Fannie Mae's Economic and Strategic Research Group (ESR) focused on the new Tax Cuts and Jobs Act, passed late last year, in its January Economic Developments report. Like most other economists, Fannie Mae's are upgrading their growth forecasts based on the impact of the bill. Between October 2017 and this month, the average forecast for 2018 real gross domestic product, some based on speculation about what the bill would ultimately contain, moved 0.3 percent higher, to 2.7 percent. The rationale for the forecasts is that cuts in individual tax rates should help push consumer spending, while reductions in corporate tax rates and allowing equipment investment to be fully expensed for five years are expected to boost that spending.

The new law "will create winners and losers in the housing market," the report says. By increasing disposable household income, the demand for housing is likely to increase, but incentives for homeownership are reduced. The bill rolls back the size of a loan for which the mortgage interest deduction (MID) applies from $1 million to $750,000 and limits the deductibility of state and local taxes (SALT) and property taxes to an aggregate of $10,000. At the same time, the personal exemption is doubled to $24,000, further reducing the incentive to itemize.

The overall impact of the new bill on final tax payments will have vary significantly for households across the nation, and it is not known how taxpayers will choose to spend their increased disposable income. Will they save it or use it to pay down debt? While it is difficult to estimate how consumers will react to the windfall, the impact of the 2001 and 2008 tax cuts can be a guide. Fannie Mae expects real consumer spending growth to pick up by two-tenths of a point in both 2018 and 2019, to 2.7 percent and 2.5 percent, respectively. The saving rate, which dipped three-tenths in November to a post-recession low of 2.9 percent, should trend up because of the tax bill. Thus, while the tax cut may not boost consumer spending substantially because some taxpayers will choose to save the windfall or use it to pay down debt, it would help provide a savings cushion for rainy days and strengthen household balance sheets. Perhaps even provide funds for a downpayment.

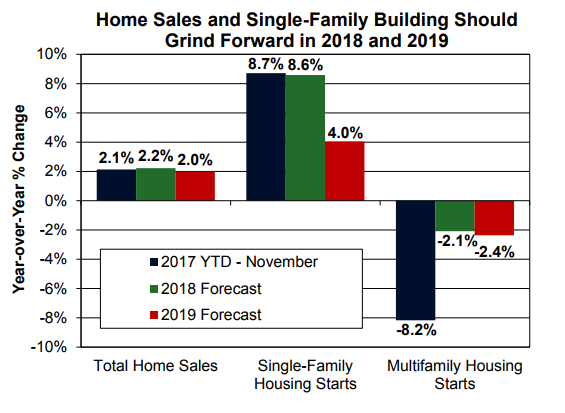

The single-family housing market near year-end was upbeat. Both single-family permits and starts rose in November to the highest levels in more than a decade. For the year to date through November, starts were up 8.7 percent compared to the same period in 2016. Multifamily building appears to have peaked; year-to-date starts in that sector were down 82 percent from the same period the previous

Existing home sales were also strong, a third consecutive month over month increase carried those sales to the highest rate in nearly 11 years, up 1.4 percent from November 2016. New home sales were at the highest rate since July 2007, a 9.0 percent annual increase.

Fannie Mae expects the tight inventory of available homes will continue to restrain home sales, even with the positive income effect from the tax cuts. The number of existing homes for sale in November was down 9.7 percent from a year earlier and has fallen year-over-year for 30 straight months. The number of available homes was estimated at a 3.4-month supply, the lowest since the National Association of Realtors started tracking the number in 1999.

The tax bill could negatively affect home prices in the high-end market; however, this segment accounts for a very small share of the total market and should have limited impact on overall home price appreciation.

The ESR is forecasting two to three rate hikes by the Federal Reserve Open Market Committee (FOMC) this year, one in March, another in September, with the Fed waiting for evidence of increased inflationary pressure before picking up the rate of increases. A third increase this year is quite possible.

Mortgage interest rates will rise only modestly over the next year, averaging 4.1 percent in the fourth quarter of 2018, up from 3.9 percent in the last quarter of 2017. Total housing starts should increase about 5 percent this year, solely because of the single-family segment, as multifamily starts are projected to decline further. We expect total new and existing home sales to rise about 2 percent, similar to the gain through the first 11 months of 2017. Total single-family mortgage originations should gain by about 5 percent this year to $1.73 trillion from an estimated $1.83 trillion in 2017, with a 7-percentage point decline in the refinance share to 31 percent in 2018.

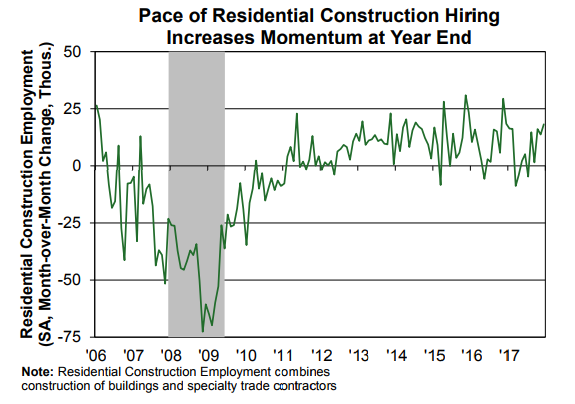

The economy added 2.2 million jobs in 2017, the seventh straight year new jobs exceeded two million, and Fannie Mae expects an average monthly gain in 2018 of about 186,000. This is an increase of 10,000 from their previous forecast. One bright spot in the December jobs report was the largest gain of the year in residential construction. This provides some hope for increased inventories of new homes. Fannie Mae is expecting the unemployment rate to average 3.7 percent in the second half of 2019, which would be the lowest level in fifty years. They have also revised their growth forecast for 2018 by 0.6 percentage point to 2.7 percent and their 2019 forecast by 0.5 point to 2.3 percent.