In its most recent Mortgage Monitor, Black Knight Financial Services dug deeper into a topic it had raised in an earlier edition, the seasonality of mortgage delinquencies. In its February Monitor the company looked specifically at the role of federal income tax refunds in mortgage cures. The analysis noted that those taxpayers who file in the first two weeks of the tax season, that is by February 5, are those most likely to be expecting a refund. They also, on average, receive a larger refund than those who file later, by factors of 35 to 50 percent more than mid-season and near-deadline filers.

Given this data, Black Knight says it is no coincidence that, based on past performance, nearly 300,000 more delinquent borrowers can be expected to bring their mortgages current in February and March than in other months, likely using their tax refunds to do so. Further, this pattern is more pronounced in early delinquencies where past due balances and fees are still relatively low and are seen more frequently among FHA/VA borrowers "who might be expected to have less cash reserves on hand and therefore be more dependent upon the infusion of funds during tax refund season to pay down late payments."

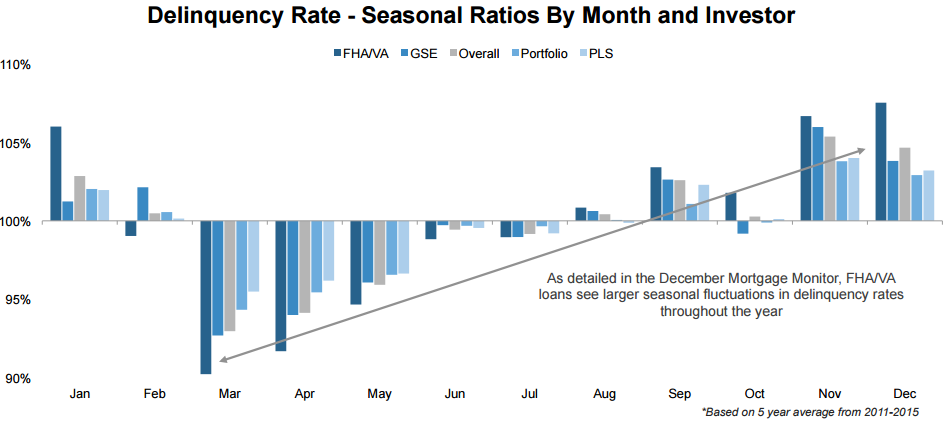

In the March the Monitor looks at the further impact geographic and loan characteristics may have on seasonal delinquencies and finds that, in addition to investor category, it varies by loan age, loan vintage, and geography. The company first looked at average seasonal ratios from 2011 to 2015, broken out by investor.

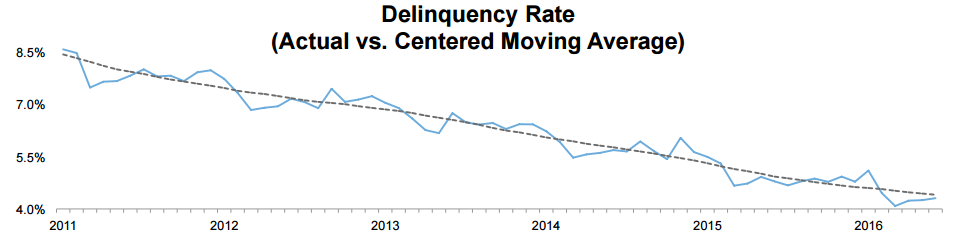

Consistent with the tax-return explanation March has the lowest delinquency rate, typically 7 percent below the rolling 12-month centered moving average. FHA delinquencies fall 10 percent below that moving average in the spring and have the most serious rise in delinquencies in the winter months, up 8 percent in January compared to 5 percent for all active mortgages.

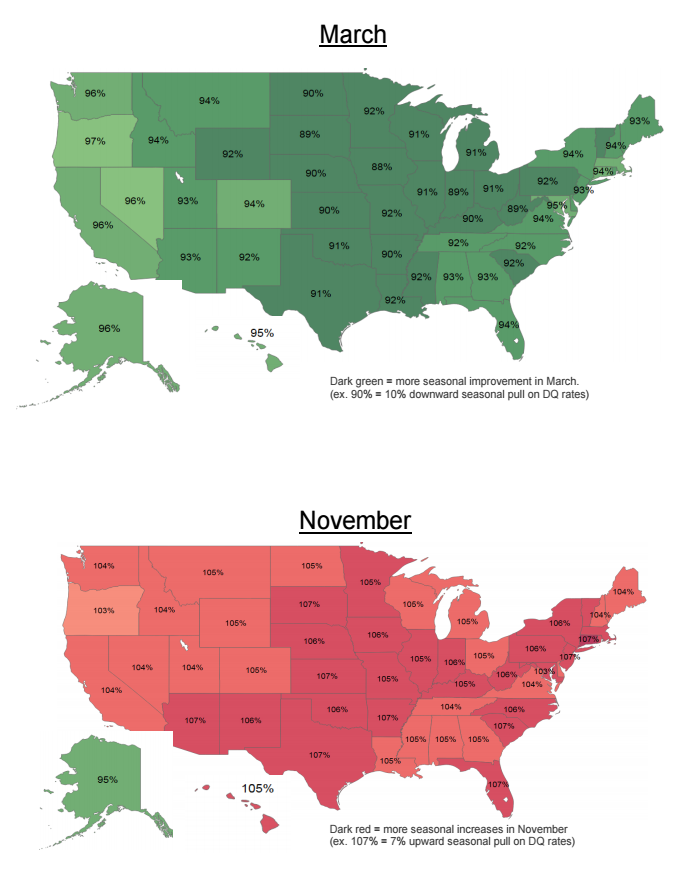

There is also a geographic component to seasonality. The two maps show the states and the seasonal pull on their delinquency rates. A number below 100 percent signifies a decline in delinquency rates from the centered moving average (i.e. 90 percent indicates a 10 percent downward pull) while a number above 100 percent indicates an increase. Black Knight notes that virtually all states follow the same pattern, lower delinquencies in the spring, higher in the fall and winter, but there is a much more profound impact in both seasons in the central U.S. while coastal areas, especially the West Coast, see much smaller seasonal swings.

