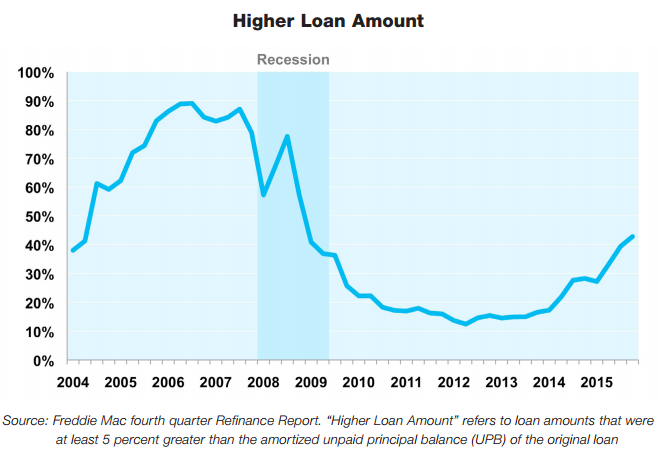

Even as the share of originations going for refinancing began to flag in the fourth quarter of 2015 the cash-out share of those refinancing increased. Freddie Mac said that transactions in which the new mortgage exceeded the old by 5 percent or more made up 43 percent of all refinances done during the quarter, up from 39 percent in the previous quarter and 28 percent a year earlier. It was the highest cash out share since 2008.

Freddie Mac funded $76 billion in mortgage loans during the fourth quarter, down from $94 billion in the third quarter. In both quarters refinancing represented about 50 percent of that volume, $38 billion in the fourth quarter and $46 billion in the third. In the first two quarters the refinance share was over 60 percent.

Prior to the housing crisis an average of 64 percent of refinances included a cash out component, peaking at 89 percent in 2006. After the crash the share plummeted, hitting 12 percent in the second quarter of 2012. It didn't climb above 20 percent for the next two years.

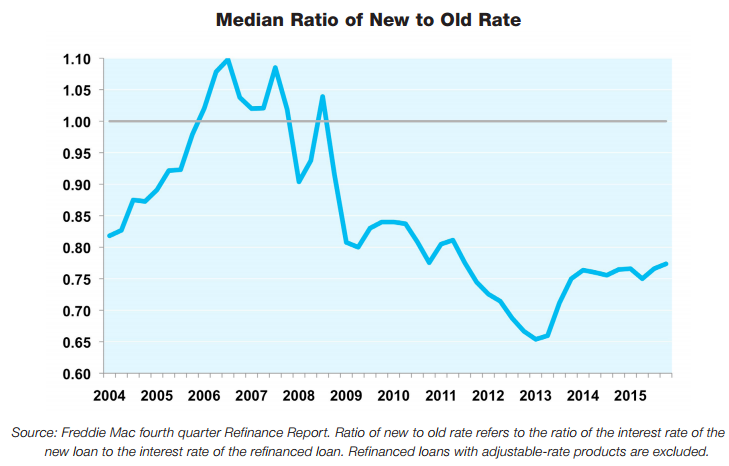

There is a definite cycle to cash-out refinancing. Simple math dictates that the percentage of refinances they represent increases during periods when rates are stable or ascending because the overall rate of refinancing declines. Consequently the ratio of new to old mortgage rates is also higher, in some periods exceeding 1:1, as withdrawing equity becomes a more important driver of refinancing than an improvement in rates.

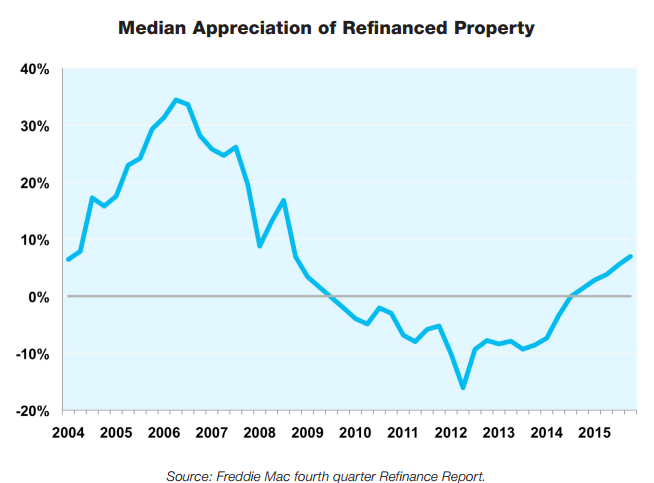

High cash out periods also correlate strongly with higher home appreciation rates between the existing and new mortgage and a shorter time span during which the old mortgage was in place. Over the years Freddie Mac has tracked the data the median age of the existing loan at refinance averaged 3.85 years. Since 2013 the median has exceeded 6 years and was 6.27 years in the most recent quarter.

Borrowers who refinanced during the fourth quarter cut their interest rate by 110 basis points on average, a 23 percent reduction. This is high by historical standards; the average rate reduction is 13 percent and during 2006 and 2007 when 83 to 87 percent of refinances had a cash-out component the average rate actually increased by 5 percent.

Prior to the fourth quarter of 2009 the median appreciation during the life of the existing loan was never negative, averaging 16 percent median growth. Then appreciation declined for 19 straight quarters, dropping into negative territory in 2010 and staying there until 2014. Appreciation has been positive for five consecutive quarters and climbed to 7 percent in the most recent quarter.

Borrowers who refinanced in the fourth quarter overwhelmingly, by 95 percent, chose fixed rate loans. Only 17 percent of those with hybrid adjustable rate mortgages refinanced into another hybrid.