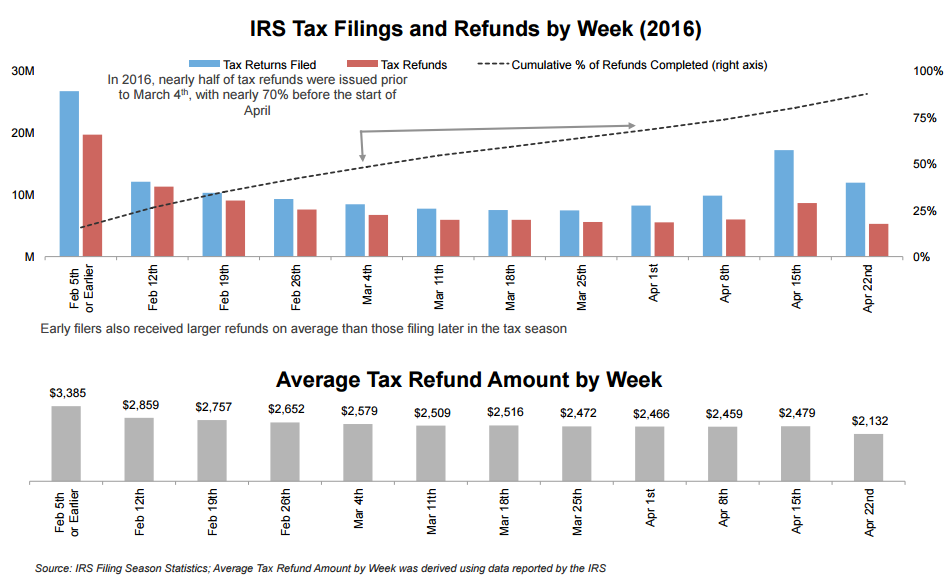

Apparently we aren't all procrastinators. Black Knight Financial Services looked at Internal Revenue Service (IRS) filing statistics and how they relate to loan level mortgage performance data for its current edition of Mortgage Monitor and found that 40 percent of tax filers are in and done by the first week in March. In fact, half of that number or one in five have finished and filed their returns within the first two weeks of tax season.

The company says incentive plays a role in this diligence as Americans who file early are more likely to be expecting a refund. On average, they also receive a larger refund than those who file later. The average refund for those filing on or before February 5th was $3,400, more than 35 percent higher than the refund for those filing in early April and nearly 50 per higher than those filing the last week of the season. In fact, IRS has already distributed most tax refunds well before the April 15 tax deadline.

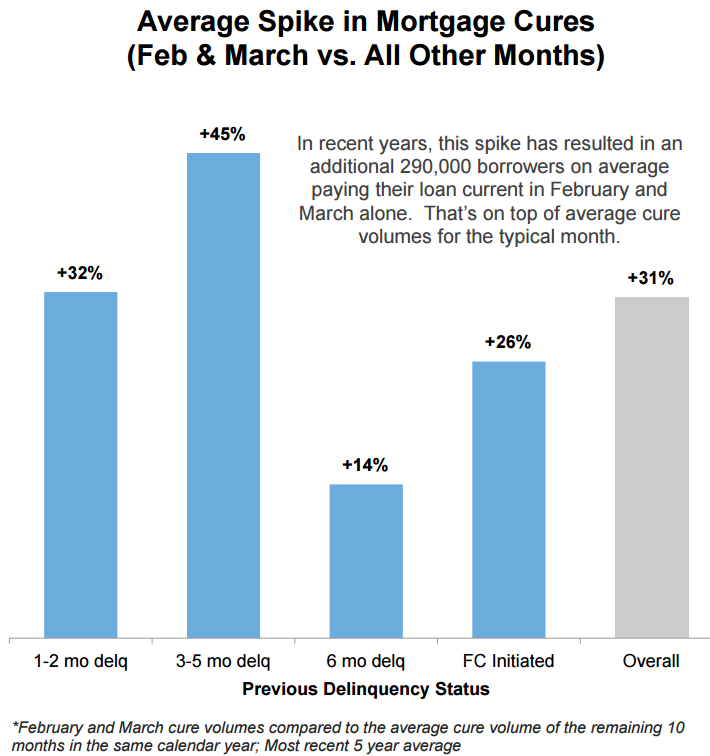

So, what does this have to do with mortgages? Black Knight says if history repeats, nearly 300,000 more borrowers can be expected to bring their delinquent mortgages current in February and March than in a typical month, and changes are they are using their tax refunds to do so. Black Knight Data & Analytics Executive Vice President Ben Graboske said, "We see this increase in cures across the delinquency and foreclosure spectrum, but it is most pronounced in the early and moderate stages of delinquency. This makes sense, in that a tax refund may be sufficient to pay a few months of past-due mortgage payments, but is likely not enough to bring a homeowner out of severe delinquency. Likewise, the most pronounced impact was seen among FHA/VA borrowers, who might be expected to have less cash reserves on hand and therefore be more dependent upon the infusion of funds during tax refund season to pay down late payments. All things being equal, there's no reason to expect this tax season to be any different."

