Last year's Federal Reserve actions, raising the target interest rate three times, led to about a 0.75 percentage point increase in the 1-year Constant Maturity Treasury (CMT) note, while the 10-year CMT note barely moved. Freddie Mac's Economic and Housing Research group says this flattening of the yield curve could be a bad sign for future economic growth. Especially should that curve become "inverted."

Freddie Mac says they don't expect the trend to continue, instead they expect long-term rates will also follow the Federal Open Market Committee's (FOMC's) anticipated actions in 2018, for three or four more rate hikes, and head higher.

Writing in the current edition of Outlook, the economists say the new Tax Cuts and Jobs Act bill's lower corporate tax rate should boost GDP growth by a about a quarter point this year. Along with continuing job growth, this should will lead to a modest uptick in consumer price inflation, allowing the FOMC to institute rate hikes gradually.

Will higher rates derail the housing market? A spike like that in the spring of 2013 would certainly slow it down, they say, but the expected gradual increase should allow the market to maintain momentum. They also expect some impact from the tax reform bill.

With the doubling of the standard deduction and a lower cap on the mortgage interest deduction (MID), the new law reduces to incentives to own rather than rent, and will, on the margins, lead to fewer homebuyers. However, there will also be a countervailing impact from higher after-tax incomes and a general macroeconomic effect.

One way to think about the tax impact on housing markets is to consider the user cost of housing, which reflects the true economic cost of homeownership. They suggest a calculation of those costs, which appears to mirror those the Urban Institute provided last week, and predict where those calculations are averaged across households, the direct impact is rather small-something on the order of a one-time one percentage point reduction in housing values.

Even if that one-point reduction hit all at once, it's not clear how house prices would react. They are currently moving higher at about a 7-percentage point annual rate, a rate that is accelerating in some markets. Housing markets are out of balance, with demand seriously higher than supply. "In much of the country, the direct impact of the tax reform bill on housing markets will be difficult to see as it phases in amidst rapidly rising home prices."

However, if the tax reform bill significantly stokes growth and/or inflation, then mortgage rates might spike. "That would have a significant, measurable, and almost immediate negative impact on housing markets."

Freddie Mac says its baseline forecast is "sanguine" about the outlook for the economy and housing markets. But things could go wrong, and they name three of them.

Is There Another Recession on the Horizon?

Freddie's economists aren't saying one is imminent, but they do see signs. The expansion is aging, and as the cycle grows longer "there are more opportunities to sow the seeds of the next recession."

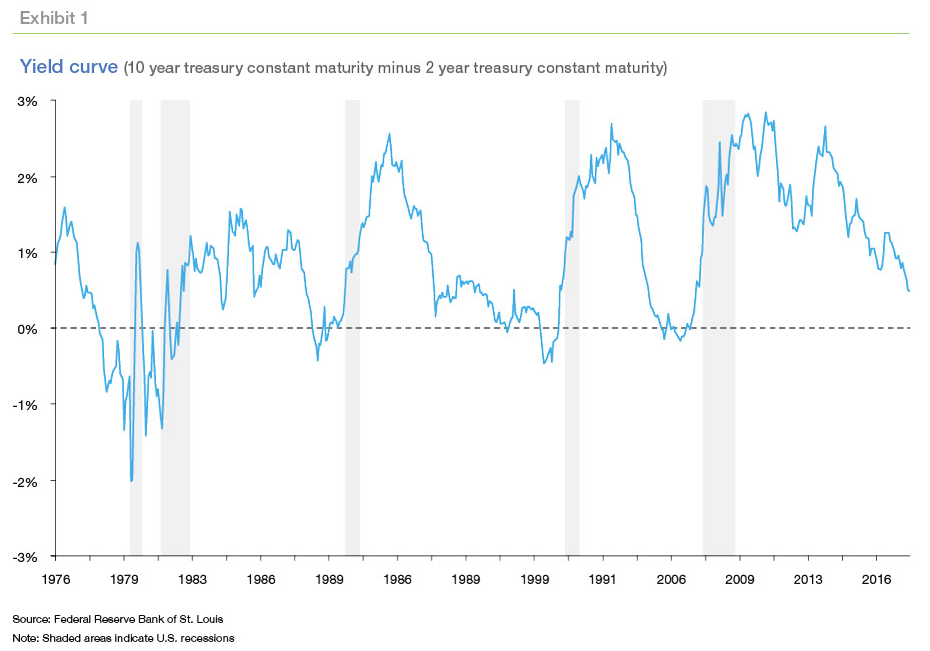

One sign is the slope of the U.S. Treasury yield curve which will usually rise with maturity. That is, a two-year note will yield less than a 10-year note. However, if that relationship inverts, banks have difficulty earning profits and generally constrict credit, typically leading to a recession. This, the economists say, is one of the more reliable indicators of a recession.

As stated above, the curve has flattened recently. While it isn't inverted. financial markets can change quickly. Were the FOMC to raise the target rate, yet other economic factors kept long-term rates from following suit, then the curve could invert.

