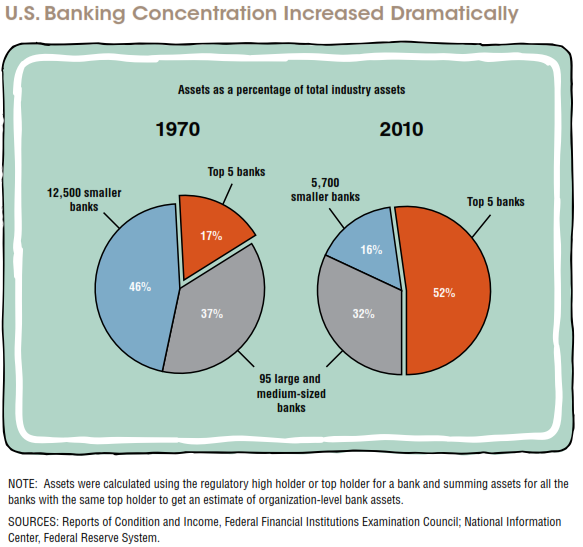

Since the early 1970s the share of the banking industry assets controlled by the five largest institutions has more than tripled from 17 percent to 52 percent. These mammoth institutions were built on leverage which was often hidden by off-balance sheet financing. The equity share of assets dwindled as banks borrowed to the hilt to chase easy profits in new, complex and risky instruments and balance sheets deteriorated. Accounting expedients allowed banks to claim they were healthy until they weren't. Write-downs were later revised by several orders of magnitude to acknowledge mounting problems.

With size came complexity as banks stretched their operations to include proprietary trading and hedge fund investments and spread their reach into dozens of countries. "Complexity magnifies the opportunities for obfuscation and top management may not have known everything that was going on, especially in regards to risk and regulators didn't have the resources to oversee the banks' vast operations.

These large, complex institutions aggressively pursued profits in overheated markets, pushed the limits of regulatory ambiguity and lax enforcement. They carried greater risk and overestimated their ability to manage it and in some cases top management groped around in the dark because their monitoring systems didn't keep pace with their expanding enterprises.

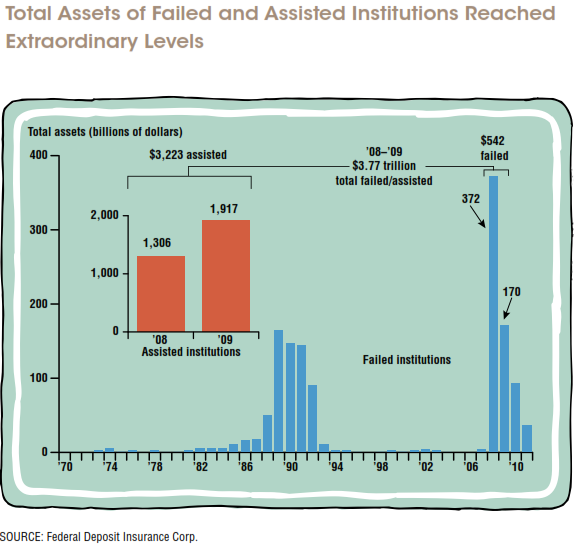

A healthy financial system keeps the economy humming and we take its routine workings for granted - until the machinery blows a gasket. It was the biggest investment and commercial banks that took the first write-offs on their mortgage backed securities in 2007 and as the housing market continued to deteriorate policy-makers became alarmed, seeing the number of big globally interconnected banks involved and fearing the loss of even one would bring the whole system down.

This fear was justified as Lehman Brothers collapsed and credit markets froze forcing the government to inject billions to keep other institutions afloat. "The situation in 2008 removed any doubt that several of the largest U.S. banks were too big to fail." Exhibit 3 (large image, opens in new window) tracks the benchmarks as the system began to fall apart.

Back then there were no lists of TBTF institutions; the term did not exist explicitly in law or policy, and the term itself "disguised the fact that commercial banks holding roughly one-third of the assets in the banking system did essentially fail, surviving only with extraordinary government assistance." Most did not fail in the strictest sense however bankruptcies, buyouts, and bailouts all constitute failure. More than 400 financial institutions did fail outright between 2008 and 2011.

With the financial system disabled, the entire system spun downward into the longest recession in the post-World War II era.

In the second part of the essay Rosenblum looks at the Fed's reaction to the recession, why TBTF has stymied recovery, and what might be done about it.

{kind=link}