Three staff member of the Federal Reserve Bank of San Francisco have published, on the Bank's website, results of a study about what drives the mortgage choices of borrowers. The three, Fred Furlong, David Lang, and Yelena Takhtamanova looked at the question of whether lower-rated borrowers paid less attention to loan pricing and interest-rate-related factors because house prices were rising rapidly.

They developed a model to account for the factors that influence mortgage choice. Earlier research has found that mortgage pricing and other interest-rate-related fundamentals are key but they also looked at housing market conditions and borrower characteristics, such as degree of financial constraint, attitudes towards risk, and mobility. Research has shown that financially constrained borrowers, or those with lower credit ratings tend to favor adjustable rate mortgages (ARMs) as do homebuyers who expect to only stay in a house a short time because ARMs have lower introductory interest rates.

Fixed-rate mortgages (FRM) initially tend to have higher interest rates than ARMs because they are tied to long-term interest rates which include a term premium to compensate investors for tying up their money longer. Both FRM and ARM rates include lender margins, that is, mark-ups reflecting general credit supply conditions, regional economic and housing market conditions, and individual borrower characteristics. Relative shifts in FRM and ARM margins can affect financing choices.

How much risk borrowers are willing to accept also can influence mortgage choice. Borrower risk tolerance can affect sensitivity to loan pricing, income volatility, and affordability in choosing mortgages. Borrowers with low credit ratings may be less sensitive to risk, for instance, because of lower cost of default. Research shows that more risk-averse borrowers tend to favor FRMs or option ARMs because they prefer to avoid the risk of future sharp rate increases possible with volatile adjustable-rate financing.

Thus, a mortgage choice model should include measures of the term premium, expected short-term interest rates over time, FRM and ARM margins, and interest rate volatility. In general, borrower preference for basic ARMs should increase as the term premium, expected short-term interest rates, and FRM margins rise, and ARM margins and interest rate volatility fall. In other words, the more affordable ARMs become by comparison, the more they're favored. No surprises here...

Research also shows that the faster house prices are rising, the greater the probability that homebuyers will choose ARMs. In addition, rising house prices can affect the importance of interest-rate-related fundamentals when borrowers choose financing.

The researchers say that one view is that the housing boom was a bubble in which financing decisions for some borrowers were divorced from traditional fundamentals while another is that borrowers paid less attention to fundamentals during the housing boom, but that such a shift is consistent with rational decision-making models, given expectations of further house price appreciation. According to this view, with little or no change in house prices, homeowner decisions about moving or terminating a mortgage would generally reflect life-cycle events, such as illness, retirement, and job changes.

Rapid house price gains might change that. During the boom homeowners expected to gain home equity as prices rose, allowing them to refinance even if they didn't plan to move or expected to flip houses soon after buying them. Such short-term mortgages might make ARMs more attractive and reduce borrower sensitivity to interest-rate-related fundamentals. In other words, they didn't care as much about the riskier nature of the loans because they planned on being out of them relatively quickly.

Finally, studies suggest that borrower financial literacy may affect mortgage choice. Borrowers who choose ARMs appear more likely to underestimate or not understand how changes in interest rates would affect their loans. Hence, systematic differences in levels of financial literacy among borrowers at different risk levels could affect sensitivity to fundamentals.

The study's model of mortgage choice allows for an examination of how these factors affected the decisions of borrowers at different credit risk levels. The authors studied a sample of about 9 million first-lien mortgages originated between January 1, 2000, and December 31, 2007 allowing for three mortgage choices: FRMs, basic ARMs, and option ARMs. Key model determinants are FRM and ARM margins, the 10-year Treasury term premium, expectations for short-term interest rates over time, and interest rate volatility. Controls included loan-to-value ratios, borrower credit risk, the two-year average change in house prices, and a measure of house price volatility. Finally, credit risk groups were defined by FICO scores: low, 660 or below, high, 760 or above, and medium 661 to 759.

The model allows the impact of interest-rate-related fundamentals to change as house prices rise. The estimates show that rising house prices have a sizable influence on the effect these fundamentals have on mortgage choice. The size of this effect differs according to borrower credit ratings.

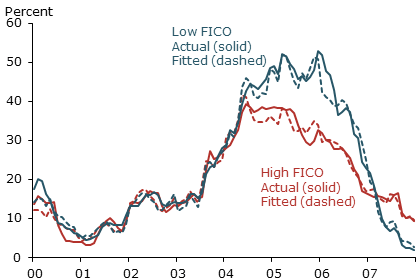

Fig. 1

Figure 1 shows the impact of margins and term premiums on the probability of borrowers choosing an ARM. The green bars indicate those factor's marginal effects if house prices are static. A higher margin makes ARMs less attractive so the marginal effects are negative. The low FICO group shows a greater effect indicating they are more sensitive to ARM mortgage pricing than the higher FICO cohort. "Specifically, if house prices were flat, a 0.8 percentage point increase in the ARM margin would reduce the probability of low FICO borrowers choosing an ARM 13 percentage points and high FICO borrowers 8 percentage points. It is useful to compare this with the ARM share of mortgage originations, shown in Figure 2, which peaked at 50%."

The two year average house price appreciation was 16 percent. The red bars show the offsetting effects of this with a reduction of one-third in the ARM margin to 8 percentage points for low FICO borrowers and 5 points for high FICO borrowers. Similarly, house price appreciation reduces the impact of increases in the FRM margin and term premium on mortgage choice. Thus, even accounting for the influence of house price gains, lower FICO borrowers generally were at least as sensitive, if not more sensitive, to fundamentals as the high FICO borrowers.

Fig. 2

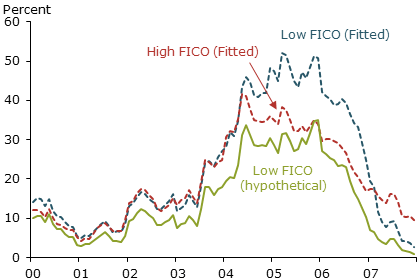

But, if low and high FICO borrowers gave similar consideration to interest- rate-related fundamentals, why were low FICO borrowers more likely to select ARMs during the housing boom? Credit risk measures, including FICO scores and lender designation of borrowers as subprime, explain most of the difference in ARM shares. The authors considered whether borrowers would have made the same mortgage choice if, all else equal, they had different credit ratings. In Figure 3, for each month in the sample, they replaced the actual FICO score and subprime designation of each borrower in the low FICO group with the average score and subprime share of the high FICO group. The results of this hypothetical exercise, shown by the green line, suggest that the low FICO group's ARM share would have been closer to that of the high FICO group had their credit risk been similar.

Fig. 3

One could interpret the results as credit risk measures being associated with borrower level of financial sophistication or the findings could reflect economic decisions related to risk aversion, credit constraints, or differences in how quickly borrowers expect to refinance. The authors conclude rising prices during the housing boom muted the influence of interest rate fundamentals on borrower mortgage choice, especially among borrowers with lower credit ratings. But when house prices rose rapidly, those borrowers responded at least as strongly as higher-rated borrowers to changes in fundamentals. "This suggests," they say, "that the greater propensity of low FICO borrowers to choose ARMs is more consistent with mortgage choice reflecting economic considerations rather than lack of financial sophistication among low FICO borrowers."