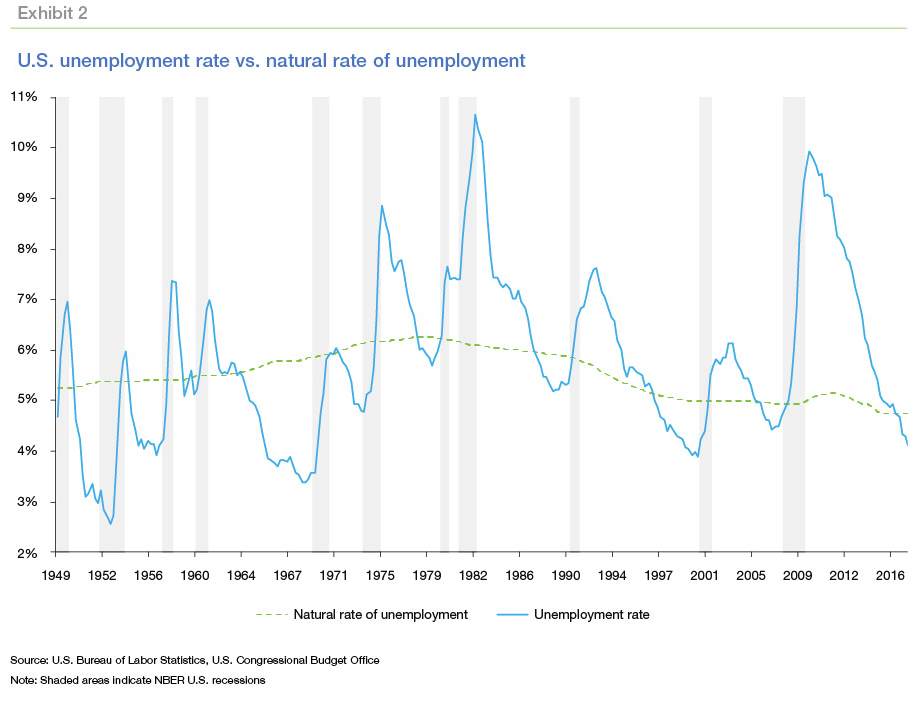

The hot labor market is another troubling sign. The 4.1 percent unemployment rate, which has held steady for several months, is well below what the Congressional Budget Offices considers to be its natural rate. However, the picture is muddled by the lack of wage inflation and the slow recovery of the employment-to-population ratio which indicate there is still some slack in the labor market. Still, history shows that an unemployment rate that stays below the natural rate for an extended period is typically followed, in two to three years, by a recession.

Although a recession does not appear imminent, we should watch, and not discard, potential recession indicators. For example, if the FOMC goes forward with rate hikes in 2018, do long-term rates increase, or does the yield curve flatten further? If the yield curve flattens further, then Freddie Mac says its outlook may sour.

How will Housing Markets Respond as Affordability Declines?

Economic growth will probably fail to push income gains enough to keep pace with rising house prices, and affordability will decline from the historic levels enabled by low interest rates. How will housing markets respond?

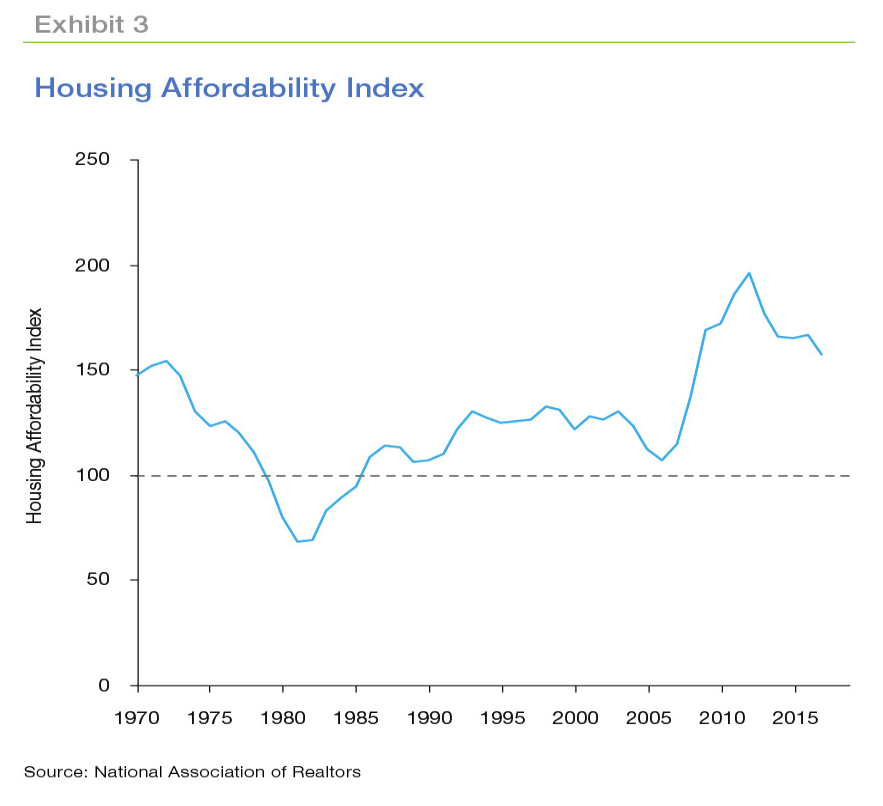

The Housing Affordability Index (HAI) constructed by the National Association of Realtors (NAR) reports the ratio of median family income required to qualify for a conventional mortgage on the median-priced home. A value of 100 indicates the median family income is just enough to qualify for the mortgage. Higher values mean the median-income family has more than enough to qualify. Exhibit 2 shows the annual HAI from 1970 through September 2017. The HAI peaked in 2012 and has been generally declining since. It still is well above its historical average.

Current levels of demand means the housing markets can absorb higher mortgage rates and home prices while sales continue to grow. But eventually declining affordability will impact sales. How long will that take?

How will young adults move the housing market?

Demographic forces provide significant tailwind when housing markets confront higher interest rates house prices, and rents. Will those forces help in the current scenario, where young adults have been slow to form households and purchase homes? Will demographics move the housing market this time?

Homeownership decisions are driven by a lot of factors and in recent years marriage and fertility rates have declined, education patterns have changed, as have choices about where young people prefer to live. Freddie Mac says more analysis is needed to determine if and when Millennials will move into homeownership and will take up the issue in next month's Outlook.