Freddie Mac's economists are expressing concerns about what they see as economic headwinds revealed by some recently released indicators. In their current edition of Insight and Outlook the company downgraded its full year estimate for 2015 real GDP growth by a tenth of a point to 1.9 percent while calling the current expansion the weakest in postwar history. They project growth in 2016 and 2017 at 2.5 and 2.3 percent respectively making them the sixth and seventh years of sub-3 percent growth.

The economists base their negative outlook on several factors, global growth, particularly in China; disappointing automotive and retail sales and wage growth, and energy prices. Their negative outlook, however, does not extend to housing.

First of all they see turmoil overseas having an upside for housing, exerting downward pressure on interest rates. They see those rates continuing to drift down in the short term, as they have since the beginning of the year, before reversing course and rising modestly for the rest of 2016. They have lowered their projections for the full year average by a tenth of a percent to 4.3 percent.

Even with this projected increase the historic low levels should help sustain housing sales and construction this year. The real constraint on sales will continue to be tight inventory and that lack of product will in turn create pressure on home prices in some areas. Still the report anticipates that in other areas increasing inventory and rising interest rates will dampen demand. They project house price gains of 4.4 percent and 3.5 percent in 2016 and 2017 compared with an estimated national increase of 6.0 percent for all of 2015.

Purchase mortgage originations, based on solid home sales and strong house gains are projected to be "robust" this year as will home improvement originations; together rising by about $117 billion or nearly 13 percent. The economists say 3.7 percent of that increase will be a function of higher home sales and 4.4 percent from higher home prices and a reduction in all-cash sales. In 2017 there will be an additional increase of $83 billion in these originations to $1.11 trillion.

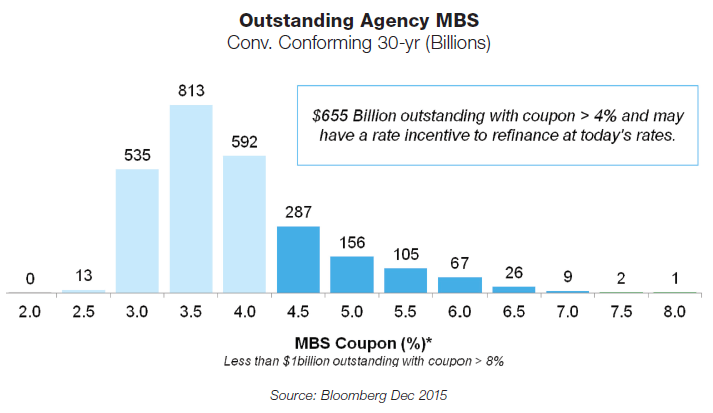

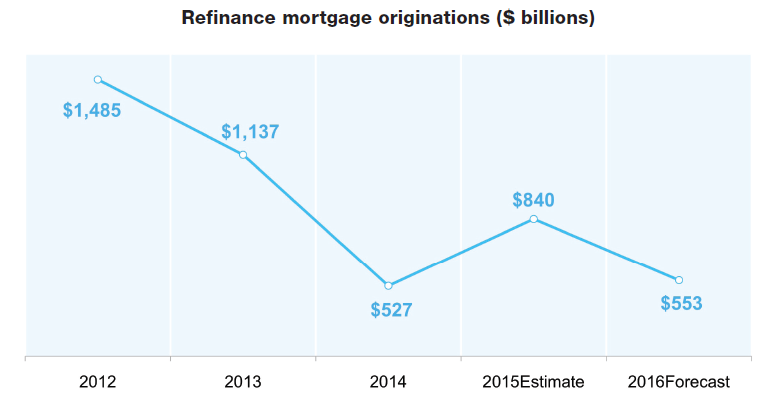

The report calls refinance originations the big uncertainty. It is pretty much a given that increasing interest rates will reduce rate and term refinances, but even there they are hedging their bets. They quote data from Bloomberg, there are $655 billion in outstanding conventional mortgage-backed securities (MBS) with coupon rates exceeding 4 percent. Freddie Mac says, "Many of those mortgages were originated years ago and the borrowers have failed to refinance even though mortgages rates have dropped steadily. However, we believe there are good reasons to expect some of them to refinance in 2016."

First, many of these homeowners found themselves underwater during the Great Recession so were unable to refinance without bringing cash to the table. CoreLogic estimates there are still about 5 million underwater homeowners, some of which turned to the Home Affordable Refinance Program (HARP) to help them reduce rates but many borrowers did not qualify for the program. Solid home price growth has been "replenishing" much of this lost equity and continued gains could lower potential borrowers' loan to value ratios enough they may soon be able to refinance.

