Although they covered the topic in last month's Mortgage Monitor, further declines in interest rates have prompted Black Knight to take another look at the impact on the refinance pool. The previous edition reported that the 30-basis point drop in the 30-year fixed rate mortgage from a post-recession peak in November to 4.55 percent by the end of December had boosted the pool of borrowers who could qualify for and benefit from refinancing by more than a half million. At that point the pool had returned to 2.4 million homeowners who could reduce their rate by at least 0.75 percent.

Since then the rate has fallen to 4.45 percent, the lowest since last April, and the refinance pool has grown to 2.9 million, 1 million more than when rates were at their peak, and the largest this population has been since January 2018. Black Knight says, "Even if rates should hold steady - and certainly if they fall further - this could lead to an unexpected bump in refinance volumes in early 2019.

Of course, any bump is predicated less on who might refinance rather than on who will. Forty percent of those who have regained their refinance incentive (424,000) took out their current mortgage between 2009 and 2011 and 75 percent of the incentive gains would be on loans originated pre-2011. In fact, about 90 percent of all refinancing incentive is held by borrowers with loans originated prior to 2011.

Black Knight points out that a large portion of those homeowners would have benefited from refinancing for a long time and when rates were even lower but have not done so. This suggests that the incentive to refinance may not be as strong as the numbers indicate. On the other hand, rates for home equity lines of credit (HELOCs) are rising, so homeowners wishing to tap equity but who haven't done so because of the rising cost of doing so may opt to cash out through full refinancing this year.

Loans held in private label securities (PLS) are generally the ones that would benefit the most from refinancing, with 12.1 percent of loans falling into the pool. Those owned or guaranteed by Fannie Mae or Freddie Mac have grown the most since November. The lowest refinance/prepayment risk is among portfolio loans, but their small overall numbers means the 1.4 percent increase represents an 81 percent increase in population. Portfolio loans, especially those originated in recent years, tend to have higher credit score and larger balances, perhaps giving borrowers more reason to respond to the renewed incentives.

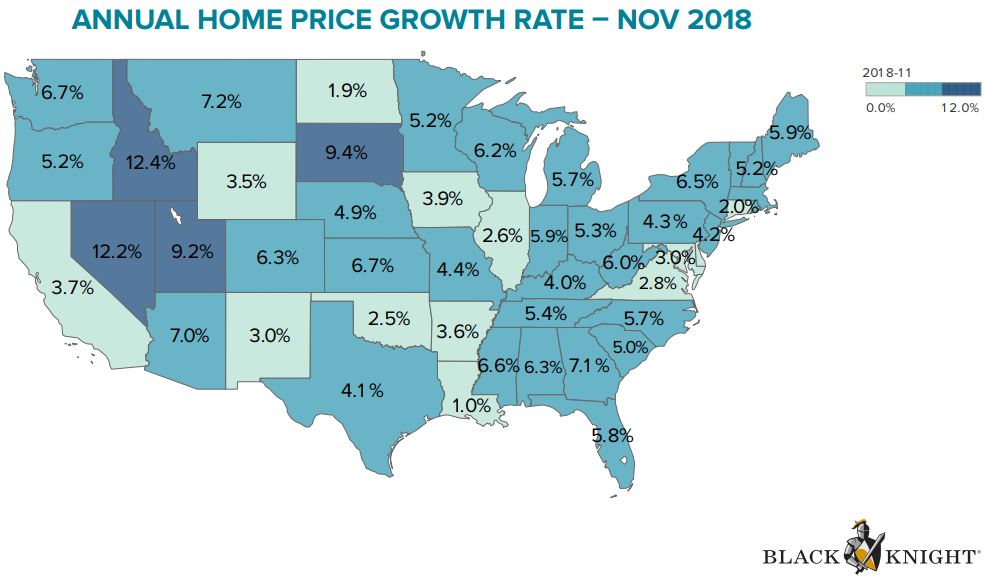

Home prices were also addressed by the Mortgage Monitor for the second time in as many issues, as their slower rate of growth becomes more apparent. The average home prices declined by 0.2 percent or $580 in November. It marked the first consecutive three-month pullback in prices and the largest single month decline since early 2012. The average home price is now down $1,361 since August. The annual rate of appreciation also slowed in November, falling another 0.4 percent to 4.9 percent. In February 2018 the annual rate of appreciation peaked at 6.7 percent.

Black Knight points out that the 30-year mortgage interest rate was at the highest average in over 7 year making the monthly mortgage payment at that point the least affordable in nearly a decade.

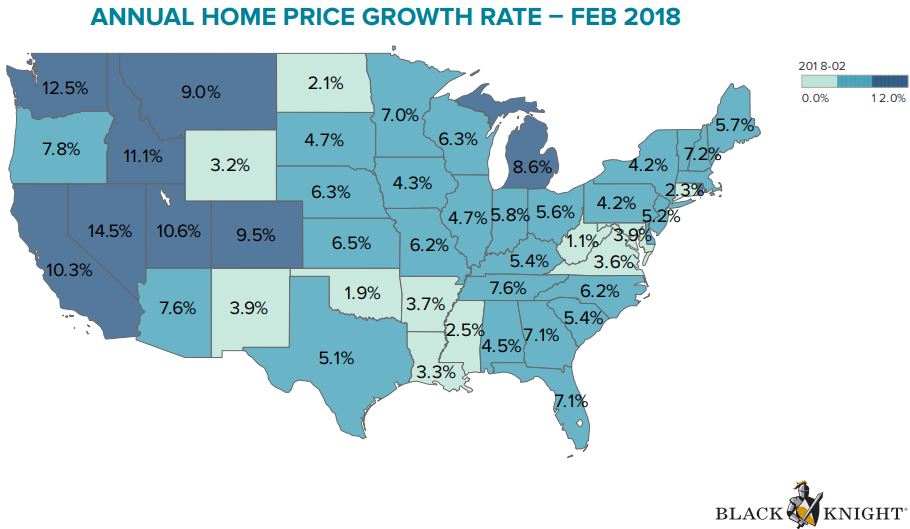

Despite recent declines prices remain higher than a year ago in all 50 states and all but one of the 100 largest housing markets. Still, the rate of appreciation is down in 36 states and 78 markets with the greatest degree deceleration in the West. The annual rate in California declined from 10.3 percent to 3.7 percent in just nine months while Washington State slowed to 6.7 percent from 12.5 percent over the same period. These changes have brought home price growth into more uniformity nationwide.

The combination of softening home prices and lower rates have improved the home affordability outlook for 2019. While the P&I payment on an average priced home is more than 10 percent higher than in January 2018, it has declined by $56 since November. Assuming a 30-year mortgage at 4.45 percent, that payment is now $1,192.