Fannie Mae's March economic forecast was written before the FOMC announced an increase in the fed funds rate last Wednesday. The company's economists assumed there would be an increase, but hedged some of their predictions by noting both upside and downside risks to their 2 percent growth forecast.

Currently the country appears on track to start the year with first quarter growth decelerating from the previous quarter for the fourth consecutive year. In February, Fannie Mae predicted the downturn would be minimal, with growth remaining around 1.9 percent annualized. New data indicates that forecast was too optimistic and they have revised their first quarter estimate to 1.6 percent. The main culprit was consumer spending, which fell 0.3 percent, the biggest drop in three years.

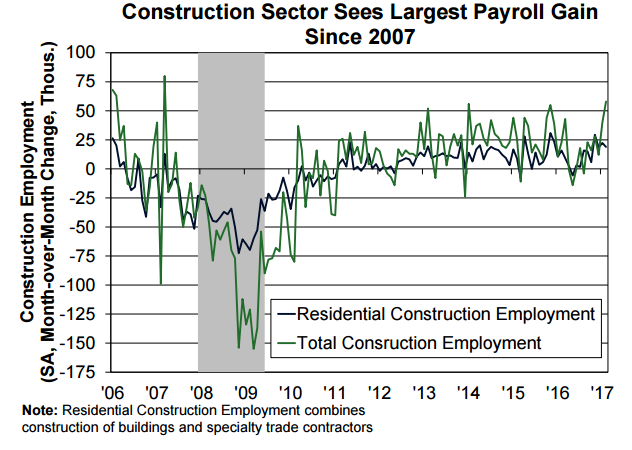

The strong February jobs report, 235,000 new jobs, was boosted by the largest monthly increase in total construction payrolls since 2007, at least in part due to unseasonably warm weather. Residential construction payrolls extended a string of at least 18,000 jobs added per month since last November.

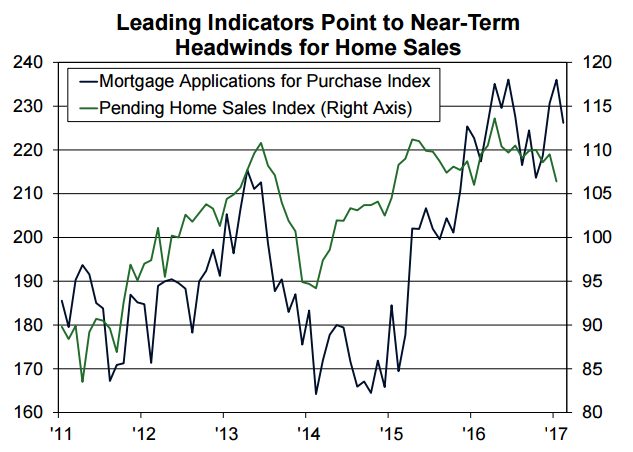

Home sales rebounded in January from their December downturns. Existing homes had a sizeable gain, growing to the strongest annual rate since 2007 and new home sales partially recouped the previous month's losses. However leading indicators were worrying. Pending sales declined for the second time in three months to a 12-month low and purchase mortgage applications dropped on overage in February after three previous consecutive monthly gains. Fannie's economists say "The weakness in these leading indicators supports our view that some of the improvement in home sales at the start of the year was likely the result of a rush to enter the market before mortgage rates could rise further."

On a positive note, Fannie Mae's Home Purchase Sentiment Index increased in February for the second month and was at its highest level since data collection began in 2010. Housing inventory remains very tight, especially for existing homes, which had the smallest inventory in January since tracking began in 1999. This scarcity has sustained upward pressure on home prices. At the end of 2016 the major home price indices recorded the strongest annual appreciation since 2013 and the early January releases indicate the trend is continuing.

Further, the inventories are leanest at the lowest tier of home prices, weighing against first-time homebuyers. Because listings are not keeping pace with demand for starter homes, prices for lower-tier homes are also appreciating at a much faster pace than prices for higher-end homes.

Homeowner net equity increased $0.5 trillion, in the fourth quarter, resulting in a cumulative increase of $7.1 trillion over the past five years. CoreLogic reported home equity as a percent of real estate value increased to 57.8 percent last quarter from a record low of 36.0 percent in the first quarter of 2009 and the share of residential properties with negative equity continued to trend down, reaching 6.2 percent from a peak of 26.0 percent seven years earlier.

While rising home prices are creating challenges for first-time homebuyers, the large Millennial generation is moving full-force into the age groups (late twenties through mid-30s) where first-time home buying is common and there are indications indicates that homeownership rate gains have accelerated recently among that generation.

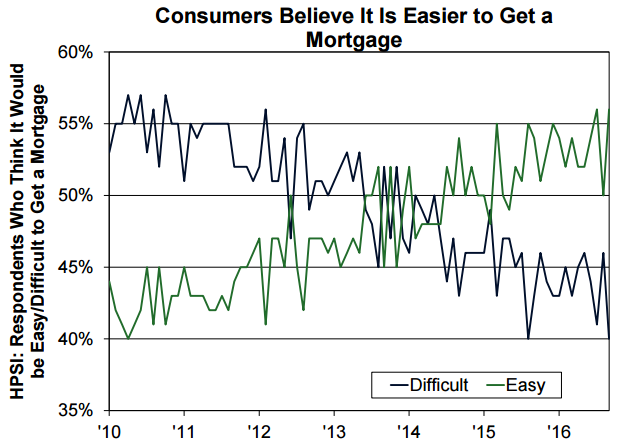

Another positive for the mortgage market is that February's National Housing Survey showed the share of consumers who believe that it is easier now to get a mortgage exceeded those who believe it is more difficult by the greatest margin in six years.

Tight inventories and home price gains are good news for homebuilding. In January, single-family starts rose modestly as multifamily activity fell sharply. Homebuilders remain upbeat; the builder confidence index rose 4 points in February and 6 in March.

Fannie Mae's outlook for mortgage rates, housing activity, and mortgage originations changed little changed from its prior forecast. Total mortgage originations are expected to drop about 19 percent this year to $1.57 trillion, and the refinance share should decline 15 percentage points from 2016 to 33 percent. Single-family mortgage debt outstanding continued to recover from its dive during the housing crisis, rising 2.7 percent annualized in the fourth quarter from the prior quarter and 2.3 percent from a year ago.