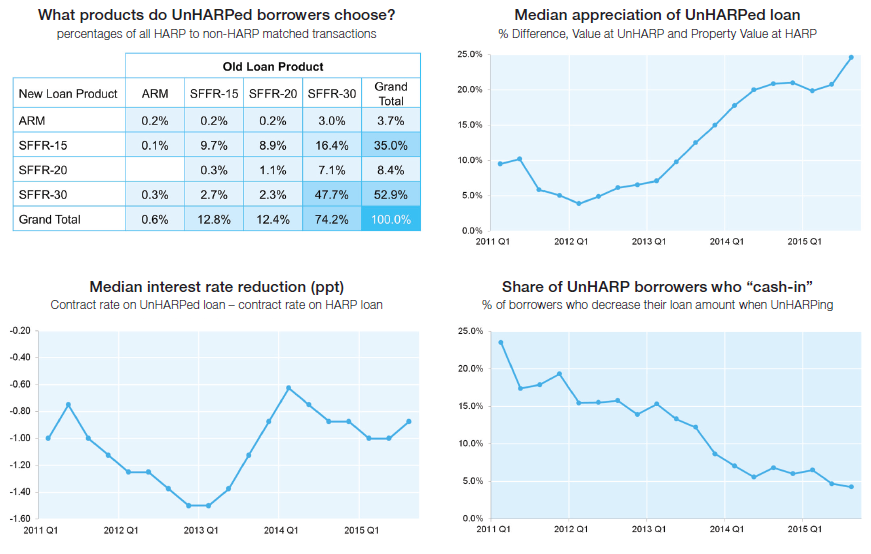

Related to this is what Freddie Mac calls "unHARPing." There were an estimated 3.4 million homeowners who did take refuge with HARP loans and those who did so between 2009 and 2012 likely have an interest rate over 5 percent. Many are now in a position to refinance into lower interest conventional loans and this, Freddie Mac says, has already begun. About 10 percent of HARP borrowers have switched and with about 2 million active HARP loans still out there, there is substantial potential for more refinancing from that source.

Freddie Mac looked at the "unHARP" transactions where it funded both the HARP loan and the refinance and found some key trends such as a switch to shorter term loans and fewer borrowers needing to bring cash to the table. Some of these trends are indicated in the charts below.

Freddie Mac also sees other potential sources of continued refinance activity. While adjustable rate mortgages (ARMs) represent only a very small share of the mortgage market today, these loans were very popular during the housing bubble. Many borrowers are facing a first reset and may refinance into a fixed product to limit risk. Over $54 billion in hybrid loans are due to reset this year.

Home equity lines of credit (HELOCs) were also a popular way to take cash out of homes during the bubble and those loans approaching their tenth anniversary are also facing the end of their interest-only open periods and will begin amortizing, probably with a substantial increase in monthly payments. CoreLogic estimates there will be about $100 billion in HELOC loan resets between the fourth quarter of 2014 and Q4 2017 and Freddie Mac says it expects substantial HELOC consolidation to reduce rate shock.

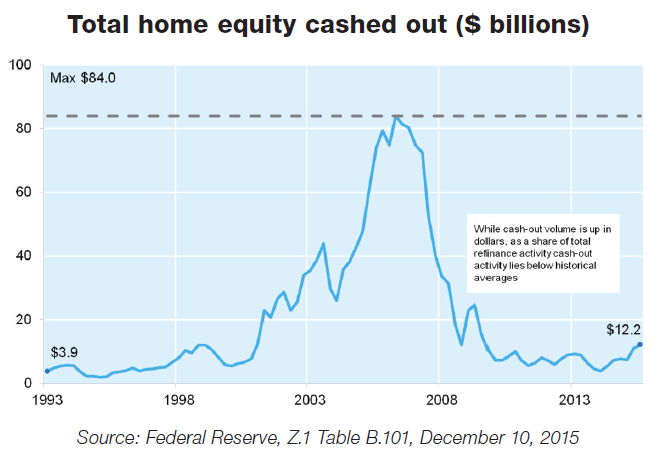

Cash out loans are reviving although they are still well below the frantic pace prior to the housing crisis. The company estimates that borrowers cashed out an estimated $12.2 billion in the third quarter of 2015 and could add an additional $100 to $200 billion in refinance activity this year.

The bottom line; Freddie Mac does see the refinancing share dropping this year and next but remaining at still respectable levels of 35 percent and 24 percent respectively compared to 48 percent for all of 2015.