That mortgage delinquencies fluctuate on a seasonal basis is well known, but Graboske points out the FHA and VA loans see the most pronounced seasonal variations throughout the year. March is the seasonal low for mortgage delinquencies, and FHA and VA loans improve the most during the period with loan cures increasing by an average of 40 percent. In contrast, GSE loans cures go up by just 26 percent. Then winter brings the most adverse seasonal impact and again these are highest among those two loan types. He says, "While the inflow in early spring from tax refunds gives these borrowers a needed infusion of funds, the data also shows they tend to struggle more when the funds burn off late in the year and money becomes tight around the holiday spending season."

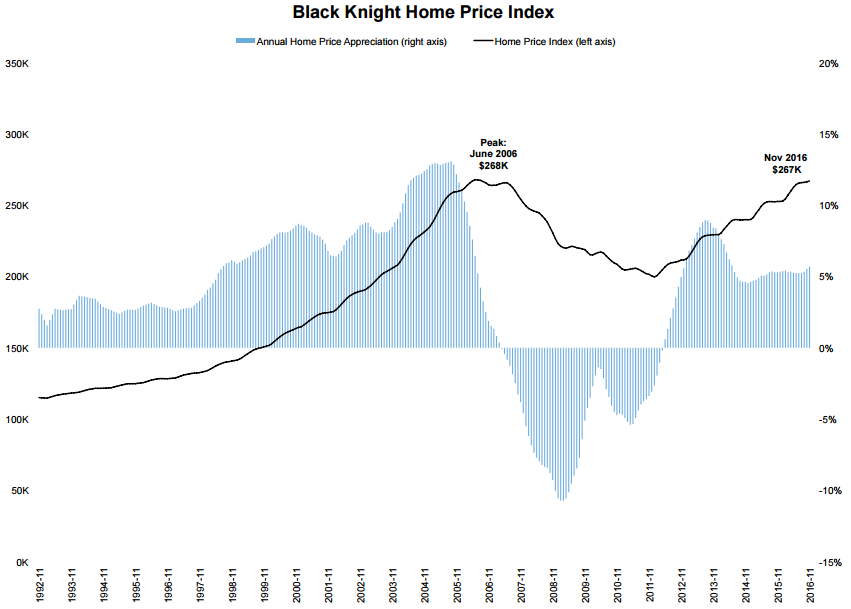

Black Knight also looked again at home affordability and how it has been affected by the current interest rate environment and continued home price appreciation. Home prices were up in November by 5.7 percent on an annual basis, marking 55 months of annual growth and the highest rate of appreciation since June 2014. Prices are now only a fraction of a percentage point off the June 2006 peak, roughly $864 on average away from that milestone. If the 2016 pattern of a price increase every month holds true for December, 2016 will join 2013 as the only years since 2005 where prices have increased each and every month.

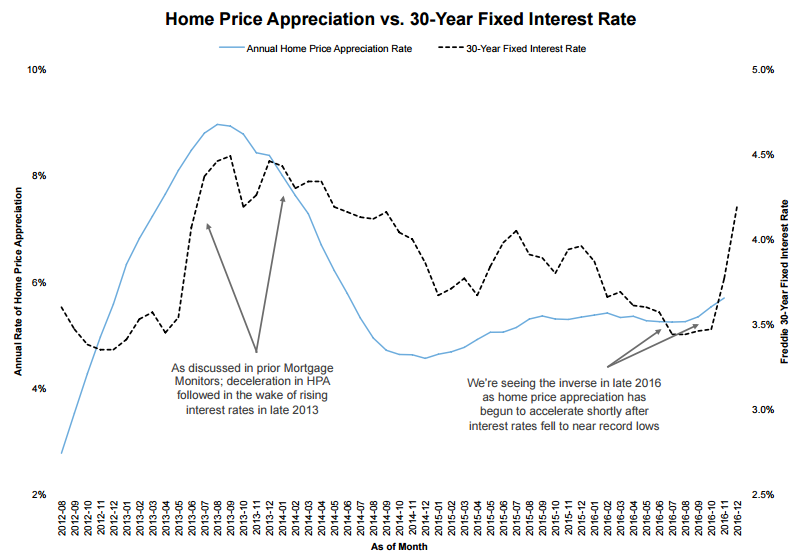

Price appreciation was beginning to accelerate in November, which the Monitor attributes to the declining interest rates in the second half of 2016 prior to the election. This, it says, suggests borrowers were willing to pay more for the same home than they were prior to the rate decline early in the year, and indicating that rather than absorbing the effects of lower rates as savings they were opting to use the increased buying power to bid up home prices. While condominiums still appreciate at a slower rate than single family residences, price gains there have also shifted into acceleration over the past four months

The Monitor says while the historically low interest rates have helped accelerate home price gains, interest rates on 30-year mortgages rose by 75 basis points in November alone. With the prevailing interest rate of 4.19 percent at the time the analysis was done, January 26, 2017, housing is now the least affordable it's been since 2010, "requiring 22.2 percent of the median income to make the monthly principal and interest payment on the median- priced home." This is an increase of 10 percent just in the fourth quarter of 2016. On a national basis homes remain more affordable than they did pre-bubble, "but it's clear that the market is now experiencing the most pressure - from an affordability perspective - since the housing recovery began. "

The Monitor reminds of analysis in prior editions where marked deceleration in price increases was observed in the wake of the "taper tantrum" interest rate increases of late 2013. A similar reaction has yet to materialize today, although based on recent history, home price movement following changes in interest rates have been lagged by 2 to 3 months.