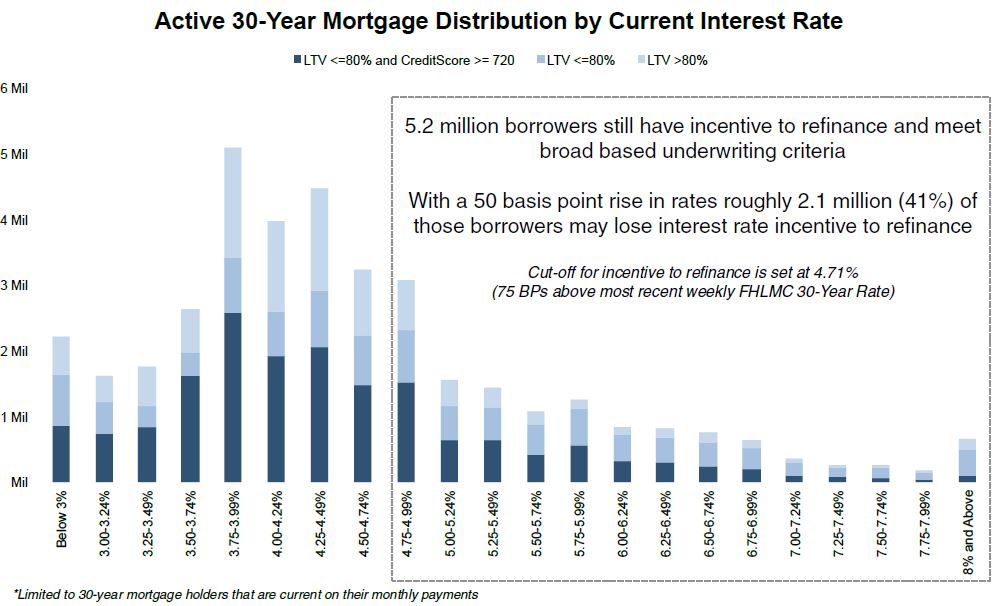

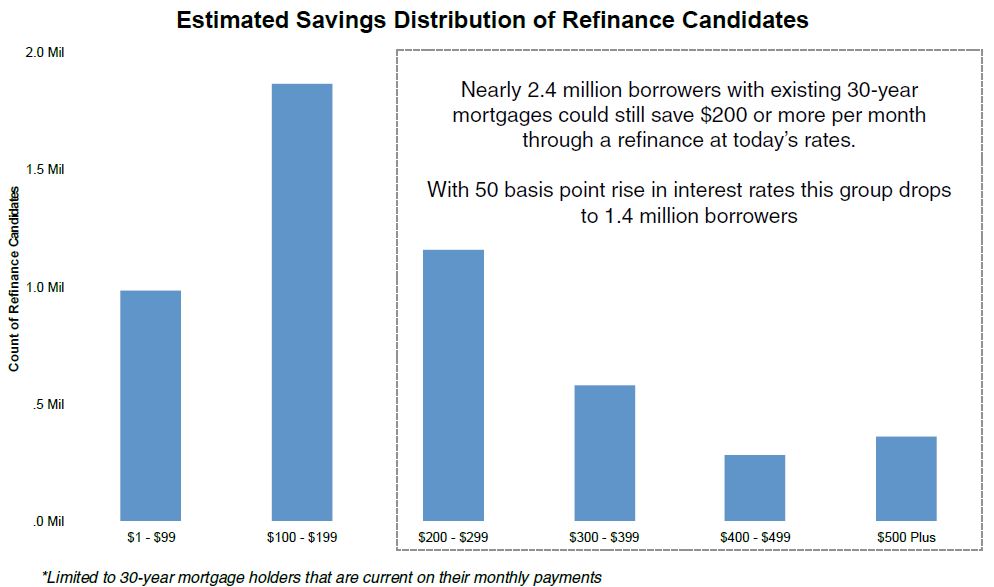

Years into the refinance boom Black Knight Financial Services estimates there are still millions of homeowners who could qualify for and benefit from turning in their existing mortgages for a new model. The company, in its current Mortgage Monitor says that group includes about 5.2 million homeowners and that 2.4 million of them could save $200 or more per month through refinancing.

The pool is shrinking however as interest rates rise and Black Knight estimates that a 50 basis point increase in rates would eliminate 2.1 million potential candidates from refinance eligibility, a 42 percent drop. A full point increase would take out an additional 1 million borrowers.

