Consumers are displaying a bit of bearishness toward the economy according a Federal Reserve Bank of New York's recent survey of how they expect overall inflation and prices for food, gas, housing and education to behave. The December Survey of Consumer Expectations (SCE indicates that median expectations about growth in household income, earnings and especially household spending all declined while there were mixed feelings about job security.

The SEC queries a rotating panel of 1,200 household heads. The sample, structured to be nationally representative, is designed to observe changes in expectations and behavior of the same individuals over time with respondents remaining on the panel for up to 12 months and an approximately equal number rotating in and out each month. The survey is Internet based and is conducted for the New York Fed by The Demand Institute, a non-profit organization jointly operated by The Conference Board and Nielsen. The sampling frame for the SCE is based on that used for The Conference Board's Consumer Confidence Survey (CCS).

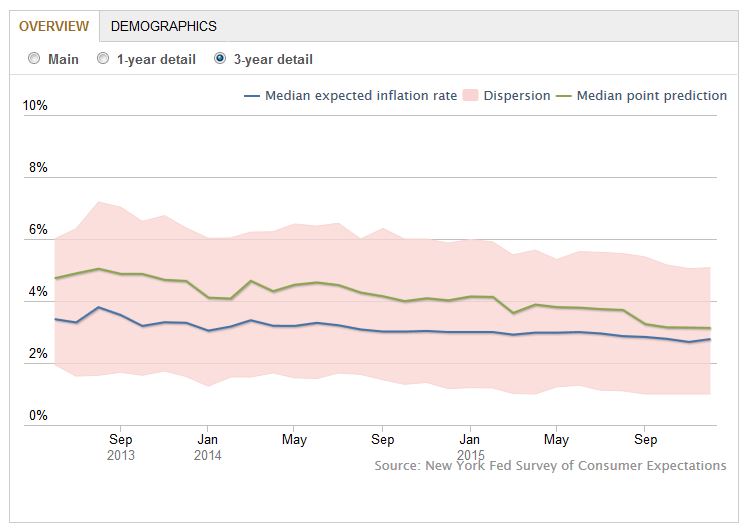

The panel's predictions about inflation were essentially unchanged, with a median expectation of 2.5 percent over the next year tying the survey low set in November. Longer term expectations rose slightly with the three year horizon up 0.1 point from the previous month - also a survey low - to 2.8 percent. Uncertainty about inflation declined for both one-year and three-year horizons to new survey lows.

Consumers expect home prices to rise a median of 3.0 percent, slightly lower than in November and matching earlier survey lows established in February and August 2015. Expectations for other individual item price changes also declined slightly in the one-year window.

Responses to questions about the labor market were mixed in tone. Predictions about the growth in earnings over the next year declined from a median of 2.5 percent to 2.0 percent, the largest one-month drop in survey history, returning responses to the level last seen two years earlier. The decline was widespread across all age groups, and especially strong for low education and middle-income workers.

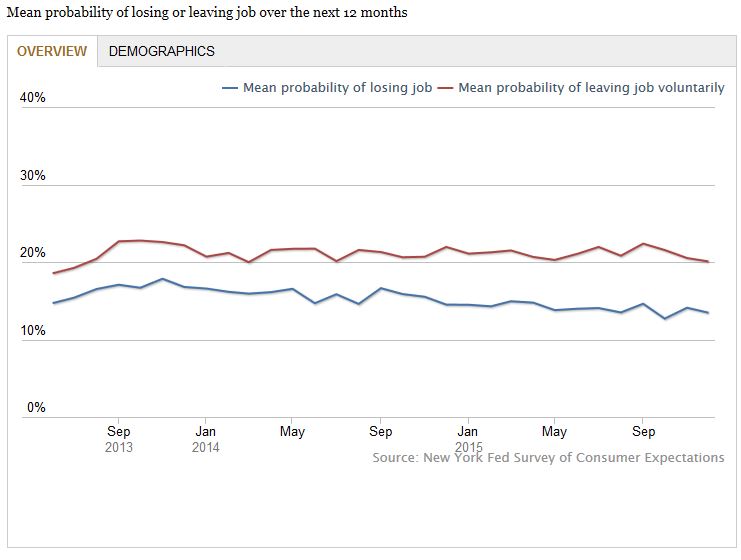

The perceived probability of losing a job decreased slightly from a mean of 14.1 to 13.5 percent - the second lowest reading since the start of the survey. The decline was driven by older, lower education and lower income workers. The perceived probability of leaving a job voluntarily also declined and is at the lower end of the survey's historic range.

But if respondents were slightly more optimistic about keeping their job they were less so about finding a new one within three months should they lose it. Responses there decreased from the November series high to 55.1 percent, although still high in the historic context.

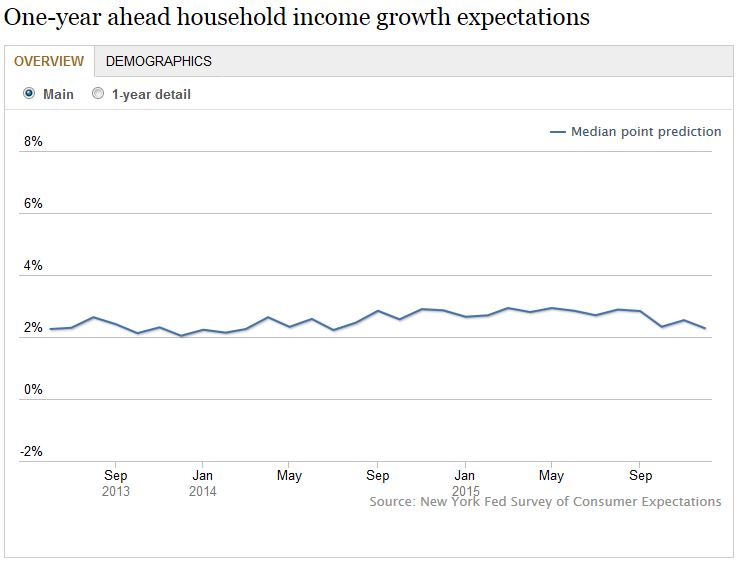

Expectations for household income growth over the next year diminished from a median increase of 2.6 percent in November to 2.3 percent. This is an even more pronounced drop when compared to the 2.7 to 2.9 percent range of responses in the first nine months of the year. This decline seems to be driven by younger, higher education and higher income respondents.

Household spending is also projected to decline, going from a one-year ahead median of 3.6 percent in November to 2.9 percent, the lowest level since the inception of the survey in June 2013. The decline was particularly strong among older, lower education and lower income respondents.

Credit availability is perceived to be unchanged over the past year by about the same percentage of respondents as in November and expectations for change over the next year also remained the same. The mean perceived probability of higher average interest rates on savings accounts over the next year reached a new series high at 35.1 percent.