Freddie Mac's economists headlined their March Outlook economic report "Adulting is Hard." The newest crop of young adults may find this to be truer than others. They have been slow to reach life's milestones like getting married, starting families and living independently, but with some valid reasons. Many came of age in the midst of recession; wage growth has been weak, and housing, education, and healthcare costs have risen rapidly. Average annual expenditures for adults aged 25 to 34 in 2016 are 36 percent higher than those faced by those the same age in 2000, while costs for health care and education have more than doubled.

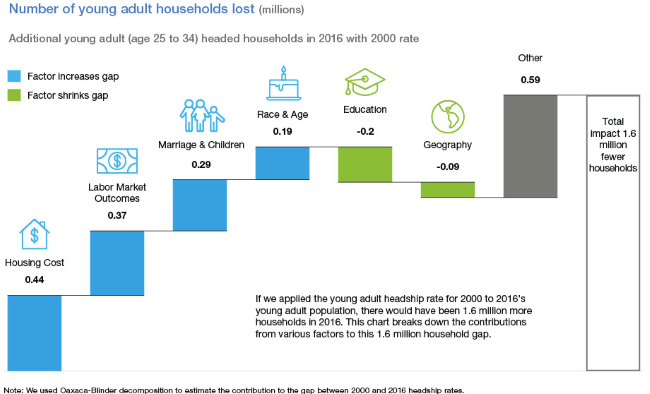

The U.S. Census Bureau says the 25-to-34-year age group contained 45 million people in 2016, 4 million more than the next older age group (35 to 44). But instead of fueling the housing market, they have been slow to form households. As of 2016, 15 percent of young adults were living with their parents, 5 percentage points more than did so in 2000. When they do strike out on their own, they often double up with a roommate. The rate of heading a household (headship rate) for young adults in 2016 was 3.6 percentage points below that of young adults in 2000. If these young adults had formed households at the rate of those in 2000, there would have been 1.6 million additional households in 2016.

The lower headship rate has had a major impact on the economy and housing markets, with implications for homeownership, residential investment and wealth building (chicken or egg?). Even relatively small percentage changes affect millions. The question is, will these young adults pick up the pace and make up for lost time in forming households.

The decision (or capacity?) to form a household depends on one's stage in life, such as age, marital status, and whether one has children. It also depends on the cost of living independently, such as choice of geography, housing costs, and an individual's ability to pay these costs-which is affected by education, income, employment and debt. The current crop of young adults is different from those in earlier generations in several ways. Freddie Mac picks five variables and compares Americans who were age 25 to 34 in 2000 and in 2016.

In 2000, 54 percent of young adults were married, and 52 percent were raising children compared to 41 and 42 percent in 2016. The marriage rates coincide with the increased number of young adults living with their parents.

More of the younger group live in central cities, 34 to 29 percent, where the cost of living is high. And they are facing higher home prices, a median of $270,000 compared to $210,000.

The younger group is far better educated, 44 percent have a bachelor's degree compared to 34 percent of their predecessors and they are carrying higher rates of student loan debt. They don't make all that much more money however; a per capita income of $38,500, up from $37,800. They are also slightly less likely, by 3 percentage points, to be in the workforce; 18 percent are not, although the authors say many of these may be employed by the gig economy.

In addition to these factors, young adults are more racially and ethnically diverse. Household formation rates tend to vary by race and ethnicity so a shift in the composition of the population could drive household formation rates.

Which of these factors have most impacted the headship rates for young adults? Freddie Mac constructed a model using person-level records from the U.S. Bureau of Labor Statistics' Current Population Survey. That model, while controlling for a variety of factors, predict the likelihood of a person heading their own household.

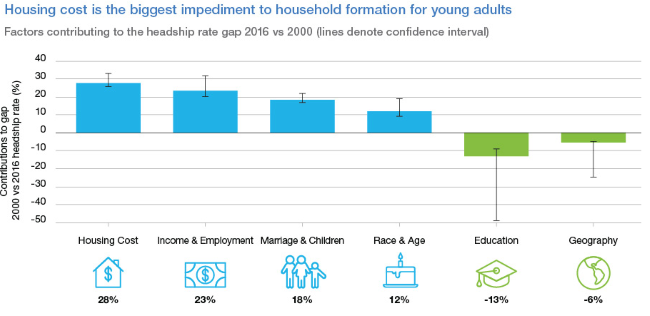

As expected, increases in housing costs decrease the likelihood of young adults forming households, accounting for 28 percent of the gap in that rate. Real median house prices increased by 29 percent, but per capita income rose by only 1 percent over the same period. This imbalance increased the ratio of home prices with income from 5.6 in 2000 to 7.0 in 2016.

A one percent increase in house prices decreases the likelihood of household formation by almost five percent. Higher incomes and higher education levels perhaps provide young adults confidence to form their own households and, all else being equal, a one-percent increase in personal income increases the likelihood of household formation by a little over three percent.

Another 23 percent of the gap is due to differences in labor market outcomes, including income and employment. Particularly important is labor market participation. Persons outside of the labor market and with zero or negative income are much less likely to form a household that those in the labor market, even with a modest income. Almost half of the gap between the generations is due to housing costs and labor market outcomes.

Differences in marriage and fertility rates account for 18 percent of the headship gap and demographics such as race, ethnicity, age, and gender account for 12 percent. Education and geography favor the younger generation, offsetting the gap by 13 percent. Overall, the variables that can be controlled in Freddie Mac's model explain about two-thirds of the decline in headship rates.

