In a new white paper titled Home Equity Lending Landscape, CoreLogic says that in the recent past homeowners who wanted to tap the equity in their homes might have looked to a cash-out refinance. The housing crash and the record low interest rates that followed have perhaps modified that behavior. "After years of being out of favor," the company says, "home equity lending is making a comeback."

For the past two year home equity loans (HEL) and home equity lines of credit (HELOC) originations have been growing as homeowners reclaimed equity in their homes and lenders regained confidence in the market. In the last three quarters of 2015 there were 976,000 new HELOCs put in place with combined limits of $115.8 billion; both numbers the highest for those quarters since 2008. The numbers were up 21 percent and the dollar volume increased 31 percent over the same period in 2014.

Home price appreciation has sharply reduced the negative equity that existed a few years ago, especially at the bottom of the market. According to the Federal Reserve homeowners have regained more than $6 trillion in equity since the first quarter of 2009. By the end of the third quarter of 2015 there were more than 15.6 million borrowers with loan-to-value (LTV) ratios below 50 percent, another 18.3 million with LTVs between 50 and 75 percent and 30 million more who own their homes free and clear. Thus there are increasing numbers of people who are able to borrow against their homes' value while job growth and increasing consumer confidence have increased the number who are willing to do so.

But back to CoreLogic's theory of behavior modification. As of October of last year the company says nearly three-quarters of homeowners with a mortgage carried an interest rate below 5 percent and the average rate on outstanding mortgages is 3.8 percent. Going forward, CoreLogic asks "how will these owners finance major expenses, college tuition, a new car, or large medical bills? What about debt consolidation? Will they be willing to give up their low first mortgages and refinance into higher rates or will they instead tap equity via HELs and HELOCs?"

And what about those owners or need larger homes or want more amenities? "Will they be as quick to sell and move up to a larger home (and a larger first mortgage at a higher rate) as they have in the past? Or will they consider remodeling instead, and use home equity products finance it?"

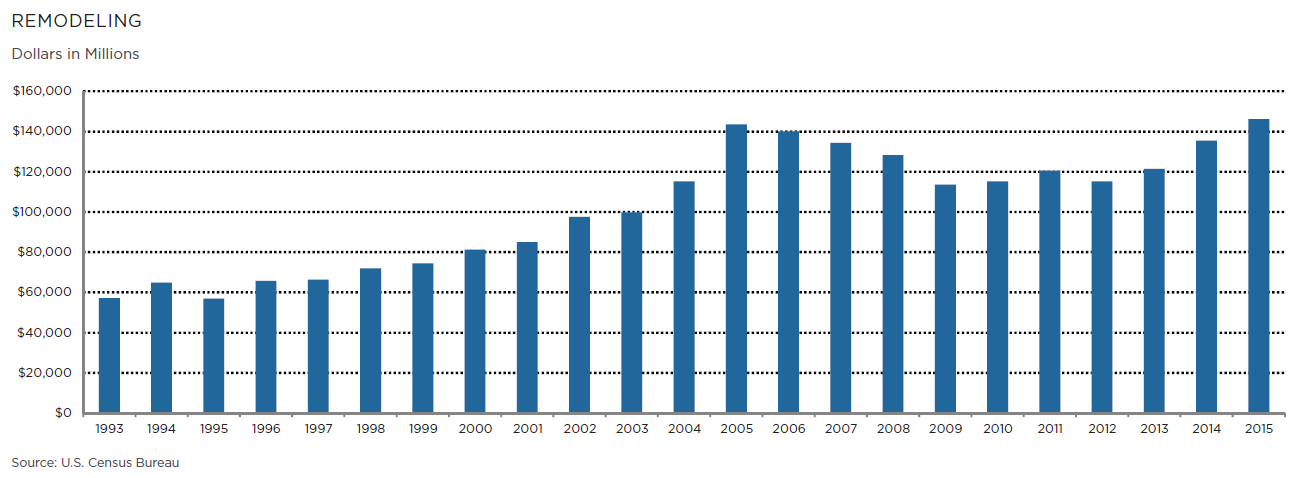

There is evidence that the later may already be happening CoreLogic says, citing the Remodeling Market Index from the National Association of Home Builders (NAHB) which has stayed above the 50 mark, indicating that remodelers are confident in that market, for 10 consecutive quarters. The Census Bureau estimates that there was $140 billion spent on remodeling in 2015, the highest number since 2005.