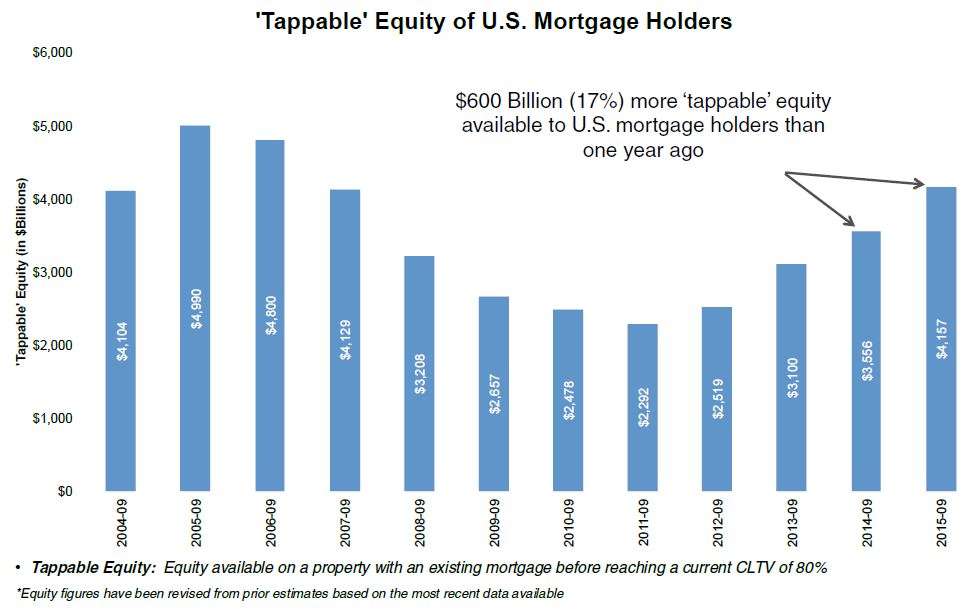

There is still a lot of equity out there that homeowners could utilize if they wished. That "tappable" equity is probably around $4.2 trillion and has increased by $600 billion in the last 12 months.

But even as homeowner equity has increased, the pool of potential refinancers has shrunk, down from over 7 million as recently as April 2015 when 30 year rates were below 3.7 percent. Black Knight put the 30-year fixed rate at the time of its analysis at 3.96 percent.

Black Knight Data & Analytics Senior Vice President Ben Graboske explains. "Looking at current interest rates on existing 30-year mortgages and applying a set of broad-based underwriting criteria, we found that there are still approximately 5.2 million borrowers that make good candidates for traditional refinancing. The full-point increase mentioned above, he says, would leave only 2 million potential refinance candidates, the lowest number in recent history.

While at present over 2 million homeowners would be able to save $200 or more on their monthly mortgage payments post-refinancing, Graboske said, this is a very rate-sensitive population. With a 50-basis-point rise in rates a million of them would see those savings fall to an average of less than $100. However the largest share - about 38 percent or 1.8 million borrowers, would still see savings in the $100 to $200 range. This would mean an aggregate monthly savings of about $1.2 billion across the 5.2 million potential refinancers.

