The overall delinquency rate on mortgage loans has now fallen below historic average levels. The Mortgage Bankers Association (MBA) said on Thursday that 4.77 percent of all mortgage loans on one-to-four-unit residential properties were at the end of the fourth quarter of 2015. That rate is a seasonally adjusted one.

The rate, gathered through MBA's National Delinquency Survey, represented a decrease of 22 basis points from the third quarter and 91 from the delinquency rate in the fourth quarter of 2014. It was the lowest level recorded by MBA since the third quarter of 2006. The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure.

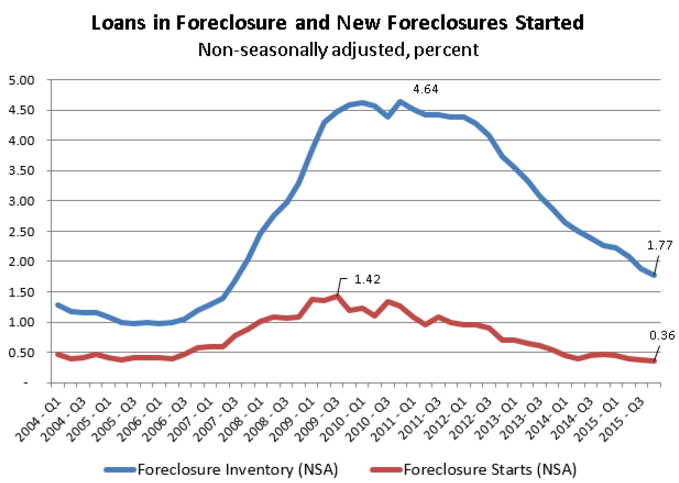

Foreclosures were begun on

properties at a rate of 0.36 percent, down 2 basis points from the previous

quarter and 10 from the previous year. This start rate was the lowest since the

second quarter of 2003.

Loans in the foreclosure process, sometimes referred to as the foreclosure

inventory, were at a rate of 1.77 percent at the end of the fourth

quarter. That was 11 basis points below

the inventory at the end of the third quarter and 50 points lower than on

December 31, 2014. The foreclosure inventory has not been that low since the

third quarter of 2007.

Serious delinquencies, loans that are 90 or more days past due, including those in foreclosure, represented 3.44 percent of all mortgages, the lowest rate since the third quarter of 2007. The rate was a 13 basis point decrease quarter-over-quarter and 108 points year-over-year.

Marina Walsh, MBA's Vice President

of Industry Analysis, said "As the job market has improved and national

home prices have rebounded, fewer borrowers were becoming seriously delinquent,

while borrowers previously behind on their payments were in a better position

to pursue alternative options to resolve delinquent loans.

Walsh noted that the overall delinquency rate is now back to pre-recession

levels, "and at 4.8 percent, was lower than the historical average of 5.4

percent for the time period 1979 to 2015. The rate at which new foreclosures

were started decreased to 0.36 percent, the lowest rate since 2003 and only

one-fourth of the record high level during the worst of the foreclosure crisis

in the third quarter of 2009."

"Mortgage performance is closely connected to job market health and most

states saw employment growth continue over the past year," she said. "However, there were increases in the

foreclosure starts rate in a handful of states that have economies closely tied

to the oil industry. Out of 12 states that had an increase in foreclosure

starts in the fourth quarter, five of those were in states with oil-dependent

local economies. Oklahoma, North Dakota, Louisiana, Colorado, and Texas saw

increases in new foreclosures while the national average continued to trend

lower.

"Foreclosure inventory rates continued to decline in both judicial and

non-judicial states. New Jersey and New York, which lead the nation in

foreclosure inventory rates, had the largest year-over-year declines in their

respective histories.