When borrowers do turn to HELOCs they find they are a different loan than before the crash. Back then they were a popular cross-sell and add-on product. "Soon after a client would get a first mortgage their lender would almost automatically follow up with a HELOC. It wasn't uncommon to see CLTVs of 100 percent and pricing at below prime. Similarly borrowers with small down payments were often presented with piggyback first and seconds as a way of avoiding mortgage insurance."

Once the crisis hit borrowers who fell into negative equity found their lines blocked and the presence of second liens prevented many homeowners from successfully negotiating mortgage modifications or short sales. Many of the homes with HELOCs eventually went into foreclosure.

There were more than 12.2 million HELOCs originated between 2004 and 2007. A significant number went into default along with the senior liens during the recession but millions remain active. Of the 4.1 million homes that were underwater as of the third quarter of 2015, 39 percent or 1.6 million had both first and second mortgages with an average mortgage balance of $307000. These were underwater an average of $85,000 versus $58,000 for those underwater homes with only one mortgage.

There has been a lot of concern that those legacy loans could eventually cause another wave of defaults and foreclosures as their open borrowing periods ended and payments reset to begin amortization. That appears to have been unfounded.

CoreLogic says there has been some increase in delinquencies related to resets but the problem appears to be manageable. Some lenders have proactively offered refinance programs to extend the interest only periods and many older lines have been refinanced into new first mortgages. The remaining smaller number of legacy HELOCs, however, may have a greater susceptibility to problems.

