The Department of Housing and Urban Development released five reports from its Office of Inspector General on Tuesday based on reviews of the foreclosure and claims processes of the five largest Federal Housing Administration (FHA) mortgage servicers. OIG conducted the audit of Bank of America, Wells Fargo Bank, CitiMortgage, JPMorgan Chase, and Ally Financial, Inc, after allegations were made in the fall of 2010 that national mortgage servicers were engaged in questionable foreclosure practices involving foreclosure mills and robo-signing of sworn documents in thousands of foreclosures.

For each of the five servicers OIG conducted a review of a wide variety of documents such as personnel files, servicing and foreclosure processes, Congressional testimony and court documents regarding those processes, FHA claims documents, and foreclosure affidavits. They also interviewed servicer management and staff and those of vendors involved in foreclosures and claim processes.

The five separate reports generally reached the same conclusions. First, the servicers did not establish effective control over their foreclosure processes. The affiants (a person who signs an affidavit and attests to its truthfulness before a notary public) routinely certified that they had personal knowledge of the documents they signed without actually referring to source documents or verifying the accuracy of the foreclosure information. Affiants admitted to having signed large numbers of documents each day. One Ally employee, for example, claimed to have signed up to 400 documents a day and 10,000 per month. The affiants had neither the work histories nor training to hold the titles they held. Notaries did not always witness the actually signing of documents and routinely notarized hundreds of documents each day.

The servicers also did not follow HUD requirements for properties foreclosed on in judicial states and may have conveyed improper titles to HUD because it did not establish control environments which followed the requirements.

It was discovered that Citi did not have written processes in place for signing documents prior to November 2009 nor did it track documents during the period of the OIG review. OIG said its investigation of Citi was hampered by this lack of records and it had to rely on personnel interviews for much of its information.

OIG found that in many instances supervisors at each servicer were aware of the violations of procedures while they were happening. The Chase report for example states "During Interviews, Chase's operations supervisors acknowledged that they routinely signed and certified that they had personal knowledge of the contents of documents ... without reviewing the source documents referred to in the affidavits." Chase also outsourced its document execution process to First American.

A Bank of America employee said her direct supervisor, a vice president, was aware and approved of the industry standard (to have documents notarized outside the presence of the signer) being followed. She assumed her supervisor's boss would have approved and been aware of the same. A Bank of America manager said she read the first paragraph of a document, and then located the place she needed to sign. She spent 1-1/2 to 2 hours per day on signing documents and two to three minutes on each.

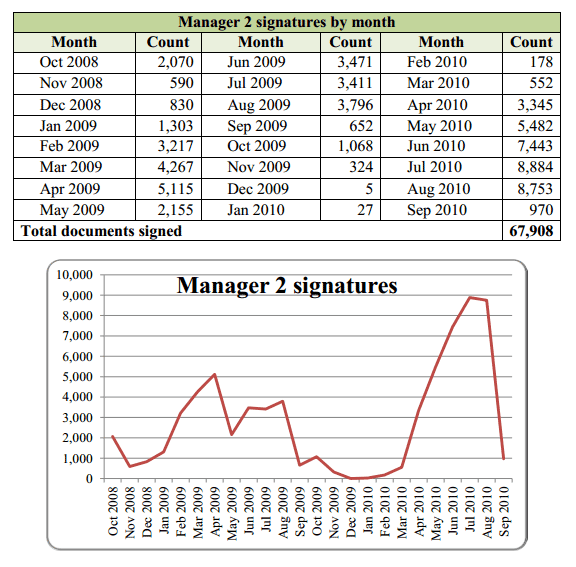

OIG provided the shipping log kept by one Bank of America manager showing that she had signed 67,908 documents (93 documents per day) and notarized 1,390 during a two year period. Records show she had notarized her own signature on two of the documents.

OIG also found that some affidavits it reviewed contained errors in the mathematics required in judicial foreclosure states. Bank of America was found to have calculated per diem charges inconsistently even within the same document and there were instances of incorrect legal descriptions of properties conveyed to HUD. Out of 36 affidavits for foreclosures that were reviewed for the Chase inquiry, the bank was unable to provide documentation for the amount of the borrowers' indebtedness listed on the affidavits for 32 and of the remaining four, OIG found the amounts to be inaccurate in three.

The findings of OIG in their reviews were used by the Department of Justice in reaching the recent $25 billion settlement with the servicers.

The five full audits can be found here.