CoreLogic continued its series of blog articles related to appraisals with an analysis of the appreciation rate when an appraisal has come in above the sale price versus a sale where the appraisal falls short. Principal Economist Yanling Mayer says when an appraisal doesn't match the sales price then buyers probably think either they overpaid for their house or that they got a bargain. If either is true, then should they expect either a below market rate of appreciation in the former instance or above-average appreciation in the latter?

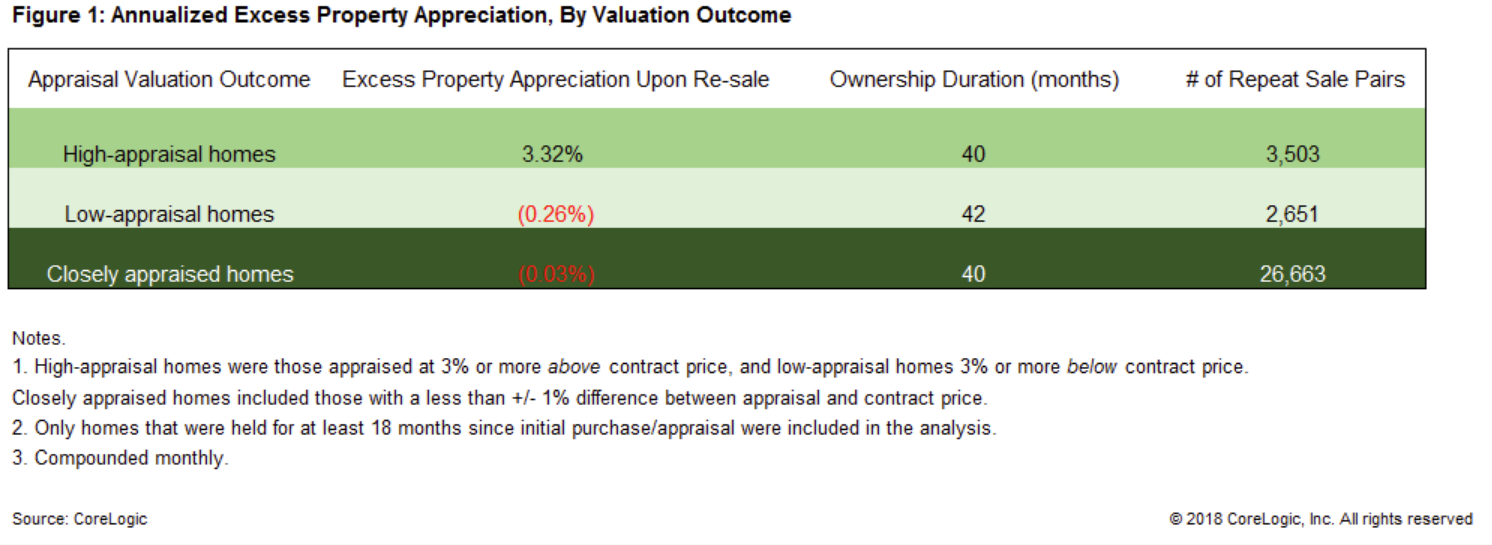

Mayer says evidence seems to support the hypothesis that there is "money left on the table" in high-appraisal transactions. CoreLogic looked at appreciation for houses in California that had sold twice post 2010. Homes that appraised during the first sale with a sizable premium above the contract sales price were found to have above-market appreciation rates.

The extra appreciation averaged about 3.3 percent over the market rate per year. Those homes that had appraised at close to the sales price gained value only factionally different from the market average, while homes with low-ball appraisals saw value grow about 0.3 percent slower than the market rate. These were annualized percentage differences between the first and second sales in excess of average market appreciation during the same ownership period.