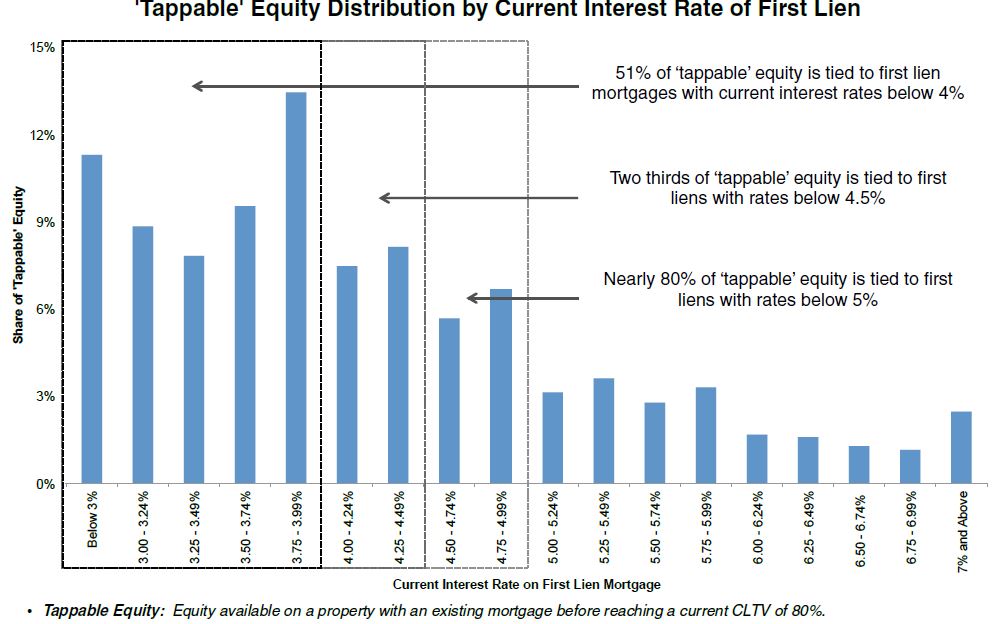

He continued, "We also looked again at the amount of tappable equity available on each home with a mortgage - by using an upper limit of 80 percent current combined loan-to-value (CLTV), including first and second liens. In total, we're looking at over 37 million borrowers with current CLTVs below 80 percent that have an average of $112,000 equity available to tap in their homes, an increase of 3.1 million from just a year ago. Roughly half of that tappable equity belongs to borrowers whose first-lien mortgages have current interest rates higher than today's 30-year rate - making them potential candidates for cash-out refis - but the other half are under 4 percent. While it's not a hard and fast rule that borrowers won't refinance into a higher rate in order to tap available equity - 23 percent of cash-out refi borrowers over the past six months did just that - for the most part, as rates rise, HELOCs will continue to become more popular to homeowners looking to tap available equity."

While there is now nearly twice the amount of tappable equity as there was at the bottom of the housing market that amount remains about 17 percent below 2005 levels. Nearly 1.6 billion or 38 percent of this equity is in California with Texas and Florida following at 6 percent each.

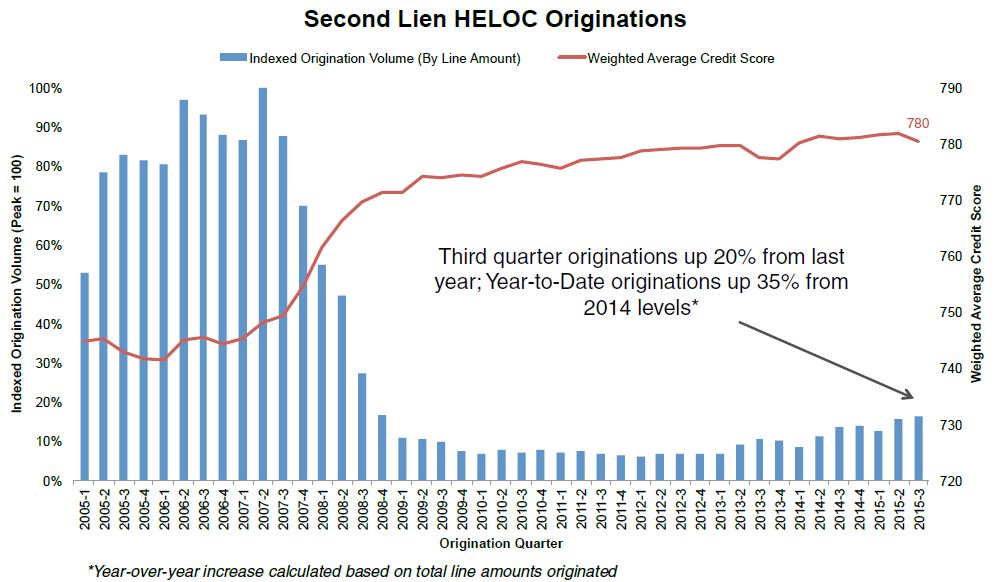

Black Knight's November 2015 data showed that HELOC originations have continued to rise. There has been year-over-year growth in originations in each quarter since the beginning of 2013 and the total credit line amounts originated climbed 35 percent in 2015 through November compared to the same date in 2014. The numbers of loans have not risen as fast, the count was up 8 percent in the third quarter from Q3 2014 and up 8 percent year-to-date.

At the same time traditional second lien mortgages have become relatively non-existent. Those loans are down 10 percent year-over-year.