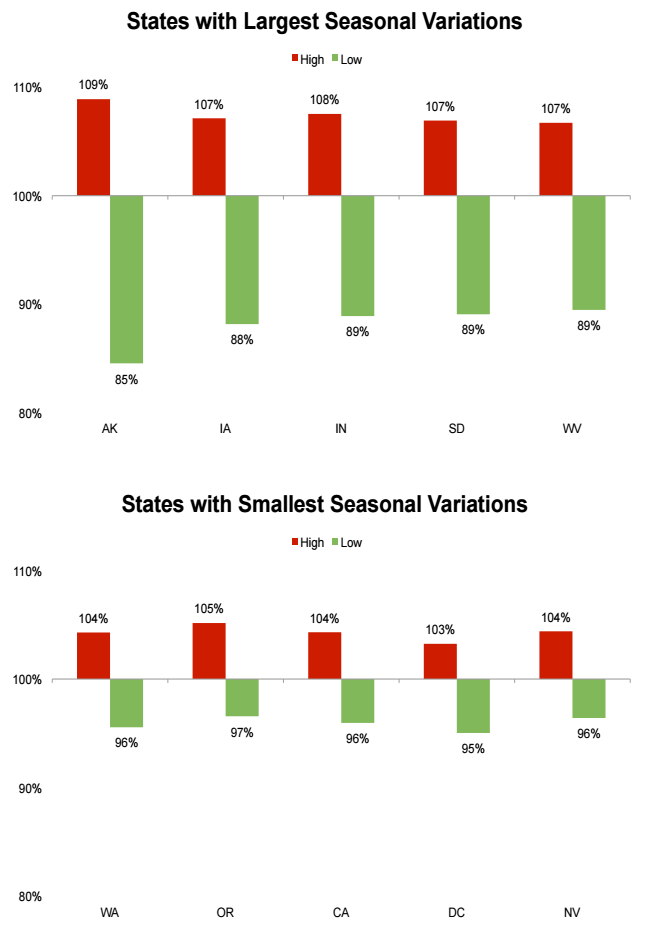

Black Knight posits several possible causes for the differing impact of geography on seasonality including home price and related down payment and reserve requirements and income variations, average loan age, and mortgage product mix. What they don't mention is weather. Four of the five states with the strongest seasonal variations are those that often suffer severe winter weather while four of the five with the smallest swings have notably temperate climates. Bad weather can increase household costs for energy and cause job layoffs in construction and other outdoor occupations. The data does make clear that in the states with the lowest seasonal variation it is less than half the impact as in those with the most.

Local market factors can also affect seasonality. Black Knight gets very granular in Alaska, the state with the greatest variability, showing the impact of the annual oil royalty payments received by permanent Alaska residents as well as the crab fishing season.

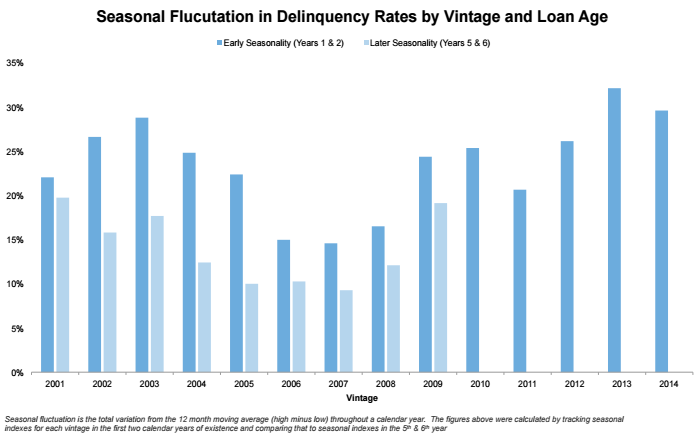

Two final factors that impact seasonal delinquencies are the age of the mortgage and the mortgage's vintage. On average, there is a seasonal fluctuation of roughly 23 percent around the 12-month moving average within the first two years of mortgage origination. However, that average of 23 percent blurs a range by vintage of 15 to 32 percent. Mortgages originated from 2006 to 2008 show very little seasonality compared to those originated before and after those dates, perhaps because delinquencies in those vintages are driven more by serious inabilities to make mortgage payments. This could be important Black Knight says, because it may suggest that early seasonality or its lack could potentially be a sign of eventual long-term performance.

Seasonality also declines with age, on average by 30 percent from the first two years to the fifth and sixty years of mortgage life. The same decline is true with 30-day delinquency rates, suggesting borrowers are less likely to become even moderately delinquent due to seasonal factors the longer they hold and perform on their mortgage.