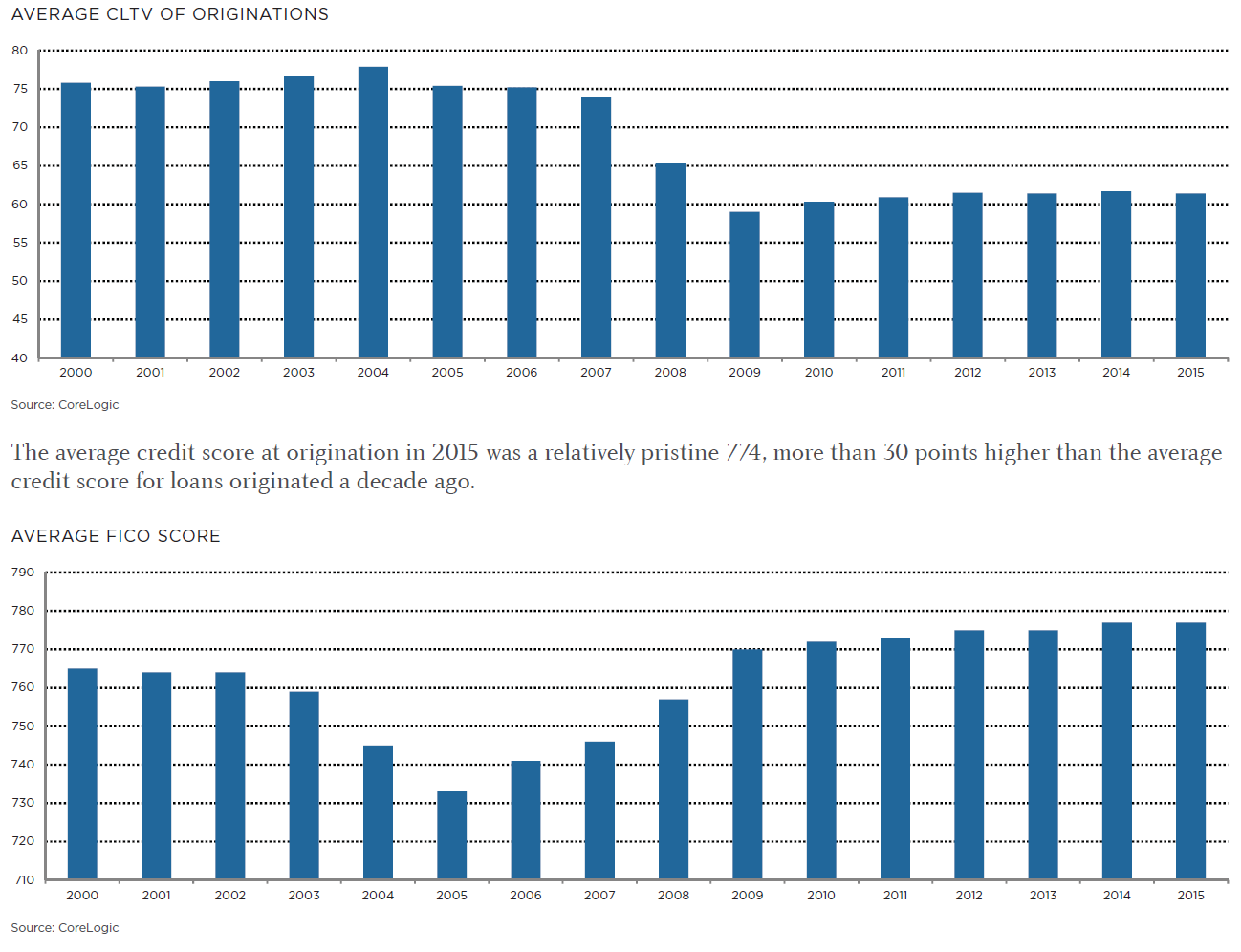

Today lenders are underwriting equity loans in a much more conservative manner than they did those legacy loans. Loans written in 2015 have an average CLTV of about 61 percent and the average credit score of the borrower was 774, more than 30 points higher than for a loan written pre-crisis.

Debt-to-income ratios (DTIs) remain in the 35 percent range where they have been since 2009. CoreLogic notes that while closed-end HELs fall under the ability-to-repay standard of the Qualified Mortgage rule with its 43 percent DTI ratio, HELOCs do not.

So far the performance of these new equity loans has been exceptionally good. Since 2009 the typical 60+ day delinquency rate at the 36 month point in the loan has been around 25 basis points, about half the delinquency rate in the early 2000s.

HELOCS on average are larger than they were pre-crash - $118,694 last year versus $105,016 in the 2004-2007 period - but the utilization rate is down; it was 65 percent last year compared to a high of 72 percent in 2010.

The white paper says that lenders face some issues of profitability if the volume of HELOCs continues to grow. This type of lending is typically marketed to the consumer as a no-cost product which makes pricing and costs of origination important.

For lenders pricing can be a double-edged sword. "They need to price for the risk that they are taking yet not price themselves out of the market and lose not only a loan but potentially a customer. In addition, higher pricing alone won't protect against adverse selection," the paper says.

There is a need to continually balance the cost of products and services used to underwrite loans with the perceived risks and to target customers who will access these lines early.

Small balance borrowers and consumers who take out loans "just in case" but don't use them are often unprofitable. Lenders are targeting consumers with enough equity to take out sizable liens and the propensity to actually use them. Consequently there is a move to using propensity models developed by several companies that help lender identify the best borrowers for these loans and if they are current customers update their credit information and with an estimate of income have enough confidence to make a pre-approval offer.

Lenders are also turning to a new approach, an invitation to apply, rather than the old "you have been approved" model of mass marketing. If a customer responds the lender can then pull credit and use a propensity model to select the top scoring homeowners who are most likely to take out a home equity loan in the next six months. This saves on the resources involved in targeting unqualified or uninterested consumers and some of those involved in underwriting the loans.