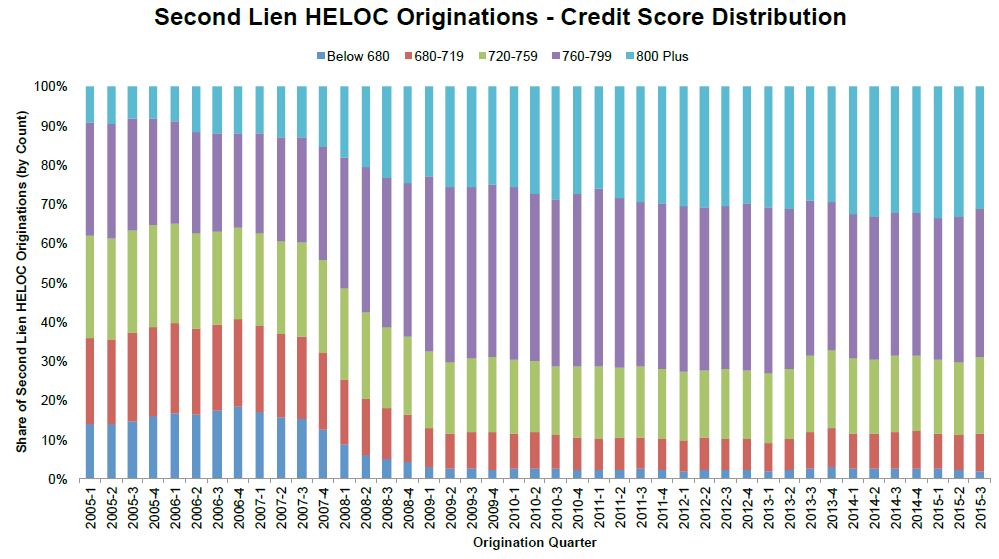

Credit score for HELOC loans remain near historic highs. Nearly 70 percent of those loans by count and 75 percent by loan amount are going to borrowers with credit scores of 760 or higher with only 2 percent are going to borrowers with scores below 680, the lowest share in over 10 years.

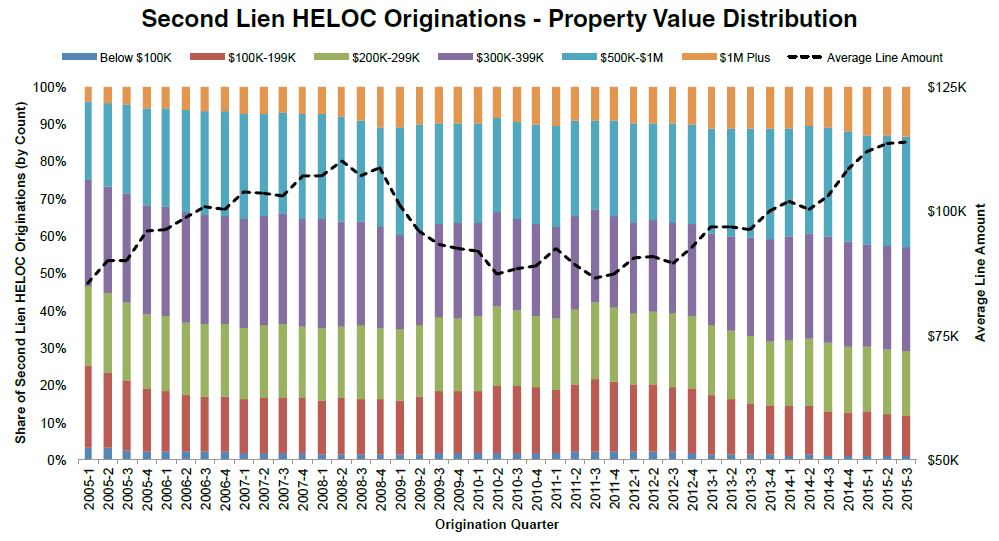

The average HELOC credit line is nearly $114,000, the highest since Black Knight began tracking this data back in 2005. However, while HELOC line amounts may be at 10-year highs, initial utilization rates - a key HELOC risk factor - are near 10-year lows. In addition, the average resulting CLTV for borrowers with second-lien HELOCs is 66 percent, well below the 75-76 percent range seen during the bubble era. Nearly 43 percent of HELOCs are on properties valued over $500,000, the highest share on record, and 70 percent are on properties over $300,000. Only 12 percent were given on homes in the lowest price tier - under $200,000, the smallest share on record. When home prices were at their peak in 2006 roughly 35 percent of HELOCs were given on properties of over a half-million.