It ain't over 'til it's over, and that seems to be increasingly true of contacted home sales. Trulia reported on Wednesday that, "Deals to sell homes are falling through at a faster rate than they were a year ago and it's agreements for starter homes that are most at risk."

The company reviewed the daily status of all listings for the first two months of each quarter from the fourth quarter of 2014 through the fourth quarter of 2016, looking for properties that went from a pending or active contingent status back to being for sale either by an agent or an owner. They sought to determine where it was most common for properties to go from under contract back to for sale status. They call these "sale fails."

The analysis found that the proportion of listings that fail at least once has been rising nationally at an increasing rate, from 1.4 percent of all listed properties in the fourth quarter of 2014 to 4.3 percent in the same quarter of 2016. Most of this increase occurred after the fourth quarter of 2015. The failure rate for all of 2016 was nearly double that of 2015 - 3.9 percent compared to 2.1 percent.

Sales of newly constructed homes were least likely to fall apart and very old homes had the second lowest failure rate. As of the fourth quarter of 2016 homes built in that year had a contract failure rate of 2.6 percent while the rate for homes built between 1900 and 1920 was 3.5 percent. The highest rate was for homes built from 1959 through 1969, 5.2 percent.

Starter home sales were also among the most failure prone in the fourth quarter of 2016, accounting for an average of 7.1 of all listings in the largest 100 metros, compared with 6.7% of trade-up homes and 3.8% of premium homes. For all of 2016, the failure rate was 6.3% for both starter and trade-up homes and 3.6% for premium homes.

Trulia offers several explanations for what they see as an increasing failure rate. One is the experience of the buyer. The National Association of Realtors® (NAR) reports that first-time homebuyers, who had been missing in action for some years, accounted for 35 percent of sales in 2016, up from 32 percent in 2015. Note, that this is their share only of successful transactions. Tulia says that, "Not only are first-time homebuyers unfamiliar with the process, they face unique hurdles. They don't bring equity or a credit history from a previous home. Their finances face additional scrutiny. And for those seeking an FHA loan for down payment, there are restrictions on type of home and its amenities."

First timers are, of course, likely to be buying in the starter home category as are those so-called boomerang buyers who have served their obligatory time-out after foreclosure and are now able to move back into the market, but may still have damaged credit.

Trulia explains that there could also be an interrelationship between the age and the price tier. Premium homes make up more than 70 percent of all listings built after 2000 and less than 40 percent of those built before 1980. "Since premium homes have the lowest fail rate regardless of year built, their dominance drives down the fail rate in more recently built homes, and their smaller role pushes up the fail rate in older homes."

Also, homes that are 20 to 40 years old are more likely to be encountering their first round of expensive maintenance needs, increasing the likelihood of deals failing based on home inspections. Homes older than 40 years, to remain livable, have probably already had some major problems addressed. There is also the possibility that buyers seeking older homes may anticipate encountering needed repairs and upgrades.

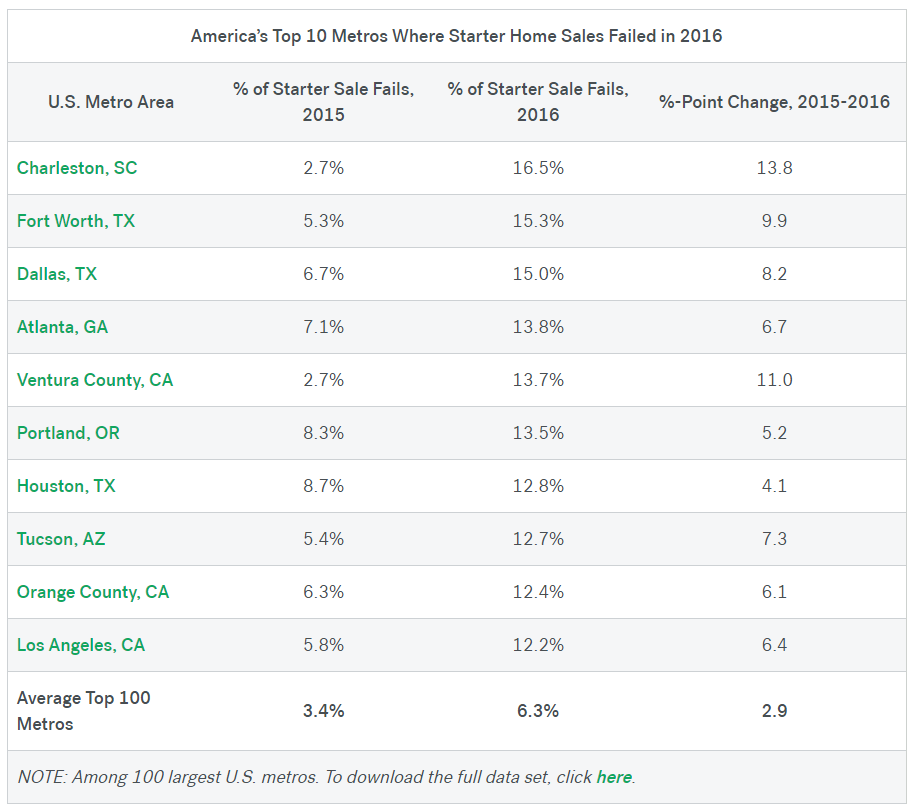

Looking at the geography of failed sales, eight of the 10 metro areas with the highest percentage over the last two years are clustered in the West and three are in California. In the fourth quarter of 2016, seven are in the West, four of which are in California.

We asked NAR to comment on the Trulia report. Their spokesperson, Adam DeSanctis, said that among the questions NAR asks its members in its monthly Realtors Confidence Index is if their most recent sales contract was either closed or terminated. He supplied us with the three-month rolling averages for the last two years which, as he said, show settlements and terminations remaining roughly the same. During the first three months of 2015, the averages were at 9 or 10 percent. Since then they have consistently ranged between 6 and 7 percent.

NAR adds, however, "There is another way of looking at this that may confirm Trulia's finding. Because of constrained inventory data in much of the country, the percent share of sales sold at or above list price has recently been convincingly higher than a year ago. This would indicate an increase in multiple offers on a home that's for sale."

Data they supplied on this phenomenon, dating back to 2012, shows that while above listing price sales have not increased at a steady rate, they have trended upwards, starting at 28 percent in December 2012 and reaching as high as 40 to 43 percent through most of the second and third quarters of 2016. In the fourth quarter the figure settled back to 37 percent.

DeSanctis said that, "Especially among first-time buyers, there could very well be cases where a contract is delayed or terminated because the buyer couldn't come up with the additional cash or more financing to close the deal. "

Trulia concludes by saying it is important that a potential buyer do everything possible in the way of mortgage approval and preapproval and to know his or her financial limits. This will make it easier to recognize potential challenges and opportunities earlier in home buying process. Sellers and agents would be well serviced to know about the market and the home and to confront any problems areas that would be likely to come up in an inspection.