The Millennial Generation, adults born between 1981 and 1996, were late bloomers when it came to buying a home. They came of age just in time to be clobbered by the Great Recession, have been burdened by high levels of student debt, were slow to form households, and once they did, watched home prices skyrocket. Still, as economist Archana Pradhan points out in the October edition of CoreLogic's Intelligence Newsletter, the generation has now embraced homeownership enthusiastically.

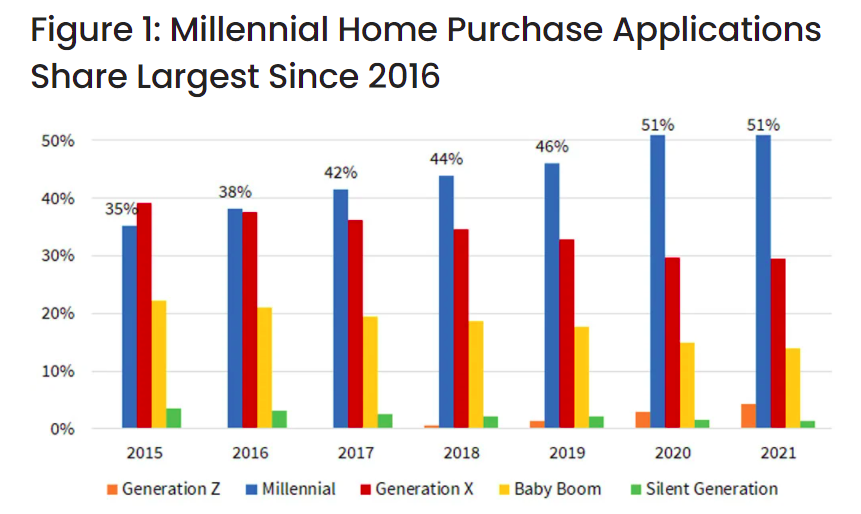

Pradhan says Millennials have accounted for the largest share of home purchase mortgage applications since 2016 and accounted for 51 percent so far in 2021, up from 46 percent in 2019. Younger Millennials are still in their first-home buying years while older members of the generation are of an age to be moving up. In both cases they are a potent force in the market. In 2021 they have accounted for 67 percent of mortgage applications for first-home purchases and 37 percent of those for repeat purchases.

The Millennial share varies across housing markets and previous CoreLogic research has shown those homebuyers made choices based on factors including affordability, employment opportunities, ability to work remotely, and local taxes. While they have more buying power in affordable markets, other CoreLogic data shows the generation still accounts for large shares of purchases in more costly locations, especially those with high-tech job opportunities.

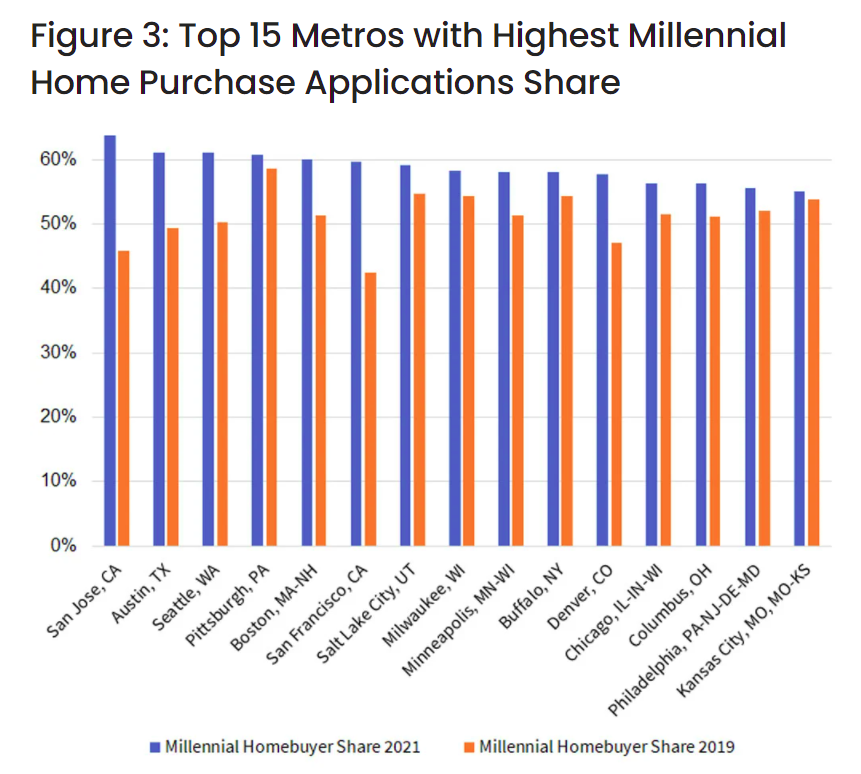

San Jose had the highest percentage of Millennials applying for a mortgage at 64 percent, followed by Austin, Seattle, Pittsburgh, Boston, and San Francisco, all with shares of at least 60 percent. These and the remainder of the top ten (Salt Lake City, Milwaukee, Minneapolis, and Buffalo) were either quite affordable or offered high-tech employment.

Conversely, metros in Florida and Arizona had the lowest percentage of millennials applying for a home mortgage. Miami and Las Vegas were at the bottom with 43 percent, followed by Orlando, Tampa, Phoenix, and Jacksonville. None exceeded a 45 percent share.

Among those metropolitan areas with high shares of Millennial buyers, those with high-tech opportunities are increasing their share more rapidly than those where affordability appears to be the magnet.

That growth also has a positive relationship with increases in the high-tech employment, although to be fair, Pradhan points out that Millennial homebuyers in San Jose, San Francisco and Boston had the highest average credit scores, highest average income and made a bigger down payment. This could be a result of higher wages among high-tech industry jobs, which have been attracting millennials. Also, the share of older buyers in these high-cost areas is falling as homeowners sell their houses and move to lower cost areas in warmer climates. This could account for the small shares of Millennial homebuyers in Florida and Arizona metros.

Pradhan concludes, "Despite affordability challenges for many potential millennial homebuyers, especially in the high-cost market, millennials with high-tech skills whose compensation is commensurate with local living costs can buy homes. Declining numbers of older generation homebuyers is contributing to change in the ratio as well, because as older generation buyer share declines, millennial share rises."