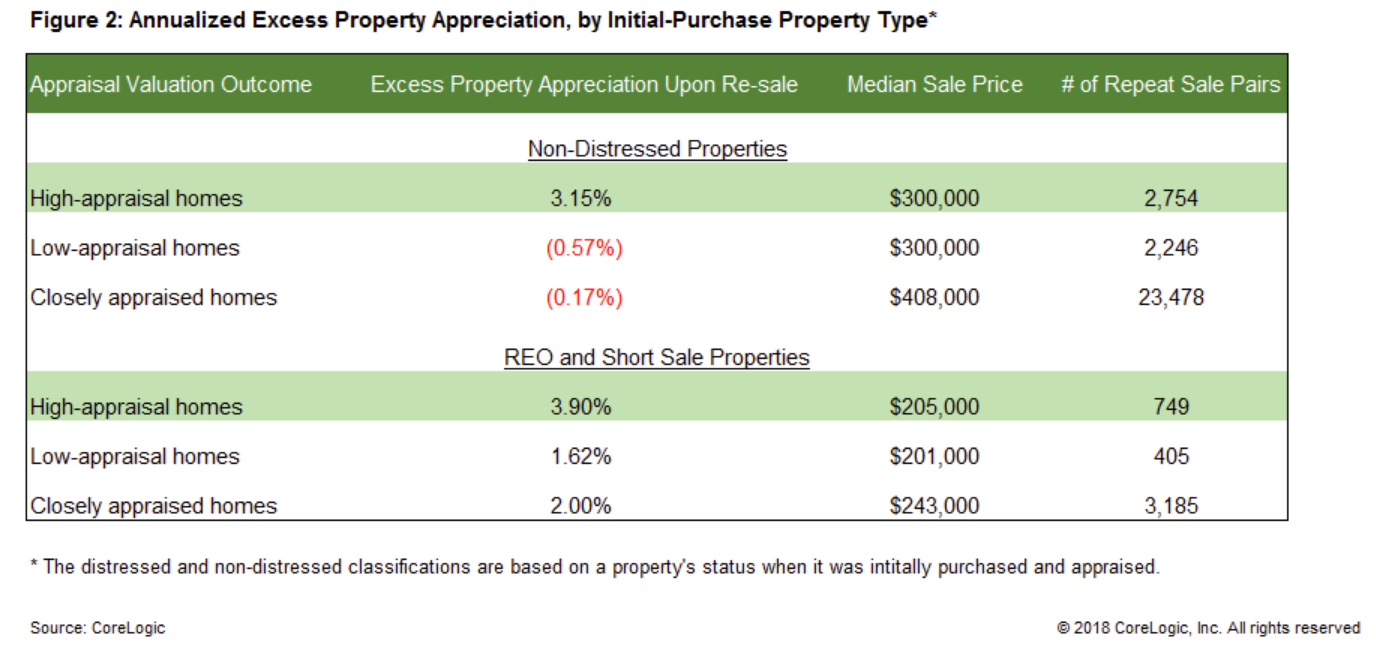

Within the 3.3 percent excess appreciation in higher appraisal homes were differences between homes that sold as distressed properties and those that did not. The extra appreciation among non-distressed sales averaged 3.15 percent while it was 3.9 percent for real estate owned (REO) and short sales. Those distressed sales also exhibited higher appreciation rates regardless of the appraisal to sales price ratio, likely driven by their below-market pricing to motivate sales. Work done by investors to enhance value could also be a factor despite that only homes that were held for at least 18 months between sales were included in the analysis, excluding flips.

The median sales price of closely appraised homes was higher than the median prices for the above and below appraisal properties. This was true whether the properties were distressed or not. Mayer says both high- and low-appraisal homes may have been drawn disproportionately from lower-priced homes, so even in a market where lower priced homes have appreciated the fastest, that alone could not explain away the large disparities in price appreciation between the two.

In Figure 3, sample homes were further sub-grouped by the year in which they were initially purchased and appraised. Given the significant market dynamics during 2010-2015, property appreciation rates were likely to vary depending on the timing of initial purchase. They ranged between 2 and 5 percent, reaching the highest during the 2012 market bottom when market-wide underpricing was likely the severest.

Mayer concludes, "Regardless of the reason(s) why a home may have sold for less than its appraised value, the buyers appear to have benefitted by having a faster-than-market appreciation during their ownership tenure."