Sixty-three percent or 986,000 of the of the 1.6 million lost households are accounted for above. Exhibit 4 (below) demonstrates the bite taken by each of the variables. The remaining 590,000 households, or 37 percent are unexplained by Freddie Mac's model. They may be the result of debt, credit, underwriting standards, increased costs for medical care and education, even shifts in tastes. above.

The bottom line is what this all means for the future. How will these factors influence future housing demand? How will young adult household formation evolve by 2015; will it catch up with 2000 or continue to lag? How will those young adults show up in the 2025 housing market? Sheer numbers mean more households, but how many more.

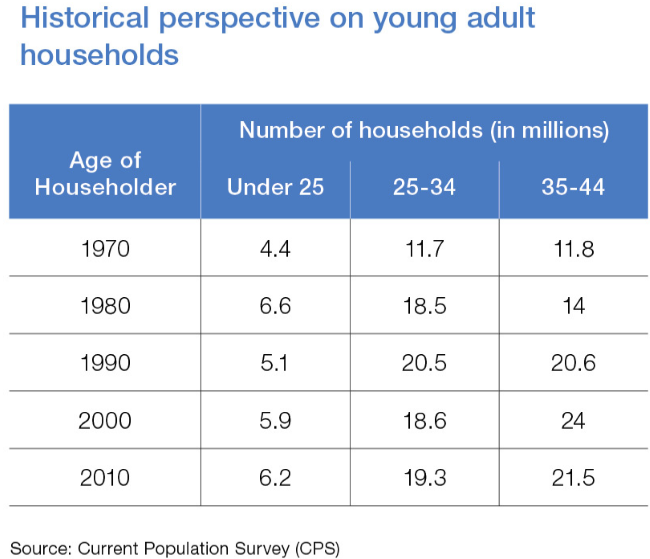

The historic numbers of households give some clue. In the 1970s, the 25-34-year cohort headed 11.7 million households and after 10 years, increased that to 14 million. The 1990 crop of 25-to 34-year-olds headed 20.5 million households, 24 million by 2000.

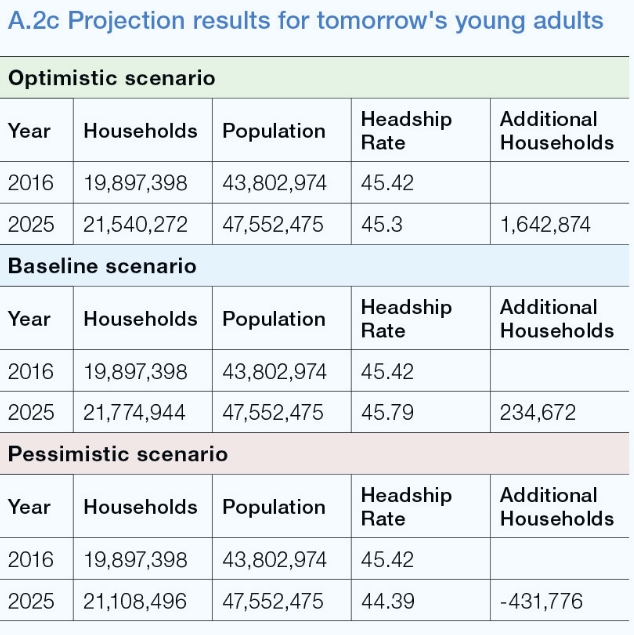

How might today's young adults contribute to household formation by 2025? Freddie Mac analyzes those two factors with the greatest impact to date, housing costs and labor market outcomes, assuming the current trends in economic, sociological, labor market and housing market factors persist over the next 10 years. The baseline scenario which reflects a relatively static economy provides a view on the effect of evolving demographics on household formation.

Their most optimistic take is that economic conditions will improve over that period, keeping housing costs fixed but matching the 1990s experience where real personal income increases 15 percent for all age and race/ethnicity groups. They also push labor force participation and unemployment rates to 2000 levels.

Their pessimistic outlook keeps labor market and income fixed but presents a deteriorating housing scenario. Housing supply persists in falling short of demand and real home prices increased an additional 10 percent. Overall young adults will confront a cost of living 20% higher than that of today's young adults.

Using the variable values and their influence on household formation on the projected population, Freddie Mac came up with an estimate of the number of households that might be formed. Those young adults aged 25 to 34 in 2016 could add between 4.2 and 4.5 million net new households while future young adults (ages 15-24 in 2016) could add between 15 and 16 million households.

Given the relationship between household formation and housing demand, it is important, Freddie Mac's economists say, to track the former to predict and prepare for the latter.

Housing costs are a major factor holding back young adults' household formations, and Freddie Mac's analysis indicated that 28 percent of the decline in household formation is due to those costs. That factor will suppress household formation by 600,000 over the next decade if those costs continue to rise. Alternatively, if costs stabilize and the labor market improves, there could be 300,000 more new households relative to the baseline.

Freddie Mac's analysis concludes, "There is substantial pent-up demand for household formation from today's young adults. That demand will tax a housing market that is struggling to produce enough supply to meet demand under current conditions. Rising housing costs along with the substantial pent-up demand will add pressure to housing markets and increase the urgency for solutions that provide affordable housing."