The National Association of Home Builders released the monthly Housing Market Index today.

Derived from a monthly survey that NAHB has been conducting for more than 20 years, the NAHB/Wells Fargo Housing Market Index gauges builder perceptions of current single-family home sales and sales expectations for the next six months as "good," "fair" or "poor." The survey also asks builders to rate traffic of prospective buyers as "high to very high," "average" or "low to very low." Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

Excerpts from the Release...

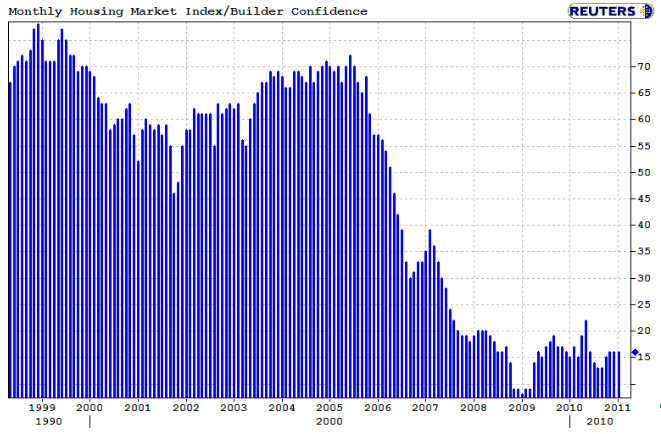

Builder confidence in the market for newly built, single-family homes held unchanged at a relatively low level of 16 for a third consecutive month in January.

Regionally, HMI scores rose by one point in the Midwest and four points in the West in January, to 14 and 15, respectively. Meanwhile, HMI scores fell two points in the Northeast and one point in the South, to 20 and 17, respectively.

While the HMI components gauging current sales conditions and sales expectations for the next six months both held steady from the previous month, at 16 and 25, respectively, the component gauging traffic of prospective buyers edged up a single point to 12 in January.

NAHB Chairman Bob Nielsen says..

"As we emerge from the traditionally slow holiday season, builders continue to look for signs of improvement in the economy, home buyer demand and builder and consumer credit conditions. Unfortunately, a severe lack of construction financing, and widespread difficulties in obtaining accurate appraisal values, continue to limit builders' ability to prepare for anticipated improvements in buyer demand in 2011."

NAHB Chief Economist David Crowe says...

"The HMI and its subcomponent indexes are holding steady following a below-expectations finish in 2010. At this point, housing remains on the sidelines of a weak economic recovery as consumers and builders wait for clear and consistent indications that jobs and economic output are reviving. Meanwhile, the problems that builders continue to confront in obtaining production financing, and in maintaining performing lines of credit, threaten to significantly slow the onset of a housing recovery."